iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

Information-technology Promotion Agency, Japan (IPA), Japan External Trade Organization (JETRO), and the Indian Software Product Industry Roundtable (iSPIRT) have shared common views that (i) our society will be transformed into a new digital society where due to the rapid and continued development of new digital technologies and digital infrastructure including digital public platforms, real-time and other data would be utilized for the benefit of people’s lives and industrial activities, (ii) there are growing necessities that digital infrastructure, together with social system and industrial platforms should be designed, developed and utilized appropriately for ensuring trust in society and industry along with a variety of engaged stakeholders and (iii) such well-designed digital infrastructure, social system and industrial platforms could have a great potential to play significant roles to improve efficiencies of societal services, facilitate businesses, realize economic development and solve social issues in many countries.

Today, we affirm our commitment to launching our cooperation and collaboration through the bringing together of different expertise from each institution in the area of digital infrastructure, including mutual information sharing of development of digital infrastructure, in particular, periodic communication and exchange of views to enhance the capability of architecture design and establishment of digital infrastructure. We further affirm that as a first step of our cooperation, we will facilitate a joint study on digital infrastructure, such as (i) the situation of how such digital infrastructures have been established and utilized in India, Japan and/or other countries in Africa or other Asian regions (the Third Countries) as agreed among the parties, (ii) how the architecture was or can be designed for digital infrastructure as a basis for delivering societal services in the Third Countries and (iii) what kind of business collaboration could be realized, to review and analyze the possibility of developing digital infrastructure in the Third Countries through Japan-India cooperation. We may consider arranging a workshop or business matching as a part of the joint study to figure out realistic use cases.

Our cooperation is consistent with the “Japan-India Digital Partnership” launched between the Ministry of Economy Trade and Industry, Government of Japan and the Ministry of Electronics and Information Technology, Government of India in October 2018. We will work closely together and may consider working with other parties to promote and accelerate our cooperation if necessary.

For our most recent Startup Bridge Salon on May 9th, we had planned for sixty 1-1 strategic partnership meetings between 11 B2B startups and 35+ US corporates. In the weeks leading up to the event and the week post-event, we clocked 115 meetings. Read more to learn about the event & program, and how you can participate or get involved.

I got 10 meetings with decision makers through StartupBridge which is worth 1000 business cards at a trade show. (Raviteja, CEO @Moengage, May 2019)

I made 18 connects out of which 11 are of extremely high value. (Aditya, CEO @FirstHive, May 2019)

History of StartupBridge, M&A/PSP Connect

In 2013-14 the M&A Connect (and Business Exchange BEX) program was established as part of iSPIRT’s Market Catalyst pillar to help solve the problem of extremely low “exits” to “investment” ratio for startups in India. Strong “exits” are healthy markers of a mature startup ecosystem, closing the cycle of capital flows. The program consisted of developing a strong match between the global corporates interested in acquisitions (buy-side) and Indian startups (sell-side).

The initial problem was a discovery issue where Indian startups were not on the radar of these potential acquirers. The M&A connect program activated the India radar, by engaging the buy-side to collect deep virtual mandates, and use it to match and make warm connects with the sell-side, at times hand-holding the connect process to several favorable outcomes.

In this program, we found that our startups were not effective at pitching their story to a potential acquirer. This resulted in a few aborted connections. Additionally, it became clear that the path to an effective M&A lay in facilitating potential strategic partnerships (PSP), which if nurtured has the potential to blossom into investments or acquisitions. Strategic partnerships can surface in the form of technology or GTM/distribution level enfgagement between startups and larger corporates. It can open several doors instantly, making distribution easier, revenue growth faster and gives the startup multiple options.

The M&A Connect program morphed into PSP Connect (Dec 2016 onwards) and the program goals moved from pure M&A to building strategic partnerships. iSPIRT partnered with TiE leaders in Silicon Valley to create the Startup Bridge India initiative (SBI), where many buy-side companies were invited to meet and explore strategic level engagement with highly curated sell-side startups.

The Startup Bridge Approach

Over the last 3 years, the SB team, iSPIRT volunteers and TiE partners, have helped B2B SaaS/enterprise startups refine their air-game, and engage in partnership discussions with high conversion outcomes.

We have connected 45 startups to Fortune 1000 corporations and in the process catalyzed $200M+ of value in terms of PSP (potential strategic partnership), customers and M&A. (Manu Rekhi, Inventus Capital & Startup Bridge)

The key value proposition is to help startups scale revenue by 10x in 2 years through meaningful PSP connects with decision-makers at global Fortune 1000. In turn, these corporations leverage SB to engage with highly curated startups to get access to technology and product gaps.

We are effectively the bridge over the chasm that most startups struggle with, and the potential disruption that many corporates are worried about.

Startup Selection

Did you know that ~50% of Unicorn enterprise startups in the Silicon Valley have an Indian founder or co-founder and had origins or back-offices in India?

Our stringent startup selection process is essential for matching the “Who in India” with the “Who in USA”. Data from the program over the years have shown that the startups which stood to leverage the program effectively and benefited the most were in the ARR range of $500K to $5M. Hence SB’s high-level criteria for inducting B2B enterprise/SaaS startups into the program focus on a) having a global product-market fit, preferably in the US, with b) a strong footprint & revenue (~$1M ARR), and c) bringing deep technology, high revenue potential and/or a high growth momentum.

PSP Wishlist

Karthik & Vinod discuss their key partnerships approach

On the buy-side, it is critical to engage corporates who can enable the 10x growth for these startups. Most startups see partnerships as tactical like with a reseller, system integrator (SI), channel/OEM partner… A strategic partner goes beyond tactical value. A startup can explore and collaborate with a PSP to accelerate its strategy in the emerging focus area. In return, the PSP provides a rocket boost to the startup’s customer acquisition, distribution, branding, and/or a holistic product strategy. Having such a partner can also significantly impact startup valuation.

As a startup, you need to think about a PSP early in the game at the ‘Flop’ and not at the ‘Turn’. You need time to develop a PSP and you need to start early. (Vijay Rayapati, Nutanix, Jul 2018)

If you think of the value chain of your customers, their vendors, integrators, solution & platform providers, a strategic partner may lie above you and your peers, and a level or two above your target customer. Often high growth customers can transform into strategic partners. We help the startups think through their PSP wishlist and make relevant recommendations.

Startup Air Game

Pitching to a PSP company is very different from the pitching to a customer or to an investor. A well-articulated pitch can make a difference between a yawn and a wow! A great startup pitch highlights their Mission, problem statement, their solution & approach, the product/platform overview, key metrics & traction, unit economics of growth & acquisition, testimonials, market size & drivers, and finally their ask.

I thought I knew my pitch and had the details at my fingertips. But then I started getting really valuable, thought-out feedback…I had to focus on pitching to partners, not customers. (Pallav Nadhani, FusionCharts, Dec 2016)

Mentor feedback sessions during the boot camp

It takes 100 hours per startup to articulate their value proposition into a pitch deck of only 10 crisp slides. The initial hours creating & refining their pitch deck with assigned mentors. It is followed by a day-long boot camp before the event where they are grilled through their pitches by the SB team, startup & corporate mentors from the industry, and successful entrepreneurs.The multiple rounds of feedback not only cover their proposition, but also helps weave in the founders’ story, and develop their stage presence, and tonality. Post boot camp they work on the critical feedback with their individual mentors, sometimes even redefining their models & assumptions, and final dry runs with the SB team. The results at every SB event have been astounding 7-min founder pitches amazing every attending corporate and industry leader.

Tapesh and his amazing 7-minute “technicolor” pitch deck

PSP Virtual Mandates & Exclusive Connects

Vamshi 1-1 connects over the roundtable.

We have found that startups require 2 points of support for effective partnership outcomes. First, crafting warm connects based on virtual mandates. Second, prime focus on shepherding the startup-partner conversations on a rolling basis. The unmet need is to have 1-1 connects with the right person on common ground.

I went from first discussion into pricing in one week with a Fortune 10 company. Getting in front of the decision maker is all the difference. As a founder/CEO I can close the sale without the long drawn out sales process. (Sanjoe Jose, CEO @Talview, May 2019)

Bringing PSP companies into our network, we connect with key profiles within the company on their build-buy-partner outlook. This helps in surfacing several latent areas of focus for partnerships, investments or acquisitions. Constructing the virtual mandate out of these relations is key to recommending a high-potential match between the startups and corporates.

All startup bridge sessions and introductions are curated and by invite-only.

Exclusivity made the quality of event and connections even more important. I attended because of an impressive amount of my peers from other Fortune 1000 companies. (Rahul Kamath, VP Oracle, May 2019)

Impact to Date

The stringent startup curation criteria ensure high potential innovation & growth partnerships for corporates. The intense boot camp and mentoring hours help startups develop highly effective positioning in the market. The latent virtual mandates enable effective match-making resulting in extremely relevant growth opportunities for the startups.

If I had to do this on my own each of these connections would have taken 8-12 weeks of effort.

Though these events get significant attention & traction, the goal of the SB program is to deliver these connections on a rolling basis. Here are some stats and anecdotes across the years:

19 out of the 45 startups in the SB cohorts have grown 10x in the past 2 years.

749 connections to decision-makers have been made to-date with >$200M of value creation in terms of partnerships, customer purchases, and M&A.

121 PSP connections from the May 9th event and beyond.

3 exits and 1 more on the way.

Focus on quality and value creation has resulted in consistent high NPS 56-81. This focus on quality is the core principle of this community lead effort and the hallmark of success so far.

What can you do?

Shifting from its pro-bono, volunteer-run orbit, Startup Bridge is transforming into a mature, scalable global program. By broadening the corporate network reach beyond Silicon Valley, and expanding support to startups of Indian origin regardless of domicile, the program is poised to benefit startups and corporates at scale. Upcoming SBDays are being planned for New York, Bay Area, Japan. Startup Bridge continues to be mission-driven, helping fill a critical gap in strategic partnership building for Indian origin startups.

If you are a startup or would like to refer a startup to be part of the SB program please fill the partnership application form. Alternately you could email us at [email protected].

If you are a corporate exec and/or can help us with decision-makers (CXOs, EVP/SVP, GM), or key influencers (VP/Director of Partnerships, Corporate Development) please email us at [email protected].

[This post could not have been possible without inputs from the SB Team & iSPIRT volunteers, Dipty Desai, Jibin Jose, Manu Rekhi, Raju Reddy, Sharad Sharma, Sijo George, Rajan Thiyagarajan, Vrushali Malpekar, and volunteers from the previous Startup Bridge/PSP Connect program. Also, personal thanks to all the volunteers, mentors, and the participating startups for making the SB Salon on May 9th successful.]

In January 2016 iSPIRT ran the largest software entrepreneur school in India, called PNgrowth (short for Product Nation Growth). The central vision of PNgrowth was to create a model of peer learning where over 100 founders could give each other one-on-one advice about how to grow their startups. With peer learning as PNgrowth’s core model, this enterprise was supported by a volunteer team of venture capitalists, founders, academics, and engineers. See iSPIRT’s volunteer handbook (https://pn.ispirt.in/presenting-the-ispirt-volunteer-handbook/)

However, unlike a regular “bootcamp” or “executive education” session, the volunteers were committed to rigorously measuring the value of the peer advice given at PNgrowth.We are excited to announce that the findings from this analysis have recently been published in the Strategic Management Journal, the top journal in the field of Strategy, as “When does advice impact startup performance?” byAaron Chatterji, Solène Delecourt, Sharique Hasan, Rembrand Koning (https://onlinelibrary.wiley.com/doi/10.1002/smj.2987).

TLDR: Here’s a summary of the findings:

1. There is a surprising amount of variability in how founders manage their startups. To figure out how founders prioritized management, we asked them four questions:

“…develop shared goals in your team?”

“…measure employee performance using 360 reviews, interviews, or one-on-ones?”

“…provide your employees with direct feedback about their performance?”

“…set clear expectation around project outcomes and project scope?”

Founders could respond “never,” “yearly,” “monthly,” “weekly,” or “daily.”

Some founders never (that’s right, never!) set shared goals with their teams, only did yearly reviews, never provided targets, and infrequently gave feedback. Other, super-managers were more formal in their management practices and performed these activities on a weekly, sometimes daily, basis. Not surprisingly, the supermanagers led the faster-growing startups. Most founders, however, were in the middle: doing most of these activities at a monthly frequency.

2. Since PNGrowth was a peer learning based program, we paired each founder (and to be fair, randomly) with another participant. For three intense days, the pairs worked through a rigorous process of evaluating their startup and that of their peer. Areas such as a startup’s strategy, leadership, vision, and management (especially of people) were interrogated. Peers were instructed to provide advice to help their partners.

3. We followed up on participating startups twice after the PNgrowth program. First ten months after the retreat, and then we rechecked progress two years afterwards.

We found something quite surprising: the “supermanager” founders not only managed their firms better but the advice they gave helped their partner too. Founders who received advice from a peer who was a “formal” manager grew their firms to be 28% larger over the next two years and increased their likelihood of survival by ten percentage points. What about the founders who received advice from a laissez-faire manager? Their startup saw no similar lift. Whether they succeeded or failed depended only on their own capabilities and resources.

4. Not all founders benefited from being paired up with an effective manager though. Surprisingly, founders with prior management training, whether from an MBA or accelerator program, did not seem to benefit from this advice.

5. The results were strongest among pairs whose startups were based in the same city and who followed up after the retreat. For many of the founders, the relationships formed at PNgrowth helped them well beyond those three days in Mysore.

So what’s the big take away: While India’s startup ecosystem is new and doesn’t yet have the deep bench of successful mentors, the results from this study are promising. Good advice can go a long way in helping startups scale. iSPIRT has pioneered a peer-learning model in India through PlaybookRTs, Bootcamps, and PNgrowth (see: https://pn.ispirt.in/understanding-ispirts-entrepreneur-connect/).

This research shows that this model can be instrumental in improving the outcomes of India’s startups if done right. If peer-learning can be scaled up, it can have a significant impact on the Indian ecosystem.

David Vs. Goliath had a happy ending, but the odds of beating Goliath as a startup are slim and most startups do not have a fairytale ending, unless…

At SaaSx5, I had the opportunity to hear Vijay Rayapati share his story of Minjar. This was a fairy tale with all the right ingredients that kept you engrossed till the end. With angels (investors) on their side, along with Minjar and Vijay’s prior experience, Minjar could have faced many Goliaths in their journey. Instead of going the distance alone, Vijay followed the Potential Strategic Partner (PSP) playbook (Magic Box Paradigm) and identified one in AWS. His reasons were clear, one of the biggest challenges a startup faces is distribution. And, a PSP can open several doors instantly, making distribution easier, revenue growth faster and gives the startup multiple options. As a startup, you need to think about a PSP early in the game at the “Flop” and not at the “Turn”. You need time to develop a PSP and you need to start early.

Identifying a PSP in your vertical maybe easy, but building a relationship with them is the hardest. It requires continuous investment of time to build the bond with the PSP such that they become the biggest evangelist of your product. This involves building relationships with multiple people at the PSP -from Business, Product & Tech- to make sure you have the full support from the company to scale this relationship without roadblocks. In the case of Minjar, with AWS as their PSP, it opened roads to customers, built their brand and also increased the value of the company. One of the highlights of the Minjar story was about the CTO of AWS, evangelizing the product at their conference. As Vijay ascertained “Invest time in people who can bring visibility and credibility to your company”. Focusing on these people is a sales channel by itself, and a Founder has to be involved in building that channel when it shows glimmers of hope. The Minjar story had a happy ending, because they invested more time in building their PSP relationship and limiting other marketing activities: they did not spread themselves too thin. This involved multiple operational changes like training, presenting thought leadership & co-selling at conferences, and making sure the end users at the PSP are successful in using your product. It is also important to note that a partnership is not a reseller or transactional relationship. A partnership is a relationship of strengths, in which each entity brings unique skills and together provides exponential value to the end customer. Partnerships work when you have champions leading on both sides of the table and one of the best outcomes a PSP can provide to a startup is a strategic acquisition. A PSP is one of the best ways for a startup to exit, especially if you have not raised a lot of capital.

At Tagalys we have tried to develop relationships with PSPs; twice, and we seem to be making good progress today after one failed attempt. My learnings resonate with Vijays’ and some of them are

Persona: Not every large enterprise, who might also serve your target customer, is a valid PSP. An enterprise is an ideal PSP if the value you provide as a startup is something that can be incorporated into the product or process of the Enterprise, and without which the end value of the enterprise depreciates. If your startup is not important to the customers of the PSP, then they are not a match for your startup.

Timing: In your early days, a startup needs to focus on customers, customers and more customers. A PSP is likely to work with you only if you are part of the affordable loss for them. Very early in your stage the risk is too high for the PSP to consider the relationship an affordable loss. Remember, you are adding value to the PSP, hence any risk in the value proposition you bring to the table, is a risk to the end customer. Only after having proven your value to your own customers, will a PSP be willing to take you to their customer.

Credibility: Today, Tagalys works with many recognizable customers in the country and that makes the process of gaining credibility & trust easier. Your product is only as good as what your customer says it is. For a PSP to work, you need buy in from stake holders like the CEO, CTO & Product Managers and they are going to put their neck on the line if they can trust you. Customer references are the best channels to gain trust.

Lifecycle: As CEO, I have time to invest in meeting with various stakeholders at the PSP because our product is in steady state. This steady state of the product is theright time to speak with a PSP because your team can take on this additional responsibility. We also have a clear understanding of our expected outcomes, risks and upside in working with the PSP, hence our conversations are well guided and makes the discussion very productive.

Bill of Materials: While Tagalys is a line item in what the PSP provides to the market, we are an important line item who can potentially extrapolate the end value provided to the customer.

Not every startup can find a strategic partner, but one thing is for certain, as Vijay said, “You miss 100% of the shots you do not take”.

Antony Kattukaran is the Founder & CEO of Tagalys. Tagalys is a merchandising engine for online retailers, dynamically predicting what products to display across search & listing pages to increase conversion.

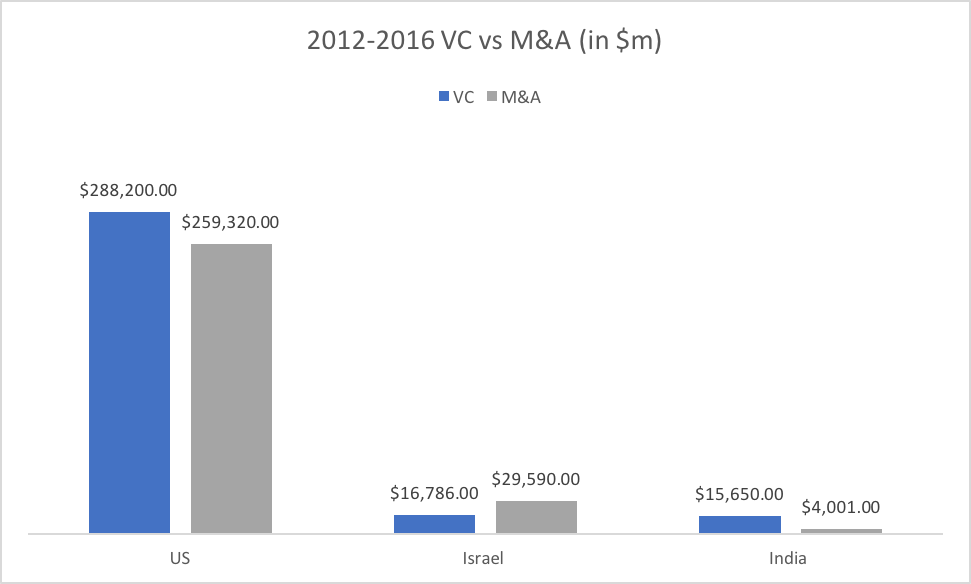

Recently was having a conversation with a Private Equity friend and was trying to explain the challenge that has captured my imagination and full attention, ie exits for software product startups in India. He felt that the data about the exit structural deficit that I was trying to point out felt too bearish to be true. My counter argument was that my intent is not to sound bearish but instead be a realist, after all acknowledgement of a problem is first step to solving one. Post that conversation I thought should put this data out publicly so that through crowdsourcing can at the very least improve my understanding if it is off by wide margins.

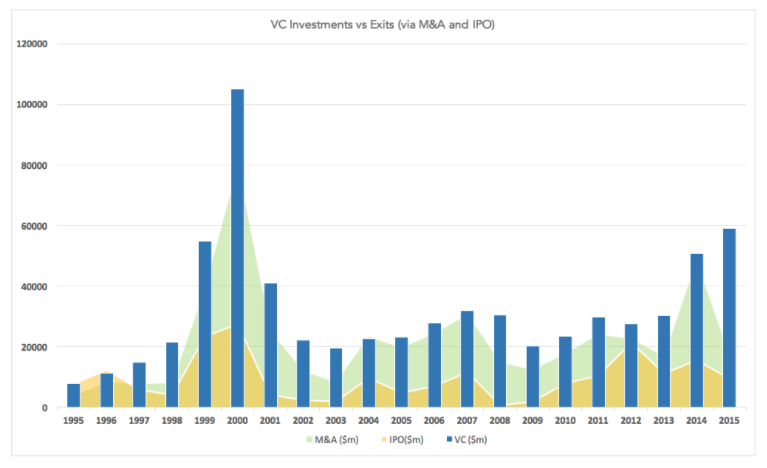

Above data indicates that Israel was able to generate 1.8X of the money that went in while in India in the same period it was 0.2X. The right comparison is exits from 2012-2016 with VC investments from 2005-2009, iSPIRT report does that comparison but results are even less encouraging.

Exits follow a power law distribution, however in India it seems like a power law’s power law.

Not only is the volume of exit a challenge but also the structure, any ecosystem exits follow a typical power law. For every $1 bn exit, there are ten $100m deal, for every $100m there are hundred $10m deals.

Top 7 deals in India account for ~$2.5b of the $4b in exit. About 250 of 391 deals total a deal volume of $97m which means the size of an acqui hire i.e in long tail is about 0.5m, which is inadequate even for an angel investor (in other ecosystem long tail is >$10 m, hence being referred to as power’s law power law). Lack of many $10-100m deal means there is a missing middle of the long tail.

Anything in the data above that does not feel kosher ?

iSPIRT M&A Connect program takes a multiyear view to design interventions that can address the middle and long tail of the market coordination challenge.

Think about endgame, chess grandmasters do so to win.

Studies point out that chess grandmasters visualize the chess board state few steps away to a ‘winning game’ and make moves based on memory pattern that can lead to that board state and thus help them win the game.

Many startups however operate in a game where the rules are dynamic and change unexpectedly. An unanticipated flood of competition could sweep in, or the ground gets shaken underneath because of a regulation or policy change. Due to such unpredictability most of the founder’s move is extremely tactical, the focus is in on surviving and not getting killed as opposed to planning to grow like rabbits.

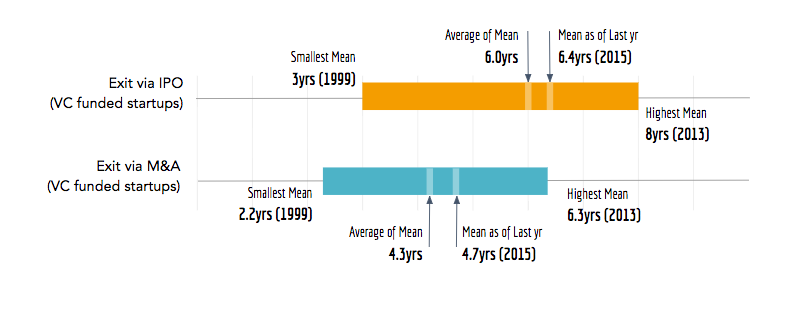

Data from 20 years of startups in US suggest mean time to exit is 4th and 6th year.

Mean exit time for startups

This is simply because If investors don’t do that then they can’t return the capital to their own investors (i.e limited partners) within the 10 year fund cycle.

Same data also reveals that after 1997 there has been more exit through M&A than IPO both in terms of count and value which means that it is more likely for a startup to have an exit via M&A rather than an IPO as the most likely route

VC vs M&A vs IPO

In India with no IPO route, M&A is the most likely endgame

On decade long VC scale, Indian ecosystem is quite young and thus historical data is not available to compare however similar forces broady apply.

Also while scale can become large but technology market growth rates in India are not as fast the US. Add to this the fact there is no IPO market in India for the technology companies. Some efforts are underway to open it such as the new ITP platform by SEBI but nothing has kicked in practice. That makes M&A option all the more important to consider for an Indian startup founder.

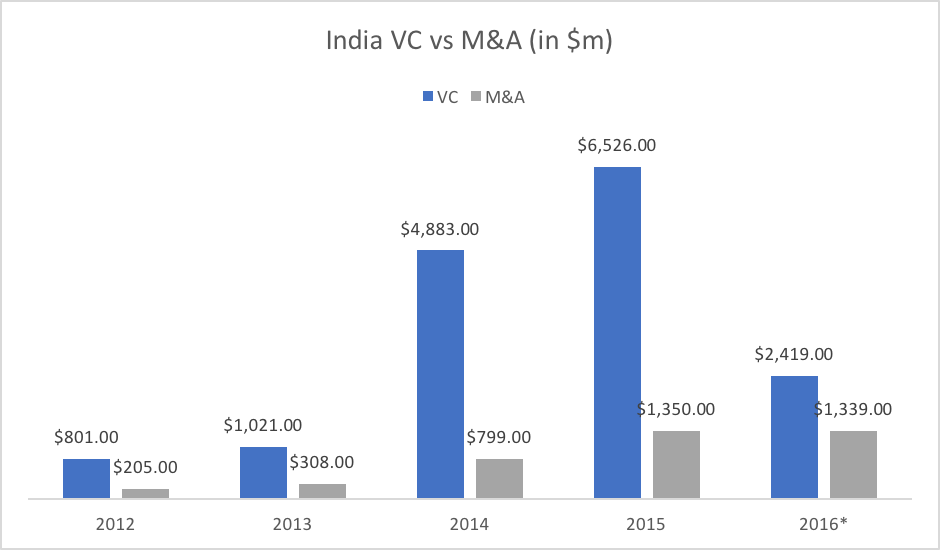

From limited data that is available about the Indian ecosystem we can that $14.5 billion of VC money has been invested in last 4 years and $2.5b of exits have happened in the same period spread over 300 deals. This ratio are still very skewed when compared to other ecosystem.

India M&A / VC Ratio – Low

All of this build the strong case for why an Indian startup founder should think about exits via M&A

A reason they don’t think about it is because they don’t know much about exits or the playbook involved in doing that. Second likely reason could be that advisors actively discourage founders from thinking about exits by labeling them opportunistic and not being a visionary founder.

Paradoxically the right time to think about exits is exactly when an exit is not needed.

Founders should think about exit before they are forced to think about it

PS: Exit has a broader significance, applies to open source and even countries. Here is a talk by Balaji Srinivasan that illustrates the importance of exit as key lever of an healthy ecosystem

Acquisition opportunities arise through design or by chance. As your company profile improves, bigger players may approach you if they perceive a complimentary relationship. That could be a large competitor, who has been losing key accounts to you. An OEM or strategic partner, who observes significant sales resulting from the partnership, may look for vertical integration.

It is also possible to plan for an acquisition once your business has reached a certain scale. The points made above can work in reverse – you can judge which competitor, partner or someone in an adjacent space can benefit from acquiring your product. As part of your roadmap, you can then align your positioning, offerings and client base to be complimentary. By winning deals with some overlap in clients, you can work towards some kind of sales, SI or OEM relationship. After creating a network of senior level contacts inside that organization, you can make an overture for a strategic investment or outright acquisition.

The first contact must be at a high level, preferably CEO, directly or through trusted contacts. Once initiated, an M&A negotiation proceeds like an investment deal. The acquirer has to find your product, leadership team, client base, current revenue and growth potential attractive. You must be convinced that the buyer is the right one in terms of business prospects, culture, and management team.

Negotiations have to proceed in strictest of confidence. The risk is higher for the smaller company – any leak can impact market confidence in your future if the deal falls through. After signing a mutual NDA, both sides share high level revenue and profitability numbers. You may have to part with much more information than the buyer if you are much smaller. Get clarity on mutual synergies in clients and products and future combined roadmap. M&A makes sense if 5 and 2 can result in something more than 7.

The first one or two meetings are usually decisive. It is quickly apparent whether both sides have a similar vision and share similar values. Cultural fit can make or break the deal. With two CEOs used to having their own way, a lot depends on their rapport. M&A deals have fallen through because of ego issues between leaders.

If there is good business synergy, the acquisition amount and terms are discussed. Once there is a handshake on valuation and broad merger principles, a term sheet is signed.

In M&A too, the buyer will assign a team to verify all claims, do customer checks, and examine potential risks or liabilities related to tax, loans, IP, client defaults etc. Any major risks or liabilities discovered during this review can result in the deal falling through or change the valuation. If all goes well, both sides work on a comprehensive agreement to conclude the deal.

For about 2 hours in the RoundTable session, the intense discussion was centered around how to be ready for M&A. Buyers, who have an interest in your company will ask about your product, your markets, your customers, your revenues. As an Entrepreneur, what is your first ask in return? Usually they are any of the following. What will the buyer pay us? Is this the right time, should we wait for a better valuation? What will the buyer do with us post acquisition?

Jay Pullur, CEO, Pramati Technologies, helped us realize, that the first question should be, what will our company do for the buyer? What is the fitment of our product or solution in the buyer’s vision? You need to ask and most importantly answer this yourself. Don’t expect the buyer to answer this, if you are, then you are not ready for any deal. It was a moment of epiphany. Fellow Entrepreneur, the first step to readiness for an M&A is to ask, what your product does to the buyer’s company, not what the buyer can do for your company.

Four hours of entertaining stories by both Jay Pullur, Pramati Technologies and Sanjay Shah, Invensys Skelta, 12 companies and about 20 participants got the opportunity to interact and learn many of the wise nuggets from these industry leaders. Not all elements of the session can be reproduced here, but below are some of the key highlights and learnings.

Wise Nuggets – Its all about Knowing (see below for details)

Wise men plan ahead. The pain or the gap that your company addresses should itself be strategically planned. Positioning your entire company, like a pretty bride will ensure the suitor will come. According to Jay, technology buyers in the US do several acquisitions in a year, so for them its just another transaction, they are not emotional about it, not attached to it, its just their job. So the interests of the suitor should always take precedence, otherwise the suitor will move to the next company on the list. Sanjay added that using an iBanker to help you in the match-making process or to source the right type of buyers is also a very beneficial activity. To sum it up, like for any Sale, Seller has to make it absolutely comfortable and easy for the buyer to buy. The checklist includes, but is not limited, to the following.

Know or Define the right fitment (addressing the GAP in the buyer’s arsenal is most important)

Know your Position (be clear on the landscape and position your product very clearly)

Know when to exit (constantly guage the pulse or the sentiment of both the market and the buyer, macro-economic conditions can play havoc, sense the weight of an opportunity)

Know your Buyer’s problem – Demonstrate that you know the Customer’s Exact Problem (POC, Story boarding the Pitch and strategy all come into play)

Know your Product (Don’t use flowery language and adjectives- show the customer, you are only solving a pain – which is not a glamorous job to do)

Know your Buyer – Gauge the buyer’s impending need to buy (They will usually reciprocate with the same rigor as you)

Know the Competitors, their strategies, their features, their benefits and most importantly their weaknesses.

Know your-self (You know that you have built a rocket or a rickshaw – if you are in a rocket, you should be on-top of the short-list)

Know your price (indicative pricing is most important – make sure all research leads to a best possible quote)

Know how to close (all the criteria for success should be met, there is no alternative for preparation and effort)

Know your readiness (systems/processes for closure, like record-keeping, employment contracts etc)

Know what the deal entails (who brings the deal – may be an iBanker, upper thresholds, lower thresholds, etc)

Know your Organizational structure (are you are platform, are you embeddable, do you need domain expertise)

Know the parties and their motivations (Eng Team in California v/s CFO in London – who is the deal maker, who is the deal breaker)

Know the term-sheet (if not hire legal guys or ibankers who can help).

Insights and Learnings

There were many learnings, which definitely are tied to the personal experiences. Some of the key ones are

When Jay sold Qontext to Autodesk he found them to be extremely professional and did not find any price penalty, or discrimination, because of the Indian-ness of it. In fact, he was able to sell it for a very good multiple. The best valuation/revenue multiple silicon valley companies to could get. So its a myth to think that a technology product from India, might get the raw end of the deal.

When Sanjay sold Skelta to Invensys, he understood the weight of the opportunity. Even though the conversation was not intended for M&A, both parties realized that its mutually beneficial to do so within a couple of hours of conversation.

Sanjay’s additional advise, raise adequate money at a comfortable time, and continue to stay relevant via media briefings, etc all the time.

Other general learnings were also discussed. To note a few,

Learn about Earn-outs, ESOPs, Liquidation Preferences (Be real to scale)

Invest if you have clarity on Exit (do everything possible for the deal to come to a fruition, POC, be aggressive, call the CEO if needed)

Learn about Black duck tests, acqui-hires, escrows for indemnification, etc.

Define the outcome post M&A and get consent.

Conclusion

Overall M&A stands for all your Moves & Acts. Its all about the Story, your clarity of all the characters and props in the story, and their acts. Commercial success is most important, direct accordingly. Re-takes’s are possible, in-fact easier provided you make your first venture successful.The hilarious moment and the most catchy line came from Jay. Someone asked about honesty and truth, during the process of due-diligence, for which Jay laughingly said, “Tell the truth with such conviction, that the buyer will lie to himself”.

It is a typical Monday 9 AM! Ready to kick-start another challenging week! Fine day in Chennai !! Not so hot like a typical Chennai climate. But, for first generation entrepreneurs it is an ordeal to pass thru weekly pressures of Cash flow, Attrition, New business and opportunities etc. etc. This experience is collectively described as “Monday Morning Blues”.

The growth dilemma

There has always been a great dilemma for entrepreneurs during fund raising exercise especially when it comes to taking the company to the next level of growth. The dilemma does not stop by simply raising the money for growth, but it goes on till such time one is able to strike a balance between how much stakes to dilute and the tangible benefits that the venture will get.Then comes the business and revenue models. The previous eras have brought countless innovations in the theory and practice of running businesses. Many are now staples of contemporary management, but others were ephemeral distractions that led companies down the wrong roads. Too often, leaders have sought the appearance of success rather than its reality – size for the sake of size, book-keeping profits as opposed to intrinsic value, earnings growth manipulated to please the stock markets. This era’s changes are already redefining management theory and practice. Raising competitiveness intensity forces a return to basic again. Going down to basics today means first and foremost focusing on how you can create intrinsic or fundamental value for your business. Your ability to create fundamental value rests on how good you are at finding the right balance between your external and internal realities and your financial aspirations; in other words, how skilfully you develop and use your business model. The major reason to focus on the fundamentals is that growth won’t come easily. Organic growth will not often produce the double-digit gains that were routine and even obligatory in the last era.

Leaders who hope to grow their way to success through mergers and acquisitions in the present market scenario are left with umpteen no of options. Needless to mention that M & As promises to increase economies of scale and yield efficiencies from synergy – or at least show the kind of revenue growth that looks like progress. And some players thrive by picking up battlefield causalities on the chips and hammering them to shape. Many people viewed General Electric’s acquisitions in the late 1980s of troubled RCA as a misconceived diversifications ploy. But after selling off RCA’s consumer electronics and aerospace businesses, GE wound up with NBC for a song, turned it around and went on to build it into a network powerhouse. NBC generated significant profits year in and year out, and with the addition of Vivendi Universal’s entertainment assets which greatly helped GE’s future growth.

The courage to change

Many first generation entrepreneurs lack with the intelligence to recognize that they have reached a crossroad but don’t follow through and head down the new path. Their inner core isn’t tough enough to allow them to acknowledge and deal with an unpleasant reality, whether it is closing a loss making division or taking realistic look at the business model and tweaking to market expectations. Many would like to continue in their comfort zone of their familiar managerial routines and protecting their pay checks. They may be afraid: change means taking risks and taking risks raises the possibility of failure. The fear failure occupies most of entrepreneur’s growth dilemma of raising money, divesting their stakes and working under a different management culture.

These entrepreneurs often don’t recognize that failing to make a shift can be riskier than making none. The entrepreneurs who have the appetite for tough actions have the inner strength. They are willing to look at clearly at the business model that has been highly successful and is no longer relevant.

To raise funds for growth or get merged is a difficulty and at times too difficult to get consensus from founder/ promoters. This leaves the emerging organizations with fewer options such as the following:

Tag along with a bigger player and pitch for bigger contracts – on a case-to-case basis

Dilute promoters’ stake heavily and raise money from PEs or VCs at the cost of losing control of the company in your eyes and also not knowing the business outcome after fund infusion

Be a captive IT Partner for a big group and get acquired by them eventually once a decent value is built. The flip-side to this approach is that one does not know the time it will take to realise decent value

The current era of business offers promising option than the usual organic growth for entrepreneurs.

M & A – The most preferred option to grow in uncertain times

While an acquisition may have higher risk of failure than any other expansion strategy, it also provides a much superior return profile in comparison to organic growth strategy. M & As is intrinsically risky and predicting the aftermath of any acquisition is almost impossible. The fact remains that predicting the aftermath of any business plan execution is also an impossible task. But there are learnings from the past that can mitigate the risk of failure. Most M& A s fail due to inadequate articulation of two key enablers of a deal: transaction management, which is all about paying the right value, conducting a thorough due diligence and appointing the right transaction adviser; and integration management, which is about devising a detailed integration strategy ahead of the buy decision to keep the rationale of the acquisition intact. The fact of the matter,however is that any corporate strategy can go bad despite putting safeguards against any possible fallout in future. And so can simple business decisions related to marketing and research and development will lead to unpredictable business outcome.

If there are precedents where shareholders’ wealth has been written off as fallout of ill-planned M & A, there are more than a handful of cases in history through well executed M & A strategy that delivered immense value to share-holders:

IBM’s market value of USD 227 Billion has been created virtually through acquisitions. It has acquired 187 companies since 200 for about USD 200 billion

SAP has made 5 major acquisitions since 2001 for a whopping sum of USD 20 billion to reach its current position of Euro 17 Billion

Cisco built the current sales turnover of USD 47 billion from USD 4 billion in 1996. Cisco has acquired more than 450 companies since its inception. Cisco’s fundamental growth strategy has been M & A

GE has acquired more than 18 companies since 1952 ranging from Aerospace, Process Industry, Financial Services , Healthcare for whopping sum of USD 14 billion to reach its current revenue of USD 150 billion

Exxon Mobile, It is what today on the back of a merger between two energy giants which clearly didn’t happen without the risk of failure in 1999. Exxon Mobile has surpassed Apple’s market cap and reached the USD 385 billion in April 2013.

Maersk has acquired P & O Nedlloyd in 2005 to create one of the largest shipping lines in the world.

P & O and Nedlloyd were merged together in 1996 which was yet another record in the history of shipping lines.

It is all about convincing the company’s management on the risks associated with a strategy like M & A on the back of statistics of successful transactions.

The entrepreneurs who are looking at raising money must do the following reality check and decide whether M & A is an option.

Research and evaluate your competition

Measure share-holders value year-on-year and see whether it is increasing

Your ability to raise funds and offer significant returns within a short period of time e.g. 3 years to 5 years

Ability to devote time on innovation and offer more customer value

The IT/ ITeS industry are moving towards consolidation and better economies of scale and efficiencies.The market is swamped by competition and the technological advancements are determining new way of delivering customer value. Therefore, IT services companies have to seriously consider M & A as their growth strategy to protect investor’s wealth, IP, customers, business.

Guest Post Contributed by Rangarajan Sriraman. The views expressed in this article are personal. The author is a serial entrepreneur, mentor and strategic advisor to start-ups in IT and ITeS segment based in Chennai and has been involved in 2 start-ups so far from the concept to execution stage and later on successfully exiting.

I made 18 connects out of which 11 are of extremely high value. (Aditya, CEO @FirstHive, May 2019)

I made 18 connects out of which 11 are of extremely high value. (Aditya, CEO @FirstHive, May 2019) We have connected 45 startups to Fortune 1000 corporations and in the process catalyzed $200M+ of value in terms of PSP (potential strategic partnership), customers and M&A. (Manu Rekhi, Inventus Capital & Startup Bridge)

We have connected 45 startups to Fortune 1000 corporations and in the process catalyzed $200M+ of value in terms of PSP (potential strategic partnership), customers and M&A. (Manu Rekhi, Inventus Capital & Startup Bridge)

I went from first discussion into pricing in one week with a Fortune 10 company. Getting in front of the decision maker is all the difference. As a founder/CEO I can close the sale without the long drawn out sales process. (Sanjoe Jose, CEO @Talview, May 2019)

I went from first discussion into pricing in one week with a Fortune 10 company. Getting in front of the decision maker is all the difference. As a founder/CEO I can close the sale without the long drawn out sales process. (Sanjoe Jose, CEO @Talview, May 2019)