iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

iSPIRT is pursuing the Stay-in-India Checklist 2.0 with Department for Promotion of Industry and Internal Trade (DPIIT), Government of India, targeted to bring Ease of Doing Business for start-ups.

Our efforts gained momentum with DPIIT’s Regulatory Roundtables since August 2022. Reserve Bank of India has further eased the reporting of FDI on the FIRMS portal. The item was on the list of issues that were taken up with RBI through DPIIT.

The new announcement called “Foreign Investment in India – Rationalisation of Reporting” has been announced vide circular no. RBI/2022-23/160 A.P. (DIR Series) Circular No. 22 Dated January 04, 2023. Please visit the RBI site on linked here.

The announcement is expected to further ease the reporting of the foreign direct investment received.

Details of the Reform Measure

In its effort to tout India as an attractive investment destination, the Reserve Bank of India (RBI) has released the RBI/2022-23/160 A.P. (DIR Series) Circular No. 22 on 4 January 2023, which brings about certain reforms in the reporting process in the Single Master Form (SMF) on the FIRMS portal. The SMF is a form which integrates the reporting structure of various types of foreign investment in India. It has implemented the following changes with respect to reporting in the SMF on the FIRMS portal:

The forms submitted on the portal will now be auto-acknowledged with a time stamp and an auto-generated email will be sent to the applicant. The AD banks will have to verify the same within 5 (five) working days based on the documents uploaded.

The system would automatically identify a delay in reporting if any.

For forms filed with a delay of less than or equal to 3 (three) years, the AD bank will approve the same, subject to the payment of LSF.

The LSF will be computed by the system, and an e-mail will be sent to the applicant and the concerned Regional Office (RO) of the RBI, specifying the amount and the timeline within which the LSF is to be paid to the concerned RO.

Once the LSF amount is realised, the concerned RO will update the status in the FIRMS portal, and the updated status will be communicated to the applicant through a system-generated e-mail, which can also be viewed in the FIRMS portal.

The AD bank will approve the forms filed with a delay greater than three years, subject to the compounding of the contravention. The applicant may thereafter approach the RBI with their application for compounding.

The remarks of the AD Bank for rejection of forms, if any, will be communicated to the applicant through a system-generated e-mail and the same can also be viewed in the FIRMS portal.

The resulting effects of the RBI circular

1. Auto acknowledgement of SMF

While the rationalisation of the reporting process is a welcome move, and the auto acknowledgement of forms will bring comfort to the applicants after filing the form, we are receiving mixed reactions from stakeholders with regard to the verification of the forms submitted by the applicants within the 5 (five) working day window. Given that there are no overarching guidelines on the format of documents required for filing Form FC-GPR and Form FC-TRS, and the format differs from bank to bank, it may be helpful if banks were to consider offering pre-vetting services in relation to reporting for cross-border transactions.

The likely result of an AD bank not approving the form within 5 days will be auto-approval of the form.

The circular is silent on what happens in the event an authorised dealer (Bank) isn’t satisfied with the details. It seems, in such an event, what could have been approved with a few follow-up queries will have to be rejected within the 5-day window, if the queries remain unanswered.

Separately, we also believe that a 5-day window is very short given the complexity that can arise with some filings. Banks and their regulatory teams also usually work only till 5:00 PM (and cannot, in any case, be expected to work 24×7), so if a form is submitted close to or after 5:00 PM, an applicant may already have lost close to a day.

2. Online calculation of late submission fee.

Auto-identification of a delay in reporting and calculation of the late submission fee (LSF) by the system will likely be greatly appreciated by stakeholders. Prior to this reform, if an applicant received an email from the RBI regarding the LSF, the applicant would have to draw a demand draft in favour of the RBI, which would have to be acknowledged by the RBI through email. While the process was efficient and hasn’t changed post the amendment, there have been multiple instances of applicants not having a record of the acknowledgement with them after a few years, either due to: (a) IT policies of the organisation which delete older emails; or (b) due to a change in employees. Now that the concerned RO of the RBI will update the status on the FIRM’s portal (along with the standard email process), the amount will be reconciled and the LSF can be viewed on the portal.

Disclaimer: This blog post is co-written by Tanuvi Thakur of iSPIRT and Sanjay Khan of Khaitan & Co and is meant to inform about a new announcement by the regulator. It should not be considered as advice.

At the Fourth National Startup Advisory Council Meet held on 17.05.2022 under Hon’ble Minister of Commerce and Industry, Consumer Affairs, Food & Public Distribution, and Textiles Shri Piyush Goyal, the NavIC Grand Challenge (GC) was launched. The GC seeks to mainstream the use of NavIC and establish it as a domestic mapping solution.

iSPIRT has contributed to the development of this Grand Challenge. During the Third NSAC Meet, Sharad Sharma, Co-founder of iSPIRT and a member of the National Startup Advisory Council (NSAC), proposed the concept of prominence to NavIC as a domestic mapping solution.

Later, the iSPIRT Team, led by Captain Amit Garg and our volunteers Sayandeep Purkayastha, Captain George Thomas, and Tanuvi Thakur, presented the concept note and working paper on the GC to DPIIT (Dept for Promotion of Industry and Internal Trade).

Multiple rounds of discussion among the Department for Promotion of Industry and Internal Trade, Indian Space Research Organisation (ISRO), and iSPIRT Foundation brought the final shape to the working paper. All of this culminated in the launch of GC-NavIC on the 17th of May.

What is NavIC?

NavIC or Navigation of Indian Constellation is India’s independent regional satellite navigation system created by DOS/ISRO. Its signals are inter-operable with the civilian signals of the other navigation satellite systems namely GPS, Galileo, Glonass, and BeiDou. NavIC has made in-roads into civilian applications in India like vehicle tracking, power grid synchronization, location-based services (using mobile phones), disaster alert dissemination, etc. Efforts are being made to enable the incorporation of NavlC into drones, the maritime sector, wearable devices, time dissemination, geodesy, etc. The applications are being promoted by the availability of NavlC-enabled off-the-shelf chipsets & devices at competitive rates and by the adoption of NavlC in national and international industry standards.

The GC is a step towards taking NavIC adoption further into the future, i.e. the future of AtmaNirbhar Mapping Solution. The GC brings together the triumvirate of NavIC, Agriculture, and Drones by becoming a big-bang thrust for the Kisan Drones Project as well.

The GC-NavIC

The GC-NavIC has an intersection with GOI’s Project Drone Shakti. It seeks to promote:

The use of drones to solve the problem of agriculture insurance, i.e., the integration of the product to solve cases under the Pradhan Mantri Fassal Bima Yojana, is in line with the Government’s steps to harness technology for agricultural growth;

Building a digital database of agricultural data that will supplement the digitization of land records and crop assessment measures of Drone Shakti;

The use of ISRO’s homegrown NavIC technology in developing drones under the GC will promote the use of NavIC in the commercial drone landscape for remote sensing, imagery, mapping, etc.

The GC has invited innovative solutions that will utilize NavIC-enabled drones to capture data related to farm field topography, process this data, and make it available for use for commercial purposes. Ideas should be such that the product can be deployed across all terrain types in the country. Further, the captured and processed data should be viable and efficient for use within the Pradhan Mantri Fasal Bima Yojana (PMFBY) framework.

A detailed application process (here) calls for a detailed proposal of the tech specs of the participants’ product solution. This will be the basis for 25 participants selected for a presentation of their product before the Experts Panel. 7 selected participants on the basis of an objective and transparent selection criteria will compete in Phase 1 of the GC – the prototype deployment stage. In phase 2, the top 3 participants will compete towards fulfilling the problem statement by deploying their fully functioning product.

Transformative Powers of Challenge Grants

Challenge Grants have transformative powers and scalability opportunities that can serve as an impetus to quality innovation. Treatment Adherence for TB was the first challenge launched under the Grand Challenges in TB Control program. The aim was to devise solutions for improving tuberculosis screening, detection, and treatment outcomes. One of the participants, 99Dots, came up with a novel solution for low-cost monitoring and medication adherence program by using a combination of basic mobile phones and augmented blister packaging to provide real-time medication monitoring at a drastically reduced cost. By 2017-18, 99Dots was used across all districts in India and is now listed as a treatment program on the Government’s Nikshay portal.

The GC-NavIC through its intersection with Project Drone Shakti and the revamped operational guidelines of the PMFBY that emphasize tech-based solutions will help harness technology for agriculture and create opportunities for commercial utilization of NavIC. The recent ban on foreign drones by the Government will move the focus to domestic manufacturing. Encouraging local drones with local technology will increase the AtmaNirbhar potential in the drone and navigation ecosystem and enable Indian Startups to unlock the $5 billion drone market.

Conclusion

The GC-NavIC is touted to deliver three essential outcomes – better regulations in the drone and mapping space, ecosystem development, and channel of public money for private innovation. All three will lead to transformative innovations that will push India into modern agricultural practices and domestic mapping-navigation solutions.

The post is authored by our volunteer fellow, Tanuvi Thakur. She can be reached at [email protected].

India has made rapid progress in digitisation of the economy in the last decade becoming a world leader in identity systems, digital payments and tax, and a new data sharing and empowerment framework. However, many deep-rooted issues still exist, such as extending true financial inclusion; formalisation and creating a higher trust economy, that is essential for growth of mostly small businesses.

In this blog post, we look at innovations in blockchain, distributed ledger and other technologies such as zero-knowledge proofs as potential solutions to build a stronger fabric for the economy for decades ahead. The unique opportunity India has is to boost commerce by enhancing trust, thereby culminating the transformation already underway through existing building blocks of digital identity, payments and data sharing to boost commerce. Unlike many other countries, faster and interoperable payments or reducing the dominance of private money are solved problems for India; the missing piece is to digitise commercial contract enforcement, which on the other hand is a solved problem for developed countries. Lack of adequate contract enforcement caused by contracting parties having different versions of the truth; due to data systems that don’t interoperate reduces trust and creates friction for economic growth. Solution requires connecting the goods and services ledger to the money ledger, so that contracts of any kind become binding promises that can be executed programmatically. Using technology to solve this trust problem is a unique opportunity for India.

BADAL (also happens to be a word for Cloud in local language), a techno-legal solution in the form of “Distributed Ledger for Privacy-preserving Trustful Commerce; is proposed as an interoperable fabric underlying a future programmable economy across large and small businesses to create high trust economy.

We also look at the emergence of Central Bank Digital Currency (CBDC) which is one of the core money applications of this framework and global backdrop in Annexure. There are many other use cases being proposed from land records to decentralised clinical trials for blockchain and allied technologies in different areas of government and business1https://www.meity.gov.in/content/national-strategy-on-blockchain likewise, that can be implemented in BADAL.

First of all, why is trust important?

Trust is the basic glue that connects strangers and promotes economic activity. Money is the basic economic institution in a society building that trust2https://press.princeton.edu/books/paperback/9780691146461/the-company-of-strangers. However, trust builds slowly due to a combination of various factors such as the nature of institutions (political and legal) and the level of formalisation. While formalisation of even small businesses is increasingly addressed by the successful rollout of GST for India, formalisation of trust still remains elusive. At a core fundamental level, trust is a public good that creates friction-free commerce and is a recipe for rapid economic growth.

There is a high correlation between the level of trust in society and GDP per capita3https://ourworldindata.org/trust-and-gdp. A study conducted by World Value Survey attempted to measure the level of trust in a country by recording the positive responses received to the question ‘most people can be trusted’. It found that countries with high GDP per capita such as Sweden, Norway and Netherlands recorded high levels of trust exceeding 60% determined in this manner as the graphic below shows.

Douglass C. North, Nobel laureate in economics4https://www.nobelprize.org/prizes/economic-sciences/1993/north/lecture/, found that ‘the inability of societies to develop effective, low-cost enforcement of contracts is the most important source of both historical stagnation and contemporary underdevelopment.’ The Union Minister of Finance and Corporate Affairs has rightly acknowledged the role of the “Hand of Trust”5https://pib.gov.in/PressReleasePage.aspx?PRID=1601273when presenting the Economic Survey of 2019-20.

In societies like India, with limited ability to efficiently enforce routine civil or property contracts, businesses tend to restrict working with those similar to them based on caste, religion etc. (called associational activity) where there is an implicit social and moral enforcement mechanism or with members who have clearly demonstrated reputation in the past (usually the large or the older players). In both these situations, the economic benefit that a new firm can bring with new ideas or new techniques will be muted as its absorption is slower. Similarly, a new player will find it very difficult to compete with incumbents even if such players are economically more efficient. Economist Olson6Olson, M. (1974). The logic of collective action. Harvard University Press showed that associational activity is often more detrimental than favourable for an emerging economy. So we need better ways to break this trust logjam. Trust in the money system in India is comparatively high, as promises tend to be kept with sufficient legal backing and can be digitised with e-mandates or automated payments/ collections; but the same is not the case for goods (or services) ledger, leaving room for delays cascading into a logjam resulting in low trust. This is often felt in day to day life by citizens not getting routine services despite advance payment or small businesses not getting paid despite having supplied goods. Delays, defaults and disputes can become the norm if parties have different versions of the truth.

Every economic activity is thus like a mini-contract with one side on the money ledger (payment from party A to B) and the other side, on the goods/services ledger (from B to A) between counterparties, and can be converted into an electronic contract that automatically executes on both ledgers subject to interoperability. To assure the performance of contracts, the money ledger and the goods/ services ledger need to be connected in a way that is scalable, privacy-enhancing, non-repudiable and programmable. This enables a contract agreed between parties becomes a commitment, and fulfilment is guaranteed by code through the electronic contract. Assuring performance of contracts is critical for a country that is seeking to grow through startup activity, not just in tech but other sectors too.

Currently, litigants lose nearly ₹ 50,000 crores annually in wages or business lost which comes to 0.5% of the country’s GDP, because of litigation, an indication of how expensive litigation can be. The majority of civil disputes in courts are related to recovery of money (30.2 per cent) and land-or property-related matters (29.3 per cent) As reported in the 2016 survey carried out by DAKSH. Common reasons for dispute are different versions of the truth of contracting parties, prior to contract (past) or during the performance of contract (future). Having the same truth and programmability inherent in electronic contracts is a boon in this regard.

In an earlier blog, we have explored the benefits of adapted blockchain technologies to solve the problem of SME financing in India with a related post by global experts7https://balajis.com/add-crypto-to-indiastack/. We build further on that and believe that India can harness recent advances associated with blockchain technology to enable trust between unrelated parties by combining the best of the scalable and centralized legacy world with a secure and private decentralized world. This can benefit the real economy vastly along with the financial world.

Innovations in distributed ledger technologies and BADAL

Distributed Ledger technology can help in two ways – first by being able to verify past performance before one party strikes a deal with another, and second, by being able to enforce a contract in most situations as performance unfolds in future. Thus, building trust about the past as well as the future.

We thus imagine a fabric based on the following basic principles to help create and grow a large number of applications to record economic activity even while reconciling with other activities and past data and help inject a level of trust by creating a reliable, immutable record of trusted data records and programmable contracts

Single platform to allow standards bodies and organisations to publish their schemas, and reuse other schema elements in composing workflows

Fully privacy-preserving capabilities to allow participants to publish relevant zero-knowledge proofs which do not require private data to be shared beyond the participating entities

A programmatic contracts capability that can help automatically carry out the relevant tasks as agreed on without any further manual intervention

By connecting a new digital money ledger (such as Central Bank Digital Currency, or stablecoins) with the new goods & services ledger, we envisage a boost to trust across economy and commerce. As such, BADAL is the first such framework we are aware of globally, uniquely suited to India’s needs, opportunities and strengths.

We have discussed the early version of this in detail in an earlier open-source document8https://github.com/iSPIRT/ppl, called Public Private Ledger. BADAL is thus a privacy supporting, trust enhancing mechanism of coordinating economic activity, and information recording and sharing. Originally this group started out of a process to explore the domain around and figure out the appropriate model to support CBDC, support data sharing between participants, and coordination and automation of event-based standing instructions across events in the goods and services ecosystem and/or money flow.

We then reviewed exciting developments in related areas first to understand their relevance given India’s unique needs. Blockchain technologies generally are seen to enable unrelated parties to trust each other and transact without depending on a central institution or intermediary. These technology innovations are around three key areas:

Maintaining immutability and integrity of data across the distributed ledgers of parties.

Governance mechanisms, especially for decentralised networks

The programmability of such transactions to allow automatic execution.

Public blockchain technologies like Bitcoin and Ethereum, on the other hand, are based on a philosophy of distrust of centralised institutions like Central Banks and are designed for unrestricted access and decentralised decision-making. But they have had to develop new approaches to contend with a few challenges, especially given the huge growth off late that see further wor:

The enormous consumption of resources to establish ‘proof of work’ that limits efficiency and scalability, leading to newer approaches

Exposing all transactions on these networks that generally do not allow sensitive data to be private on the key layer, is as critical for confidential business data as it is for personal data

Rise of many networks that are not interoperable with each other or with the mainstream economy, though some bridges do exist

May have ability to operate outside banking conduits and regulatory frameworks that challenges government’s sovereignty and financial stability through greater oversight has been coming recently

Research on amending throughput, reducing costs and enhancing privacy/auditability/KYC compliance has been ongoing at a rapid pace, especially over the last couple of years.

Despite these unresolved issues, Public blockchain-based tokens, so-called cryptocurrencies, NFTs etc have become an unregulated asset class, especially amongst the young rapidly given the ease of use, creating concerns on possible misuse as well as potential opportunities. We were also part of the recent consultation of the Parliamentary Committee on Finance on ‘Cryptoassets: Opportunities and Challenges’ and had shared with them some of our ideas above in our submission here9https://docs.google.com/document/d/e/2PACX-1vShkuTno_bSILFZPf-Cb_KNwwgM6A_6OgyRiASNS0tXB3ViriHztovrkL7sebiAC7O54y0uwQheTdin/pub.

Various solutions have been employed to address some of these challenges:

Permissioned blockchains, such as Hyperledger Fabric and Corda, allow only trusted parties to participate. Corda uses Notaries for verifying transactions. Such solutions have been successfully used in finance, supply chain, property rights, healthcare, education and e-governance

Zero-knowledge Proofs (ZKPs) allow proving/verification of specific aspects of data without actually making the data public

BADAL builds on the above primitives and is offered as an open and interoperable platform to enable money ledgers such as CBDC/stablecoin along with applications relevant for finance and commerce. This can be designed as a permissioned network relying upon a few regulated entities, and interoperable to ensure that its benefits are widespread and at much lower costs than permissionless systems. It consists of a private ledger that holds sensitive user data withaccess restricted to participating entities only, and a public ledger that contains notarised zero-knowledge proofs about transactions between users. It supports different schemas (configurations) that enable usage across different use-cases.

This programmability coupled with immutability akin to electronic contracts, allows applications in BADAL to be used to leapfrog the trust logjam, without diluting sovereign privileges of control of money given India’s stage of development. BADAL will thus establish provenance that helps establish credibility and reputation of transacting parties, proof of title/ownership of goods and assets, proof of the history of transactions including promises made and ambiguously defined and fulfilled; automatic execution of terms of contracts along with privacy as a fundamental right.

Historically, monetary accounting has solved for only one side of this metaphorical coin- the monetary value. All monetary systems denote a money value to any transfer of goods or services. BADAL, being a ledger that can record value in any domain, solves for the non-monetary aspect of the transaction. Integrated with electronic contracts for a variety of applications, BADAL will enable digital claims on non-monetary assets, including new age asset classes such as crypto assets, NFTs, where claims can be financialized and liquidated. An inherent promissory layer can be enabled into the current transaction mechanism. This extends to all data types, from land records to hospital quality service quality etc, rather than just transactions involving money and goods/ services.

The ability to connect any of the data types across domains can give rise to massive amount of efficiency gains with automated execution thanks to new data from machines like cars, consumer durables like refrigerators or health wearables coming from advances in IoT (Internet of Things), 5G, Imagine a use case of automated crop insurance with sensors that monitor weather from a satellite in space to moisture in soil etc. and deliver claim benefit to the farmer with zero friction in real-time.

One of the biggest problems BADAL could solve at bottom of the pyramid is financial inclusion in India. This is not only in the form of increased monetary transactions through it, but also the ability for MSME’s to gain cheaper credit. This is a possibility as MSME’s will find it easier to prove their liquidity and income to banks and other lenders due to the monetary traceability the system will provide. An increased ability to prove financial stability will lead to greater leverage for borrowers and more systemic trust for lenders. This increase in the systemic trust will not only lead to an increase in credit creation but catalyse an increase in money velocity in India as a whole.

In a subsequent blog post, we will detail the potential use cases; as well as preliminary design of a prototype of one sample use case that is being built currently.

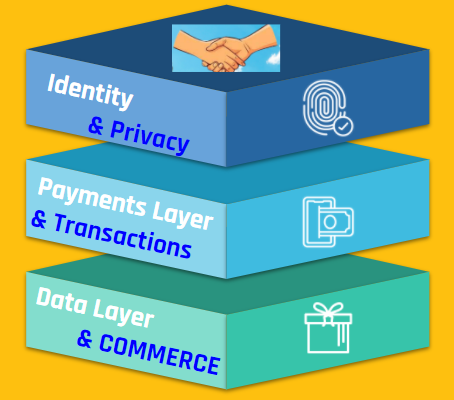

BADAL fabric supporting India Stack could boost digital India

India has pioneered transformations in Identity, Payments, and Data empowerment (these building blocks are popularly called the India Stack) through a techno-legal approach. These address friction of doing business, information asymmetry, and distributed systems. Breakthroughs along the way were public platform (identity), public protocols and standards, and techno-legal approaches to solving big societal problems.

The recent launch of the Account Aggregator (AA) model (based on Data Empowerment and Protection Architecture, DEPA) allows the controlled sharing of private financial data by citizens with various financial institutions to get the best deals. This is a global first and in some sense, an export of a truly global standard12https://twitter.com/Product_nation/status/1435997280692158464?s=20 from India.

Open Credit Enablement Network (OCEN) is creating a way to democratise access to credit, to the level of making it accessible to a street vendor for small sums. These public goods prevent any large player from monopolising the data ecosystem and at the same time reduce the cost of providing service. For instance, microloans as small as Rs.300 can be availed on GeM-SAHAY leading to true inclusion at the bottom of the pyramid.

These techno-regulatory concepts are now being considered for adoption by several countries across the world. Overall, India is arguably ahead of most countries in adopting technology for promoting financial inclusion as well13https://www.bis.org/publ/bppdf/bispap106.pdf.

Image Courtesy: Ananya Phadke

The next building block now is the trust layer through BADAL, ensuring every commitment is met and every contract is enforceable, boosting transparency and growth over the next decade. Trust permeates through all three ends of this triangle as identity is the ‘who’; and data and payment relate to ‘what’ of commerce. In BADAL, identity and data sharing can be achieved without diluting privacy to enable trusted payments (& commerce).

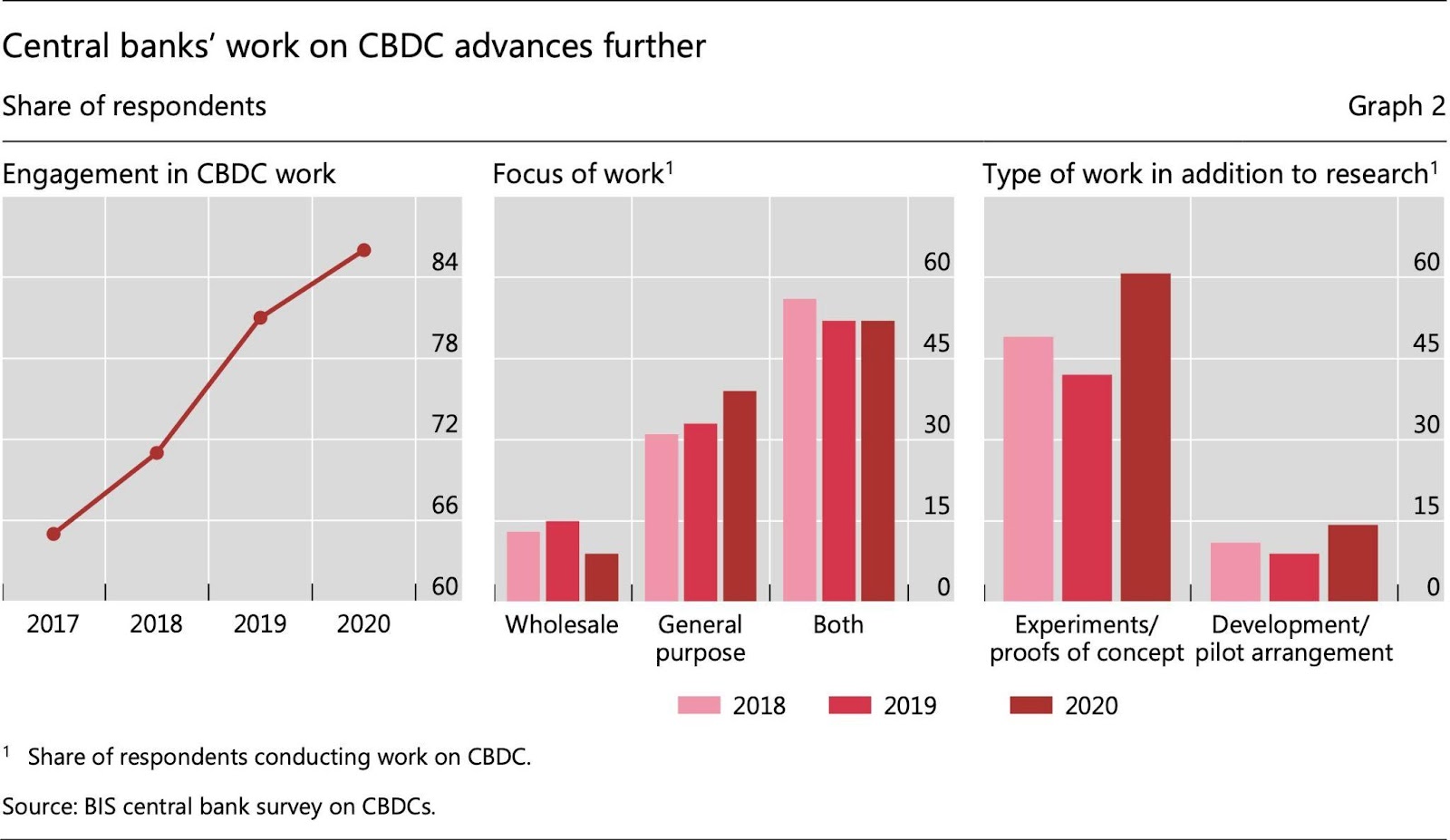

Annexure: CBDC Developments

While BADAL provides fabric to money or goods ledgers, we describe CBDC in detail here, given its importance. Money was traditionally issued by the sovereign (through a Central Banker) and circulated in the economy through layers of banking intermediaries. With the advent of permissionless public blockchains, some of which also seek to portray themselves as alternate currencies, the sovereigns have taken note and introduced their own variant as a public good to protect the financial stability of the nation-states. This sovereign/state-issued digital currency is popularly known as Central Bank Digital Currency (CBDC).

While there are different types of CBDCs such as wholesale/ retail and account-based/ token-based, ultimately a payment using CBDC can be immediately settled. This is akin to using paper money and unlike a cheque or money transfer between bank accounts that require a process of clearing and settlement adding to inefficiency and costs. CBDC can potentially thus leapfrog depending upon the development of existing banking systems in different countries.

Advanced Economies (AEs) and Emerging Markets and Developing Economies (EMDEs) have different motivations for issuing CBDC to end-users (via Retail CBDC) and financial institutions (via Wholesale CBDC), illustrated in the diagram below.

In the USA, payments are expensive due to its legacy system of banking. This has led to a burst of digital payment options, the latest being ‘stablecoin assets’ (digital currencies backed by real assets like US dollar, treasuries, etc) that also compete with their money-market funds. Stablecoin assets have crossed $100 billion25https://www.statista.com/statistics/1255835/stablecoin-market-capitalization/ in market value and are a popular choice to transact in Decentralised Finance (DeFI). DeFi is a parallel financial system evolving around crypto-assets. DeFI is not subject to transparency and compliance required in the conventional financial world at this point in time. As DeFi becomes big and interacts with the conventional financial world, there is a growing systemic risk arising from failure or fraud in DeFi. The US Government, therefore, wants to regulate some aspects of DeFI26https://www.federalreserve.gov/monetarypolicy/fomcminutes20210728.htm and may thereby bless some stablecoins and crypto-assets as explicitly permitted financial products. Earlier in 2015, Bitcoin was determined to be a commodity27https://www.cftc.gov/sites/default/files/2019-12/oceo_bitcoinbasics0218.pdf by some authorities there. The US Fed has also begun a consultation process towards design choices and feasibility of CBDC implementation.

Indian perspective

In India, the focus of policy has rightly been on promoting financial inclusion to formalise the economy and drive economic growth. One important factor which drives the usage of unregulated informal value transfer systems is the lack of banking facilities and corresponding amenities for managing money, which leaves rural communities without alternatives other than a person-to-person method of transferring monetary value. Even though India has seen a significant increase in the number of bank accounts created, Reserve bank data still highlights little improvement in account usage and institutional borrowings, which feeds into the broader issue of financial inclusivity.

Initiatives like Pradhan Mantri Jan-Dhan Yojana (PMJDY) opened doors to big change. UPI has been very successful as a payment mode but still needs underlying bank accounts to transact and thus depends on the banking system & its motivation to provide access to the poor. The PMJDY scheme announced in 2014 has increased the number of adults with bank accounts to 43.47cr 28Progress Report as on 22-Sep-21, PMJDY, MOF, GOI, https://pmjdy.gov.in/account (~46% of 93.55cr adults with an Aadhaar29https://uidai.gov.in/images/Saturation_Report_State-UT_Agewise_31-08-2021.pdf). Despite this headway, there is still a lot to be achieved. The Financial Inclusion Index (FI) recently launched by RBI shows that India is at 53.9 on March 21 (vs 43.4 in March 2017) – a little more than halfway towards complete financial inclusion (FI of 100)30https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52068. Presently, the banking system acts as the main gateway to financial inclusion as the banking system is the main distributor of cash. Hence, various government programmes (like PMJDY) rely upon banks for financial inclusion, despite those being not remunerative for banks. The accounts also have various restrictions on the number of debits/withdrawals to ensure low cost.

Even with the existence of such low-cost bank accounts, the poor do not have an incentive to use a bank account regularly as they do not save enough to use the bank account as a store of value. They use these accounts mainly to collect remittances and withdraw cash at ATMs as bulk of their transactions is in cash, not leaving a visible money trail that in turn makes financial inclusion difficult. Cash in circulation in India even now is Rs 29.38 trillion31https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52274 (~14.9% of estimated GDP for 2020-2132http://mospi.nic.in/sites/default/files/press_releases_statements/Statement_12_1st+September+2021.xls) despite the availability of these cheaper accounts, demonetisation in 2017 and the subsequent formalisation of the economy with GST, RERA, etc.

In addition, the cost of handling cash by the central bank and commercial banks (currency printing, operating currency chests, logistics of moving currency, ATM operations, etc.) has been estimated to be ~Rs 21,000 cr (Rama Bijapurkar) and ~1.7% of GDP ( (Visa Inc., 2016). High adoption of CBDC can help in reducing this cost while creating enormous amounts of data and enabling policymakers to diagnose and regulate better. At a later stage, CBDC can also be used for targeted monetary policy actions when its impact on the financial system is well understood. Experts are concerned that CBDC may result in the disintermediation of the financial system. This risk can be mitigated by following design principles set out by the Bank for International Settlements (BIS)33https://www.bis.org/press/p201009.htm (i) “do no harm” to monetary and financial stability; (ii) coexist with cash and other types of money in a flexible and innovative payment ecosystem; and (iii) promote broader innovation and efficiency.

CBDC inherently provides an alternative to cash to directly reach a customer and can complement the banking network to make adoption quicker. By providing a digital alternative to cash will enable building verifiable money trails that can lead to greater financial inclusion by private players providing customised health, insurance, investment & education products in compliance with privacy laws. In the financially excluded segments, CBDC, being a form of central bank currency, is likely to be well trusted and be adopted easily.

The blog post is co-authored by Sanjay Phadke, Dhananjay Nene, Sharad Sharma, Navin Kabra, R Barve, K Babel, V Agarwal, K Gokarn, Kalyan Narguru, Shashank B, Arun Maharajan, Karan Sirdesai, P Sahu, P Rao, A Kulkarni, Krishna Iyer, V Nene and A Lath.

If you have any queries or comments, please contact us at [email protected].

We are at the cusp of a data empowerment revolution in India. The DEPA architecture and its first instantiation, the Account Aggregator (AA) framework are empowering individuals and businesses to share their data at low cost and friction, enabling scenarios such as flow-based lending. The Unified Health Interface (UHI) is expected to drive a similar transformation in healthcare.

At the same time, we are acutely aware of the challenges that lurk, none more serious that security and privacy. With the Open Credit Enablement Network (OCEN)/AA framework, for example, a data principal can share their data instantly with many lenders, with no technical guarantees that all lenders will use their data only for the purpose of evaluating the current loan application. The upcoming Personal Data Protection Bill, increased regulation and periodic compliance audits can help detect and deter data abuse. But these measures are not only insufficient in the face of advanced, persistent threats from malicious data consumers, they increase operational costs and limit participation.

We are taking a step towards addressing these challenges by introducing a new privacy construct in Data Empowerment and Protection Architecture (DEPA) called Confidential Clean Rooms. Confidential clean rooms are hardware-protected secure computing environments where sensitive data can be processed while limiting the purpose for which it can be used. For example, lenders can host their business rule engines in confidential clean rooms, and prove to an auditor, regulator, or the consent manager that they cannot access the raw financial data, and the only outcome that they can learn is the loan offer. Confidential clean rooms are based on an emerging technology broadly called confidential computing, which is already supported by major hardware manufacturers such as Intel Corp and AMD and by all major cloud providers, and we expect this technology will mature and be commoditized over the next couple of years.

Today we are announcing the launch of a pilot to evaluate the feasibility and value of confidential clean rooms in the context of OCEN. The pilot is open to lenders, technology services providers and independent software vendors to partner with us over the course of the next year.

Please see the following open house session for more details about partnering with us and indicate your interest using the following forms by 31st of October 2021.

This is our response to the Draft Drone Rules 2021 published by the Ministry of Civil Aviation on 14 July 2021.

Introduction

The potential commercial benefits that unmanned aviation can bring to an economy has been well established in several countries. A primary and immediate use-case for drones is in Geospatial data acquisition for various applications such as infrastructure planning, disaster management, resource mapping etc. In fact, as argued in the recently announced guidelines for Geospatial data, the availability of data and modern mapping technologies to Indian companies is crucial for achieving India’s policy aim of Atmanirbhar Bharat and the vision for a five trillion-dollar economy.

The current situation in India, however, is that the drone ecosystem is at a point of crisis where civilian operations are possible in theory, but extremely difficult in practice. Because the regulations in place are not possible to comply with, they have led to the creation of a black market. Illegally imported drones are not only significantly faster, cheaper and easier to fly but also far more easily acquired than attempting to go through the red tape of the previous regulations to acquire approved drones. Thus, rather than creating a system that incentivises legal use of drones, albeit imported, we’ve created a system that makes it near impossible for law-abiding citizens to follow the law of the land and discourages them from participating in the formal system. This not only compromises on the economic freedom of individuals and businesses but it also poses a great national security risk as evidenced in the recent spate of drone attacks. If we do not co-opt the good actors at the earliest, we are leaving our airspaces even more vulnerable to bad actors. This will also result in a failure to develop a world-class indigenous drone & counter-drone industry, thus not achieving our goals of an Atmanirbhar Bharat.

The Draft Drone Rules (henceforth the draft) have addressed some of these problems by radically simplifying and liberalising the administrative process but haven’t liberalised the flight operations. Unfortunately, closing only some of the gaps will not change the outcome. The draft rules leave open the same gaps that cause the black market to be preferred over the legal route.

With the three tenets of Ease-of-Business, Safety and Security in mind, it is our view that while the intention behind the draft rules is laudable, we feel that the following areas must be addressed to enable easy & safe drone operations in India:

Remove Requirement of Certificate of Airworthiness: The draft mandates airworthiness certification for drones whereas, no appropriate standards have been developed, thus, making the mandate effectively impossible to comply with.

Lack of Airspace segregation, zoning and altitude restrictions: The draft doesn’t mention any progressive action for permitting drone operations in controlled airspaces.

Business confidentiality must be preserved: The prescribed rules for access to data is not in consonance with the Supreme Court Right to Privacy Judgement

Lack of transparent Import Policy: This results in severe restrictions on the import of critical components thus disincentivizing indigenous development of drones in India

Insurance & Training must be market-driven and not mandated: We must let market forces drive the setting up of specialised training schools & insurance products & once mature they may be mandated & accredited. This will result in the creation of higher quality services & a safer ecosystem.

Fostering innovation and becoming Atmanirbhar: A. Encouraging R&D: by earmarking airspace for testing for future drones B. Encouraging the domestic drone manufacturing industry: through a system of incentives and disincentivizing imports should be inherent in the Drone Rules. C. Recognition of Hobby flying: Hobbyists are a vital part of the innovation ecosystem; however, they are not adequately recognised and legitimized

Encouraging A Just Culture: Effective root cause analysis would encourage a safety-oriented approach to drone operations. Penal actions should be the last resort and dispute resolution should be the focus.

Enabling Increased Safety & Security: NPNT and altitude restrictions would enhance safety and security manifold.

No Clear Institutional Architecture: Like GSTN, NPCI, NHA, ISRO, and others a special purpose vehicle must be created to anchor the long-term success of Digital Sky in India based on an established concept of operations

Lack of a Concept of Operations: Although drone categories have been defined, they have not been used adequately for incremental permissions, as in other countries; rather the draft appears to prefer a blank slate approach. The failure to adopt an incremental approach can arguably be considered as one of the root causes of the drone policy failures till date in India as regulations are being framed for too many varied considerations without adequate experience in any.

1. Airworthiness

In the long term, it is strategically crucial to India’s national interest to develop, own and promulgate standards, to serve as a vehicle for technology transfer and export. The mandatory requirement for certification of drone categories micro and up is the key to understanding why the draft does not really liberalise the drone industry. It would not be too out of place to state that the draft only creates the facade of liberalising drone operations – it is actually as much of a non-starter as the previous versions of regulations.

The standards for issuance of airworthiness certificates have not been specified yet the requirement has been stipulated as mandatory for all operations above nano category in the draft (pts 4-6). However, most of the current commercial operations are likely to happen in the micro and small categories. And for these categories, no standards have been specified by either EASA or FAA. EASA’s approach has been to let the manufacturer certify the drone-based on minimum equipment requirements. On the other hand, It is only fairly recently that the FAA has specified airworthiness criteria for BVLOS operations for a particular drone type of 40kg, and which it expanded to 10 drone types in November. Building standards is an onerous activity that necessitates a sizable number of drones having been tested and criteria derived therefrom. The only other recourse would be adopting standards published elsewhere, and as of date these are either absent (not being mandated in other countries) or actively being developed (cases noted earlier). Given the lack of international precedent, the stipulation for certificate of airworthiness in the draft needs to be eliminated, at least for micro and small category drones.

2. Airspace

One of the major concerns since the early days of policy formulation in India has been the definition of airspace and its control zones. All regulations till date, including the draft, require prior air traffic control approvals for drone operations in controlled zones. However, given that controlled airspace in India starts from the ground level for the controlled zones upto 30 nm around most airports (unlike many other countries where it starts at higher levels), it effectively means no drone operations are possible in the urban centres in the vicinity of airports in India. While the Green/Yellow/Red classification system is a starting point for Very Low-Level airspace classification, the draft does not move to enable the essential segregated airspace for drone operations up to an altitude limit of 500ft above ground level.

3. Business Confidentiality

In the domain of Privacy Law, India has taken significant strides to ensure protection of individual and commercial rights over data. The draft (pt 23.) in its current form seems to be out of alignment with this, allowing government and administrations access to potentially private and commercially sensitive information with carte blanche. The models of privacy adopted in other countries in unmanned aviation are often techno-legal in nature. It is recommended that DigitalSky/UTM-SP network data access be technically restricted to certain Stakeholder-Intent mappings: executing searches for Law Enforcement, audit for the DGCA, aviation safety investigations and for Air Traffic Control/ Management. This would need due elaboration in the detailed UTM policy complemented with a legal framework to penalise illegitimate data access.

4. Insurance

One constant hindrance to compliance is the requirement of liability transfer. While the principle of mitigating pilot and operator liability in this fashion is sound, the ground reality is that as of date, very few insurance products are available at reasonable prices. The reason behind it is that insurance companies have not been able to assess the risks of this nascent industry. Assuming the regulation is notified in its current form (pt 28), arguably affording a clean start at scaling up drone operations, we will continue in this vicious dependency loop in the absence of incentives to either end. Again, market forces will drive the development of this industry with customers driving the need for drone operators to obtain insurance for the respective operations. Therefore it is recommended that initially, insurance should not be mandated for any category or type of drone operations, and instead be driven by market or commercial necessity. Over a period of time, insurance may be mandated within the ecosystem.

Similar feedback has been shared by Insurers: “Though the regulator (aviation regulator) has made mandatory the third party insurance, the compensation to be on the lines of the Motor Vehicles Act is somewhat not in line with international practices,” the working group set up by Insurance Regulatory and Development Authority of India (IRDAI) said.”

5. Training

Currently, there’s a requirement of training with an authorized remote pilot training organization (RPTO) (pt 25), applicable for micro-commercial purposes and above (pt 24). While the intent is right, it should not be mandated at the initial stage. The reality is that there are very few RPTO’s that offer training and the cost of such training is often higher than the cost of the drones themselves, while quality is inconsistent. While the current draft rules try to address this problem, they do this with the assumption that liberalizing the requirements for establishing RPTO’s will solve this problem. While this incentivizes more RPTO’s to be established, it still does not incentivize quality and leaves in place the same bureaucratic process for registration. This has been the experience of the ecosystem so far. While it is certainly reasonable to expect that remote pilots should receive training, the goal of better informed and equipped pilotry is better achieved, at this time, if left to manufacturers and market participants to drive it.

There are currently two types of training – Type training and Airspace training. Type training can be driven by manufacturers in the early days, as is the current practice, and Airspace training can be achieved through an online quiz, based on a Concept of Operations. It is our view that customers of drones will have a natural incentive to seek training for their pilots, thereby creating the market need for better quality training schools. Furthermore, as manufacturers establish higher levels of standardization and commoditization, they will partner with training schools directly to ensure consistent quality. In the upcoming years, as the drone ecosystem grows more mature, it will become reasonable to revisit the need for mandating pilot training at approved training schools, and DGCA may create a program that accredits the various RPTOs.

6. Fostering innovation and becoming Atmanirbhar

6A. R&D

To encourage institutional research and development further, we recommend authorised R&D zones be designated, particularly where low population and large areas (like deserts, etc) are available, some key areas of experimentation being long range and logistics operations which might require exemptions from certain compliance requirements.

6B. Import policy

Rather than simply delegating the entire import policy to DGFT (pt 8), there needs to be a clear statement of the import guidelines in the rules based on the following principles in the current draft:

No barriers for the importation of components and intermediary goods for local assembly, value addition and R&D activities

Disincentivising import of finished drone products, both pre-assembled and Completely Knocked Down. Possible avenues could be imposition of special import duty as part of well-considered policy of “infant industry protection”, a policy used successfully in the recent past in South Korea and is considered a part of the policy of Atmanirbhar Bharat by the Principal Economic Advisor to the PM, Sanjeev Sanyal.

Incentivising investments in the indigenous manufacturing industry by aligning public drone procurement with the Defence Acquisition Procedure (2020) and supplemented by targeted government programs such as PLI schemes and local component requirements, which will help realise the PM’s vision of ‘Make in India’ and “Atmanirbhar Bharat’.

In the long term, developing incentives for assemblers to embed themselves into global value chains and start moving up the value chain by transitioning to local manufacturing and higher value addition in India, to be in line with the PM’s vision of Atmanirbhar Bharat. Some suggestions here would be prioritisation for locally manufactured drones for government contracts, shorter registration validity for non-locally manufactured drones etc.

6C. Hobby Fliers

While research and development within the confines of institutions is often encumbered by processes and resource availability, hobby and model flying has enjoyed a long history in manned aviation as a key type of activity where a large amount of innovation happens. Hobby clubs such as The Homebrew Computer Club, of which Steve Jobs and Wozniak were members, and NavLab at Carnegie Mellon University are instances out of which successful industries have taken off. Far from enabling hobby or recreational fliers, they are not even addressed in the draft, which would only limit indigenous technology development. Legally speaking, it would be bad in law to ban hobby flying activities considering hobby fliers enjoy privilege under the grandfathering rights. A solution could lie in recognising hobbyists & establishing hobby flying green zones which may be located particularly where low population and large areas are available. Alternatively, institution-based hobby flying clubs could be authorised with the mandate to regulate the drone use of members while ensuring compliance with national regulations. The responsibility of ensuring safe flying would rest with these registered hobby clubs as is the case in Europe and USA.

7. Encouraging A Just Culture

Implementation is the key to the success of any policy. One of the key factors in encouraging voluntary compliance is an effective means of rewarding the compliant actors while suitably penalising any intentional or harmful violations. Therefore, arguably, an important step could be to build such rewards and punishments. In the context of aviation safety and security, the key lies in effective investigation of any violation while fostering a non-punitive culture. Effective investigations enable suitable corrective actions whilst minimal penal actions encourage voluntary reporting of infringements and potential safety concerns. ICAO encourages a just and non-punitive culture to enhance safety. Penal actions, if considered essential, should be initiated only after due opportunity and should have no criminal penalties except for deliberate acts of violence or acts harming India’s national security. However, considering the fallout from any unintentional accident as well, there should be adequate means for dispute resolution including adjudication.

8. Enabling Increased Safety & Security

The draft while taking a blank slate approach clearly aims to reduce hurdles in getting drones flying. However, we argue that lack of clarity on several issues or not recognising certain ground realities actually reduces the chance of achieving this. We list the details of these issues in the subsections below.

Points 13-14 acknowledge the existence of non-NPNT (No Permission No Takeoff) compliant drones and makes airworthiness the sole criteria for legally flying, provided such drone models are certified by QCI and are imported before the end of this year and registered with DigitalSky. This is a great step forward, however, keeping in mind the win-for-security that NPNT provides through trusted permissioning and logs, it is recommended that NPNT be phased back in with an adoption period of 6 months from the date of notification.

To bring back a semblance of safety to the thought process and keeping in mind that manned aviation would be operating above 500 ft except for takeoff, landing and emergencies, it would be pragmatic to enforce altitude fencing in addition to two-dimensional fencing going forward. Permissive regulation has the effect of encouraging good and bad actors alike, and this measure ensures the correct footing for the looming problem of interaction between manned and unmanned traffic management systems, where risk of mid-air collisions may be brought back within acceptable limits.

9. Institutional Architecture

The draft indicates that institutions such as QCI and Drone Promotion Council (DPC), along with the Central Government, would be authorised to specify various standards and requirements. However, no details have been specified on the means for notification of such standards as in the case of the Director-General (Civil Aviation) having the powers to specify standards in the case of manned aircraft. Such enabling provisions are essential to be factored in the policy so as to minimise constraints in the operationalisation of regulations e.g. as was observed in the initial operationalisation of CAR Section 3 Series X Part I which did not have a suitable enabling provision in the Aircraft Rules.

Further, effective implementation demands that responsibility for implementation be accompanied by the authority to lay down regulations which is sadly missed out in the draft. In the instant draft, the authority to lay down standards rests with QCI/ DPC but the responsibility for implementation rests with DGCA which creates a very likely situation wherein the DGCA may not find adequate motivation or clarity for the implementation of policy/ rules stipulated by QCI/ DPC.

It is not clear that setting up a DPC would advance policy-making and be able to effect the changes needed in the coming years to accelerate unmanned aviation without compromising safety and security. We argue that for effective policy and making a thriving drone ecosystem, Digital Sky is a unique and vital piece of digital infrastructure that needs to be developed and nurtured. In the domain of tech-driven industries, the track record of Special Purpose Vehicles (SPV) is encouraging in India, the NSDL, NPCI and GSTN being shining examples.

The field of unmanned aviation has its own technical barriers to policy making. Its fast-evolving nature makes it extremely difficult for regulators who might not have enough domain knowledge to balance the risks and benefits to a pro-startup economy such as that of India. With the context formed through the course of this paper, it is our view that an SPV with a charter that would encompass development of a concept of operations, future standards, policy, promotion and industry feedback, would be the best step forward. A key example of success to model on would be that of ISRO, which is overseen by the Prime Minister. This would remove inter-ministerial dependencies by overburdening the existing entrenched institutions.

10. Lack of a Concept of Operations

The difference in thought processes behind this draft and the rules notified on 12th March 2021 is significant and is indicative of the large gap between security-first and an efficiency-first mindsets; keeping in mind that mature policymaking would balance the three tenets. It also points to the lack of a common picture of how a drone ecosystem could realistically evolve in terms of technology capability and market capacity while keeping balance with safety and security. The evolving nature of unmanned aviation requires an incremental risk-based roadmap; the varied interests of its many stakeholders makes reaching consensus on key issues a multi-year effort. To this end, taking inspiration from various sources and focusing on the harsh realities peculiar to India, we are in the process of drafting a Concept of Operations for India.

Concluding remarks

With the goal of raising a vibrant Indian drone ecosystem, we recommend the following actionable steps be taken by policy makers:

Immediate Term – Enabling The Ecosystem

Changes to the draft

Airworthiness Compliance requirements for all drone categories be removed till such standards are published

Hobby flying and R&D Green zones be designated in low risk areas

Guiding principles for Import policy formulation be laid out to incentivise import drone parts and de-incentivise drone models

A privacy model be applied to DigitalSky ecosystem data access that technically restricts abuse while laying a foundation for a legal framework for penalties

Insurance be not mandated for any drone categories

The provision for setting up the Drone Promotion Council be subsumed by a SPV as discussed below

Next six months – Setting the ecosystem up for long-term success

A) NPNT be re-notified as a bedrock requirement for security

B) An SPV outside of entrenched institutions be set up with a charter to

1. Envision India’s concept of aviation operations for the next few decades

2. Formulate Future Policy and institutionalize some aspects of key enablers of operations currently missing in India:

Development / update of ConOps

Monitor / develop / customize International standards

Establish Standards for Airworthiness and Flight Training

3. Develop and operationalise DigitalSky in an open, collaborative fashion with oversight and technical governance mechanisms

4. Redefine control zones and segregate airspace for drone operations

5. Establish an advisory committee with equitable membership of stakeholders

6. Address all charter items of the Drone Promotion Council

iSPIRT (Indian Software Product Industry Round Table) is a technology think tank run by passionate volunteers for the Indian Software Product Industry. Our mission is to build a healthy, globally competitive and sustainable product industry in India.

Building on the previous Balloon Volunteering Open House Sessions, we will give a flavour of available volunteering opportunities in the Technology space.

In the fourth Session, we have Dr Pramod Varma, Chief Architect of Aadhaar and IndiaStack, giving you an insight into what it takes to volunteer in iSPIRT. He describes our design principles for building digital public infrastructure and gives you a peek into the thought process of an architect in iSPIRT. Finally, he breaks down how we are redefining the approach towards solving societal problems. We are playground builders. We orchestrate or create a playground so that market players can bring out an array of solutions.

iSPIRT is addressing solvability. We have a multi-decade horizon as a mission-oriented volunteer-based Think-and-Do-Tank.

As part of this session, we have some of our volunteers explaining the technical challenges you can embrace as new volunteers at iSPIRT Foundation. The problems that we are tackling require a thought process that is new and innovative. We use cutting-edge technology.

In addition to the new technical volunteering options outlined in this session, other policy-related and ecosystem-building volunteer options also exist. Apply now on https://volunteers.ispirt.in.

How do you build using Lego Blocks? Watch the recording to learn more.

Following the success of our previous two sessions, we are back again. We are presenting this next session of our open house on the theme of Market Mavens and Market Architecture.

Please find attached the video, which will talk about the available opportunities and what it means to be a volunteer at iSPIRT.

There are many volunteering challenges available. So, if in the past you wanted to volunteer but couldn’t, please do check out the additional challenges listed here. We are adding to the existing challenges that we are working towards. So go ahead and choose any of the options that resonate with you.

This Balloon Volunteering process takes anywhere from 3-4 weeks to start. Also, to get a better idea please do read our Volunteer Handbook and Playground Coda here https://volunteers.ispirt.in/.

iSPIRT Volunteering is about being mission-oriented and being self-motivated, for there is no glory here. So if you have the bandwidth and want to write the new India script, please reach out to us.

A Committee of Experts under the Chairmanship of Shri. Kris Gopalakrishnan has been constituted vide OM No. 24(4)2019- CLES on 13.09.2019 to deliberate on Non-Personal Data Governance Framework. Based on the public feedback/suggestions, the Expert Committee has revised its earlier report and a revised draft report (V2) has been prepared for the second round of public feedback/suggestions. iSPIRT had provided a past response to the previous report and in this blog post contains a response to the revised report.

At the iSPIRT Foundation, our view on data laws stems from the following fundamental beliefs:

Merits of a data democracy (that is, the user must be in charge)

Competitive effects must be well understood, for creation of a level playing field amongst all Indian companies, and some ring-fencing must exist to protect against global data monopolies

Careful design enables both high compliance and high convenience

It is with these perspectives that we have analyzed the revised Non-Personal Data report in our response.

Key Sources of Ambiguity in the NPD Report

The key sources of ambiguity in the report are:

Purpose of techo-legal framework for Non Personal Data: The non personal data framework is meant to provide the right legal and technology foundations for world class artificial intelligence to be created out of India for the betterment of financial, health, and other socio-economically important services. The current version of the report sidesteps this completely by constraining the applicability to only “public good” purposes rather than taking a holistic approach to “business & public good purposes”

Data Business entities need a harmonised definition (given the interplay with data fiduciaries as proposed in the MeitY Personal Data Protection Bill) and clear incentives for participation. The current report relies excessively on regulation & processes for data businesses to achieve the outcome.

Institutional structure for Data Trustees: The report restricts Data Trustees to government agencies and non-profit organisations; however, in a domain consisting of fast evolving technology by excluding the private sector in offering the base infrastructure creates a severe limitation on the ecosystem of modellers that can be created.

Technology Architecture: The illustrated technology architecture is unclear around the public infrastructure (through the form of open standards, public platforms, and others) that need to be created & adopted to bring to life the non-personal data ecosystem in an accelerated manner.

Conclusion

While we’re aligned with the vision of the committee, it’s critical that the above ambiguities are resolved in order to create a strong non-personal data ecosystem created in India. Till these ambiguities are resolved, the recommendations of the Report should not be operationalized.

For any press or further queries, please drop us an email at [email protected]

As we begin 2021, let’s explore some salient points and key considerations for a build vs buy decision in your product journey. If you come from an engineering mindset, the natural inclination is to build things as that is what you take pride in. If you come from a business perspective, the interest is to get a profitable product, often leaning towards a buy to make an impact in the market. As a product manager, let’s take a balanced approach to making the right decision or advising to build or buy.

Penned down some 10 Key considerations that can be useful in making this decision based on my experience of doing some due diligence as well as being part of the decision making process. The focus of this blog is in the context of software products companies, but could be applicable for other products as well.

Faster to market: as pointed in one of my earlier blog, timing to market is a key aspect for products. Let’s consider the current pandemic situation and one of the areas is digital foray including video / online platforms. Many companies have looked at getting to the market faster and may lean towards a buy as it could get them faster by 2-3 years.

Solved vs Unsolved Problem: solved problems are another area for usual buy whereas for unsolved problems you may need more R & D, and therefore a build approach may be more suitable. Solved problems with a good market could be bought over and integrated for better penetration.

Unique IP: connected to the previous consideration, there may be a unique solution IP that solves some unique problems, while it may make sense to invent and build if you find that unique IP, it’s very much possible that you can consider buying out for the IP. We have seen a lot of such things in ML / AI area or in other emerging tech.

Aligned Tech architecture: in software, one of the other consideration when making a buy decision is to understand the tech architecture and if it would be easy to align and integrate the tech into the overall architecture, how much effort is it to integrate, whether the buy would stay standalone, etc. Many times, while the decision may be towards buy to get faster to market if the tech is too different and if there is enormous effort to integrate, it may be more suitable to build it.

Culture fit: the faster to market is ticked, the tech architecture is also ticked, but when you buy it’s not just the product but also the culture that matters a lot. Lot of buy decisions may make sense, but have failed with a misfit in culture of the companies that are buying vs that is being bought. The company that is buying may be a large company and the company that is being bought is a small startup but with some passionate folks, or they may be having a risk-taking vs risk-averse culture.

Price of buy vs cost to build: beautiful, the reasoning is all good, there is tech alignment, and sounds like the culture will be good – but what about the price. What is the viability of investments? This is more of a financial decision, sometimes it could be based on product-market fit, and the timing balanced with price of the buy. What would it take to build this, whether the market is going to grow after a certain period, so building would be better option?

Customers or Users: this is another clear business reason to buy a product. A certain product may be a very successful product, has a huge user base, the buyer company sees a huge synergy of upselling their other products to this customer base or users. This may be useful when you want to expand to a new user base e.g. selling to Sales while you have momentum with Finance.

Talent: we have seen this sometimes, there is a niche product or a popular product, but more than the product, the consideration is the talented engineers or the founder behind the product, their knowledge of the domain, their unique understanding of the problem statement or their reach to the customer network. When you have to build something, it’s going to be hard to build a product team that runs together in unison. Another side of the argument here is if you have a talented team that has a great understanding of the problem statement as well as the technical acumen, it may make more sense to build the product.

Expansion front and back: often product needs more features or needs certain areas for vertical/horizontal expansion on the front or back of existing products. It could be some failed attempt at building that will lead to buy or could be an unsuccessful buy that would lead to build. Sometimes it could be buying an application that showcases an use-case for your product and at other times it could be building a platform that is behind your application to bid adieu a competitor dependency

Data: this is another new area for buy decisions. To expand your platform you need data, for which another product acquisition can help. Leaving aside any legal implication, this has become an important consideration in a buy vs build decision

Making a buy or build decision is a key aspect of software product lifecycle and growth. Hope the above helps a bit

We had our second Open House session on Balloon Volunteering on 14th December over Zoom Conference. Do watch the session video to decide if you would like to explore volunteering with iSPIRT.

Till recently, all our new volunteers (aka Balloon Volunteers) came in through referrals from existing volunteers. Eight weeks back, on 20th Sep, we experimented with an open process in the first Open House session (https://pn.ispirt.in/balloon-volunteering).

We explained the process of Balloon Volunteering and shared a few volunteer challenges. Dozens of people registered. We spoke to each of them and worked with them on the next steps. Three applicants have been accepted as Balloon Volunteers so far. This has given us the confidence to go further in opening up our Balloon Volunteering process.

As you know, iSPIRT is a mission-based non-profit technology think tank. In this second Open House session, we talk about this mission so that you can ask yourself if our cause and theory of change animates you. To understand what volunteers do and how they work, you can read our Volunteer Handbook and Playground Coda. Pointers to these documents are on our new Volunteering page https://volunteers.ispirt.in

If our mission motivates you and volunteering is your passion, see if one of the open volunteering challenges resonates with you. You can then apply using one of the forms on the webpage.

However, keep in mind, volunteering is not for everybody. So, don’t be disheartened if you aren’t able to become a Balloon Volunteer right now. All of us grow with time. Volunteering may be the right thing for you a few years down the line. iSPIRT sticks with hard problems for 20-30 years, so you can be sure that there will be many volunteer opportunities in the future!

The new guidelines on Other Service Provider (OSP) issued by DOT on 5th November is one big step taken by Government of India under leadership of Prime Minister Modi in Ease of Doing business for IT and ITeS sector.

iSPIRT Organised a Panel discussion in PolicyHacks to understand the changes that have been announced and how they impact the Industry.

The panellist included 1. Shri R.S. Sharma, Ex-Chairman TRAI 2. Rahul Matthan, Partner, Trilegal 3. Shanmugam Nagarajan, Founder and Chief People Officer, [24]7.ai 4. Chocko Valliappa, CEO, Vee Technologies 5. Sudhir Singh, Core Volunteer, iSPIRT, Policy Hacks Host

The panel discussion can be watched at below given Youtube video or you can read through the excerpts of the discussion given below in this blog.

Background

IT and ITeS companies looking for seamless cross border communication between the Indian Centers and their foreign counterparts centers use a telecom circuit service (IPLC, MPLS, Sip trunk), obtained from an Indian Telecom Service Provider (TSP). Traditionally, they were supposed to apply and get registered as OSP. The application and approval process were cumbersome and required them to submit detailed network diagrams and satisfy that authority of a legitimate use of the Circuits. The process was cumbersome, more bureaucratic than technical in nature and often subject to undue harassment by TERM cell even when use was fully legitimate.

Industry has been demanding this reform for long, as the Circuits were always subscribed through a licenses TSP in India. The Reform will give way to a new era of opening in telecom services. It is most likely to benefit IT and ITeS industry the most, boost innovation and synergistic alliance in Industry. Most importantly this will make India more attractive for FDI, as this was one major irritant in deploying most important part of the International operations i.e. International Communication.

The move will not only help large offshore IT and BPO Centers but also will empower domestic Software product companies. It will give a huge impetus to work from home and hence will be very instrumental in promotion of SaaS industry, both for their internal operations and also promote SaaS product adoption.

Some of the main highlights of this decision are.

1. No need for a Registration any more to operate as an OSP

2. Interconnection of multiple OSP centers and remote agents

3. Work From Home and Remote locations allowed

4. Centralised Infra and consolidated Traffic between Indian POP and International POP

5. Sharing of EPABX and PSTN lines by domestic and International Center

6. Distributed Architecture with main Infra at central POP and media gateways at other centers

7. CUG allowed for internal Communication

8. CDRs, access log, configurations of EPABX and routing tables to be maintained and aggregated for each media gateway for a period of one year

9. No toll bypass allowed and no telecom services to be provisioned

Excerpts of the Panel Discussions

The panel discussions started with a round of Introduction and inviting Rahul to summarise the new regulations.

Rahul Matthan started the panel discussion with a summary of the guidelines announced. He termed the new guidelines issued as Radically simplified.

Starting the introduction to new Guidelines, he said, “OSP or the Other Service Provider regulation in essence regulates Business Process Outsourcing companies and the definition of the types of entities that are regulated by this is very important. Earlier the definition used to include things like call centers, Business Process Outsourcing and other IT services, but also had very broad language at the end which included all IT enabled Services.

So, the first amendment is that it’s been restricted now to voice based business process outsourcing services.”

“The second very significant amendment that has happened is that the registration requirement has been entirely removed. Earlier you had to register with the TERM cell of DOT and that that requirement has been entirely removed,” Said Rahul.

He further mentioned that work from home (WFH) is allowed without any restriction of site or permissions and submission of network diagrams. He added. “it is work from anywhere” and “also, infrastructure sharing has been permitted there are some significant changes in the interconnectivity regulations have been permitted”.

“Bank guarantees used to run into crores for many large companies. The requirement for submitting performance bank guarantee has now been removed”, mentioned Rahul.