iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

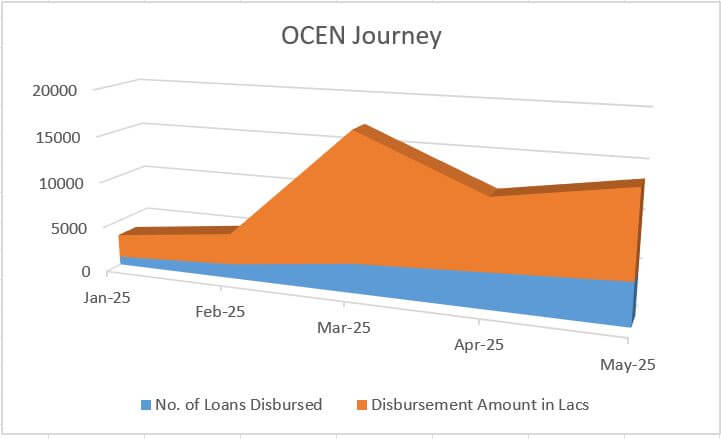

The Open Credit Enablement Network (OCEN) post its initial pilot deployment and continuous upgrades and improvements has seen growing participation across the ecosystem. OCEN’s transition from its early stages into the growth phase is now reflecting in its growing volumes and addition of new ecosystem partners.

Monthly Progress Report:

With the start of the new financial year, the April-June quarter is usually considered a sluggish season in financial services, more particularly in lending business. Corresponding trend reflects in the April performance on the OCEN traction as well, however April & May are still looking progressive in comparison to Jan & Feb performance, considering March financial year end rush as an exception. As newer products and lenders go live on OCEN, the trendline growth looks promising.

Here’s a quick look at the latest numbers on the OCEN ecosystem:

Metric

Jan-25

Feb-25

Mar-25

Apr-25

May-25

No. of Lenders Live on OCEN

7

7

7

8

8

No. of Borrower Agents Live

6

6

6

6

6

No. of Technology Service Providers (TSPs) with active deployment

2

3

3

3

3

No. of Loan Products

11

11

11

12

12

No. of Loans Disbursed

895

1567

3179

3861

4552

Disbursement Amount

₹25.17 Crore

₹33.67 Crore

₹139.11 Crore

₹76.13 Crore

₹90.82 Crore

Average Loan Ticket Size

₹2.81 Lakh

₹2.14 Lakh

₹4.37 Lakh

₹1.97 Lakh

₹1.99 Lakh

OCEN continues to engage with ecosystem partners to build the momentum for new cash flow lending products for MSMEs.

The volumes and traction on Open Credit Enablement Network (OCEN) continues to grow month on month. The growing trajectory highlights OCEN’s ability to streamline and democratise credit access for MSMEs by leveraging digital public infrastructure and fostering collaboration among lenders, agents, and technology providers.

Here is a snapshot of the OCEN ecosystem’s key updates for March:

Metric

Jan-25

Feb-25

Mar-25

No. of Lenders Live on OCEN

7

7

7

No. of Borrower Agents Live

6

6

6

No. of Technology Service Providers (TSPs) with active deployment

2

3

3

No. of Loan Products

11

11

11

No. of Loans Disbursed

895

1567

3179

Disbursement Amount

₹25.17 Crore

₹33.67 Crore

₹139.11 Crore

Average Loan Ticket Size

₹2.81 Lakh

₹2.14 Lakh

₹4.37 Lakh

As OCEN continues to evolve, it is poised to further bridge the credit gap for MSMEs, enabling faster, more transparent, and more inclusive financial support for this vital sector of the Indian economy.

The Open Credit Enablement Network (OCEN) is steadily progressing from its early stages into a more robust growth phase. With its current ecosystem participants, OCEN has started facilitating smoother credit delivery to MSMEs. At the same time, numerous other players are integrating into the protocol and developing specialized loan offerings tailored to the needs of MSMEs.

Here’s a snapshot of the OCEN ecosystem’s key updates for February:

Metric

Jan 2025

Feb 2025

No. of Lenders Live on OCEN

7

7

No. of Borrower Agents Live

6

6

No. of Technology Service Providers (TSPs) with active deployment

2

3

No. of Loan Products

11

11

No. of Loans Disbursed

895

1567

Disbursement Amount

₹25.17 Crore

₹33.67 Crore

Average Loan Ticket Size

₹2.81 Lakh

₹2.14 Lakh

OCEN continues to engage with new participants to further expand the ecosystem, adding new products and scaling up efforts to transform credit access for MSMEs on a large scale.

In the evolving landscape of financial inclusion and digital lending, India has introduced several innovative frameworks designed to streamline access to credit, enhance transparency, and create seamless financial ecosystems. Among these, the Unified Lending Interface (ULI), Open Credit Enablement Network (OCEN), and Account Aggregator (AA) stand out as key initiatives aimed at modernizing the way credit and financial data are managed.

While all three initiatives aim to transform the lending sector, each has distinct roles, benefits, and functions. To better understand their unique features and how they interact with one another, we’ve put together a detailed comparison chart.

This side-by-side breakdown helps you identify the core differences between ULI, OCEN, and AA, their respective use cases, and how they collectively contribute to building a more inclusive and tech-driven financial ecosystem in India. Whether you’re a fintech enthusiast, a policy maker, or simply looking to understand the future of credit access, this comparison will offer valuable insights into these transformative frameworks.

ULI(Unified Lending Interface)

OCEN(Open Credit Enablement Network)

AA(Account Aggregator)

Purpose

Standardized API interface for Lending institutions providing borrower’s financial and non-financial data from various sources, including government databases, and financial institutions. Helps financial institutions to reduce friction for accessing the information needed for quick loan underwriting decisions and efficient loan application processing.

OCEN is a framework of application programming interfaces (APIs) for interaction between lenders, loan agents, collection and disbursement partners, derived data providers, and account aggregators OCEN facilitates flow of credit between borrowers, lenders, and credit distributors using a common set of standards. Various participants in the credit ecosystem can seamlessly connect with one another without needing to build customised APIs and infrastructure. OCEN aims to enable cash-flow based unsecured financing for MSMEs as against balance sheet and collateral based financing. Both ULI and AA can be derived data providers in the OCEN ecosystem.

The Account Aggregator (AA) framework allows users to share consent driven financial data across institutions. Users can access their financial information from multiple institutions in one place, and can decide who can access their data, for how long, and for what purpose. The FI Types are managed by ReBIT.

Users

Regulated entities like Lenders, etc

MSME-focused Borrower Agents and Lenders. Other ecosystem participants include Derived Data Providers, Collection Agents, Disbursement Agents and KYC Partners

Financial Information Users which are Regulated entities and Individuals who wish to access their own financial details

Key Functionality

Enabling RE’s and Marketplaces to fetch different types of financial and non-financial data for underwriting using standard interface.

Standard rails to connect various participants in the Cash flow based MSME lending ecosystem. Enabling building customised credit products for MSMEs and empowering the Borrower agent as a lynchpin and a representative of the borrowers.

Providing safe, user-consented sharing of financial information between regulated financial institutions via the Account Aggregator framework. Individuals can have a holistic single source to view financial data across various institutions.

Data Usage

Utilizes borrower data from diverse sources like banks, land records, and financial history.

Utilizes specific business data of MSMEs like invoices, transactions, etc., for the credit product creation. Any kind of data can be passed to the Lender in the form of derived data. For eg. Government e-Marketplace shares borrower performance data with lenders post consent.

Uses consolidated financial data like bank accounts, GST, income, etc., from FIPs.

Role in Ecosystem

Streamline credit access by integrating borrower data from multiple sources for accurate financial assessment, enabling faster loan approvals through advanced analytics, facilitating easy integration with standardized APIs, and providing lenders seamless access to comprehensive borrower information to simplify credit appraisal and reduce documentation

Fosters innovation in MSME credit by enabling tailored loan offerings and faster credit flow thus enabling access to credit to MSMEs which earlier did not have access to the same. Reduce cost of short tenure, low ticket lending and making it viable to give loans to MSMEs which are end use controlled and enable collection control.

Promotes financial inclusion by simplifying financial data sharing and improving credit decision-making. Allowing user to share their data directly with financial institutions in a consented manner removing the data passing through multiple hands.

Technology Backbone

Consent-based data-sharing infrastructure; APIs to connect various data sources with lenders.

API infrastructure based on standard OCEN protocol for credit enablement. Participant and Product registries to enable discovery and standardisation within the ecosystem.

API-driven, centralized consent architecture defined by ReBIT under the RBI framework.

Regulatory Framework

Proposed under RBI’s initiative to enhance digital lending infrastructure.

Digital Public Infrastructure at a mass roll out stage. Once formalised will be managed and regulated as advised by regulators.

Governing law is the RBI’s Account Aggregator framework under the NBFC-AA license.

Use Cases

A farmer applies for a loan to purchase farm equipment. Lender is able to access land records and other non-financial and financial data through ULI interface to underwrite the loan application.

Zomato as a Borrowers agent on behalf of restaurants enrolled on its platform being able to offer custom loan products specifically built for restaurant partners by the participating lenders based on alternate platform data, ability of providing collection control to lenders via cash flow entrapment and acting as a representative of the borrowers instead of agent of lenders. Like Zomato any of platforms or institutions (like FPO) sitting on a Captive database can utilise OCEN to enable lending on their platform benefiting their users.

Individuals being able to share their multiple bank accounts for specific time periods and for specific purposes with the AA framework using consent mechanism. Businesses being able to share GSTN data to RE’s for loan underwriting purpose using consent mechanism.

Implementation Stage

Proposed platform; Some pilot Implementations for certain data sources have been done. Overall the ULI is in a development phase.

Few pilots – GeM Sahay, GST Sahay, Jan Aushadhi Kendra and Private network have been successfully tested. More implementations are underway at various stages and gaining traction.

Well-established under the RBI’s regulatory framework with multiple FIP’s and FIU’s already integrated.

In this insightful dialogue, Sagar Parikh engages with Deepak Sharma to explore the transformative potential of cash flow lending for Indian MSMEs. Deepak underscores the significance of democratizing credit access through short-tenor and small-ticket loans, especially for micro-enterprises that comprise 99% of the MSME sector in India. Drawing from his rich experience in banking and financial services, Deepak Sharma provides invaluable guidance on navigating the complexities of B2B financing, highlighting the critical role of innovative lending models in fostering inclusive growth.

Deepak Sharma delves into the pressing challenges faced by MSMEs in accessing financing, particularly in the realm of B2B transactions. Leveraging his extensive experience and deep insights, he offers a fresh perspective on the traditional lending landscape, emphasizing the need for agile and tailored solutions to empower MSMEs. By advocating for cash flow-based lending and trust-based scoring systems, Deepak Sharma presents innovative approaches to address credit gaps and unlock opportunities for sustainable economic development within India’s dynamic MSME sector.

Deepak Sharma’s perspectives on banking innovation and financial inclusion provide several key learnings for the industry:

Leveraging Technology for Inclusion: Sharma emphasizes the transformative impact of technologies like UPI and Aadhaar in fostering financial inclusion. These initiatives not only revolutionize digital payments but also open doors to credit access for underserved segments like SMEs.

Proactive Engagement with Tech Ecosystem: Deepak advocates for proactive engagement with India’s tech ecosystem, encouraging early adoption of initiatives like IndiaStack. He challenges banks to rethink their approach and prepare for future changes in the financial landscape.

Importance of Early Adoption: Reflecting on his experiences at Kotak, Sharma stresses the importance of early adoption of innovative initiatives. Banks that jump in early can leverage emerging opportunities and drive meaningful change.

Value of Learning from Ventures: Deepak highlights the significance of learning from both successful ventures like OCEN and past failures. This learning process is essential for banks to navigate the evolving tech landscape effectively.

Structured Innovation with the 5C Model: Sharma’s structured approach to innovation, encapsulated in the 5C model, emphasizes critical aspects such as customer acquisition, commercial viability, credit assessment, compliance, and collections. This framework ensures alignment on objectives and risk management strategies.

Startup Mindset and Controlled Pilots: Adopting a startup mindset within traditional banking institutions, Deepak advocates for establishing small, specialized teams focused on data analysis, technology, and risk management. Controlled pilots with defined success metrics enable banks to manage—- risk effectively and drive innovation.

Importance of Trust-Based Scoring: Sharma underscores the importance of trust-based scoring systems and proprietary scorecards for credit assessment. Moving away from traditional methods, these innovative approaches provide a holistic view of creditworthiness, especially for SMEs with limited credit histories.

Optimism about OCEN: Deepak Sharma’s views on OCEN reflect a visionary approach to addressing India’s credit gap. He sees OCEN as a pivotal platform to harness India’s data richness and enable comprehensive credit assessment and lending solutions.

In conclusion, Deepak Sharma’s insights emphasize the necessity of embracing innovation and leveraging technology to drive inclusive growth in the financial services sector. By adopting proactive strategies, banks can navigate the evolving landscape of digital lending and unlock opportunities for underserved segments, contributing to India’s economic development.

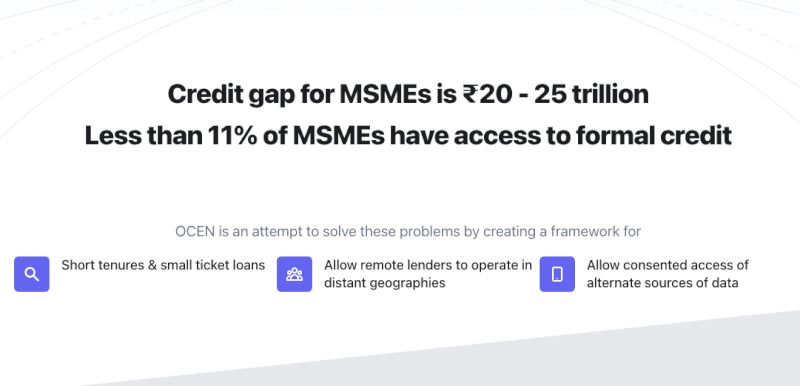

OCEN is an initiative to unbundle lending and enable the creation of specialized entities, each specialized at one part of the job. Therefore, we envision the future of lending to be a partnership between multiple firms individually focused on sourcing/distribution, identity verification, underwriting, capital arrangement, recollections, etc. The entities like marketplaces who have high business-connect with their customers (businesses or individuals), can embed credit offerings in their applications now. These entities are referred to as Loan Agents’ (LAs) and were previously referred to as ‘Loan Service Providers’ (LSPs).

OCEN (Open Credit Enablement Network) aims at democratising the lending ecosystem. The core philosophy is using open networks to reach out to maximum borrowers and lenders, with reduced risk, more transparency, strict control on funds (both end use & collections) and thus building a robust lending ecosystem. At the borrower level, using consent driven architecture and personal data as information collateral, any type of borrower (even new to credit or people with poor credit scores), can access financing. The end-to-end digital processes not only reduces the total cost of operations, but also has the advantage of reaching out to anyone and everywhere, without the lender having a physical presence. For example, sitting out of Jaipur, a NBFC has disbursed OCEN loan on GeM Sahay to borrowers operating from Andaman Nicobar Islands, Manipur, Baramullah etc and the smallest loan transaction has been of Rs.160 for business purposes.

OCEN is the right protocol, to bring credit/finance to the bottom of the pyramid and at the same time lenders also make money with this same section of people at the bottom of the pyramid. OCEN not only levels the playing field between incumbents and challengers, but also reduces the concentration risk which comes with size at bigger players. Most MSMEs are working capital intensive businesses that need quick money and do not have collateral securities to put up to banks for conventional Cash Credit limits like financing. For such businesses, this is a tool to grow their businesses, and improve their credit scores.

Lenders see opportunities in not only sourcing new business, but also reduced risk due to high quality data and use of DPI (Digital Pubic Infrastructure), like GSTN, Account Aggregator, Digilocker and its associated APIs, like mobility, Health, Fastag etc.

Why OCEN

Low Cost of Acquisition >> The Borrower Agent brings his borrowers on the network, reducing the cost of acquisition through various channels. OCEN framework benefits the Lenders to gain easy access to borrowers. Not just borrowers of one network, but easy access to multiple sets of borrowers of multiple networks.

Lower Cost of Underwriting >> The Borrower Agent also acts as a Provider of Derived Data along with other Underwriting data from various sources like GSTN and Account Aggregator which helps in lowering the Cost of Underwriting

Digitisation >> OCEN Digitises the whole process which involves various activities like Bureau pull, KYC validation, Account Aggregator data, E-Sign on documentation, e-NACH for repayment etc and reduces the time and effort of processing at reduced costs.

Reduced Cost of Collections >> OCEN provides a large opportunity to Lenders and Borrowers to participate in T4 (Type 4) loan products which have End Use Control and Collections control for ensuring higher portfolio quality and cash flow control as well as reduced Cost of collections

OCEN solves for MSME’s Credit requirements: Small Ticket Short Tenure Loan

Small businesses need loans of smaller amounts and for shorter tenures (15/30/90 days) for their businesses compared to larger businesses to help them navigate through the requirement of day-to-day Working Capital needs.

It also helps Lenders to create Loan books for smaller loans which are granular loan exposure on a rotational basis, compared to large bulky loans. Hence reducing concentration risk.

As these Loans are for short tenure, there is higher predictability and lower risk compared to long tenure loans in which recovery of loans may sometimes be a challenge.

The Loan Agent (LA) model is a departure from the Direct Sourcing Agent (DSA) model and is an ‘agent of the borrower’. The LA explains to borrowers their ‘bill of rights’ ensuring transparency and safeguarding of borrower interests. They educate the borrowers about the various credit product offerings, pricing and more details. They help the borrowers get access to formal, affordable credit at low interest rates and collaborates with lenders to create more tailored offerings for borrowers.

In their simplest form, LAs are a loan marketplace that enables borrowers to compare loan offers from multiple lenders and choose the best one. In a more advanced version, the LAs are akin to a borrower’s financial advisor, looking after their interests, fetching the best offers and advising the customer to make good decisions.

In the longer run, it is envisioned that many more LAs (with apps) will be created. Each of them would focus on distinct borrower pools and build the specialized experiences suited to their customers. This would allow lenders to focus purely on their underwriting and collections logic and cater to diverse collaborations with the LAs.

OCEN 4.0

The OCEN model has been built incrementally in phases, with reinforced learnings from each of the previous pilots. The goal for OCEN 4.0 is to build an ecosystem of participants that creates a Cambrian explosion of cash-flow based loan products across different MSME sectors and different types of borrowers.

Participant Roles

OCEN 4.0 supports specialized roles for the participants. The purpose of introducing new roles is that it promotes specialization and enhances system efficiency. For example, by establishing a local network of participants, the burden on lenders is reduced, resulting in increased credit accessibility in underprivileged areas.

Role

Description

Lender

Lenders are the regulated entity that create and own the credit products. They work with other participants as part of a Product Network to serve the Borrower. The Loan-agent understands the borrowers’ credit requirements and works with the lenders to create the product.

Loan-Agent (LA)

Agent of the borrower who will help the Borrower to pick up the best loan offer. The Borrowers agent will charge the Borrower a fee for helping them select the best loan. Loan agent is a more inclusive term that encompasses both Borrower Agent (BA) and Lender Service Provider (LSP), spanning across the existing DLG model referred to as LSP and the emerging model in which BA operates as the borrower agent.

Derived Data Partner (DDP)

A derived data provider is a collaborating partner within the network that furnishes supplementary data to the Lender, aiding in enhancing their underwriting engine with additional information.

Collections Partner (CP)

A Collections Partner is a network-affiliated collaborator designated by the Loan Agent (LA) to aid in the collection process. The lender retains the option to either opt for the Collections Partner or continue using their existing collection procedures.

Disbursement Partner (DP)

A Disbursement Partner (DP) is responsible for supporting Purpose Controlled products. This partner will establish integration with suppliers, retrieve their catalog, and facilitate seamless direct payments to suppliers within the OCEN journey.

KYC Partner

A KYC partner is a collaborator selected by the Loan Agent (LA). This partner can be engaged for Assisted KYC or any technology-related specialization available on the network. The lender retains the choice to employ the KYC partner within the network or continue with their existing procedures.

In addition to the participant roles above, OCEN framework also relies on Account Aggregator and Credit Guarantees (CGTMSE) as part of the loan journey.

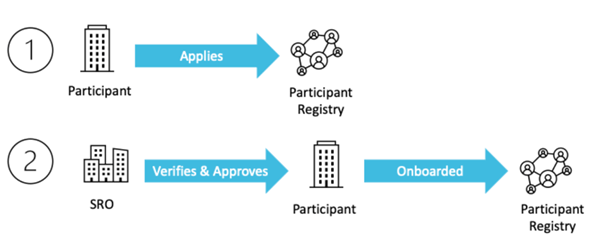

Participant Onboarding

All participants are onboarded to OCEN 4.0 via the participant registry. A standard onboarding process is followed for all participants, and their verification is guaranteed by SROs to ensure that new members receive an equivalent level of trust within the network.

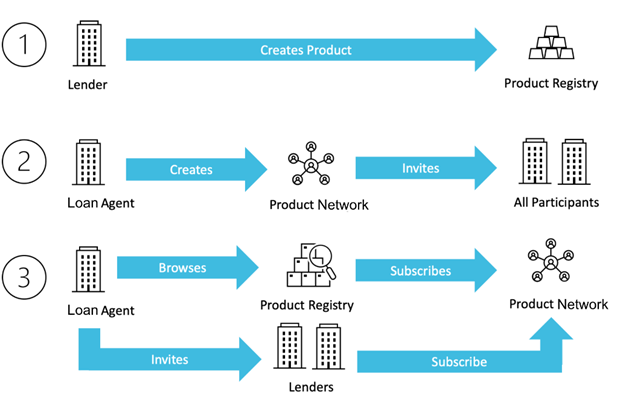

Product and Product Network onboarding

Lender will create & manage the Product and the Loan Agent will create & manage the Product Network to serve that product. All participants in OCEN 4.0 can browse the Products and Product Networks on the Product Registry and subscribe to serve a Product via the Product Networks.

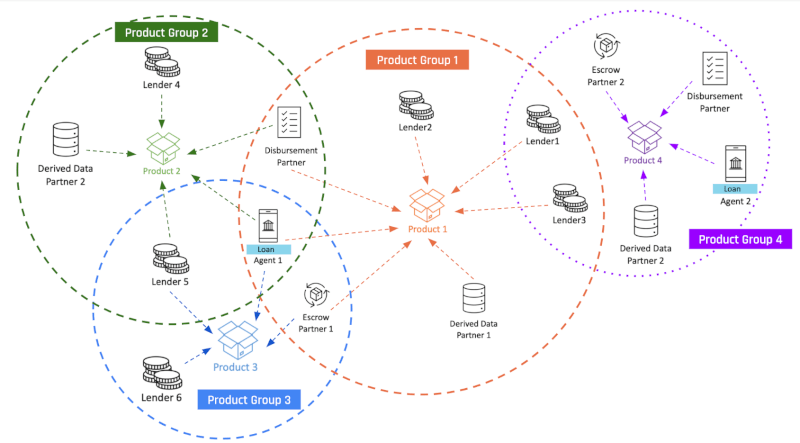

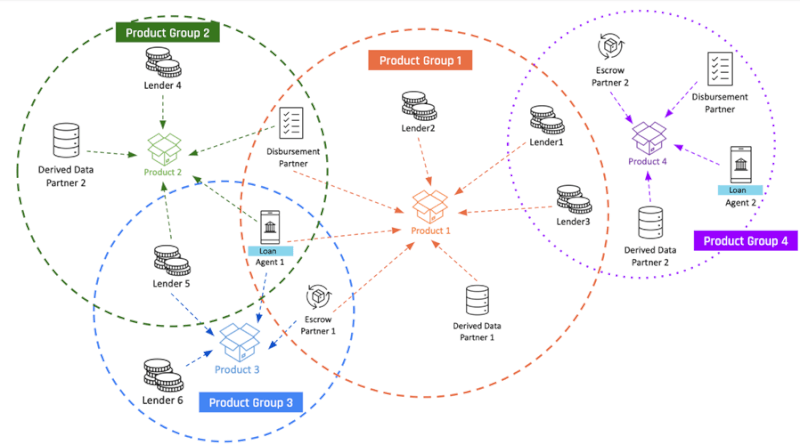

Product Networks

OCEN 4.0 enables a network of product networks that participants can discover, collaborate and serve products to borrowers. See sample example below:

Network begins with Product Network 1

Created by Loan Agent 1 who onboards as network participants – 3 lenders, disbursement partner, collections partner and a derived data partner

Loan agent 1 can serve their borrowers other products as well.

Network expands with Product Network 2

Created by Loan Agent 1 who onboards as network participants – 2 new lenders, the same disbursement partner, and a new derived data partner

Loan agent 1 can continue to serve their borrowers other products as well.

Network expands with Product Network 3

Created by Loan Agent 1 who onboards existing participants and a new lender (Lender 6) to serve the product

Participants can discover products and join the product network

Network expands with Product Network 4

Created by a new LA, Loan Agent 2, who onboards existing and new participants to serve the product to their borrowers

GeM is a short form of one stop, ‘Government e-Marketplace’ where common user goods and services can be procured by various Ministries and agencies of the Government. Government e Marketplace (GeM) offers both products and services as part of its offerings to its registered buyers. GeM facilitates the procurement of a spectrum of Product and Service categories in a way to facilitate Buyer in ease of selection and procurement. GeM SAHAY is an online platform built on the OCEN protocol that provides loans against Purchase Orders to the sellers.

GeM SAHAY is the pilot project on OCEN to validate the idea of cash-flow based lending for MSMEs. In this pilot, GeM (Government e-Marketplace) is the Loan Agent. The Lenders onboarded onto the pilot offer loans to MSMEs on the GeM portal against government purchase orders. The pilot validates that short-tenure, small-ticket size loans enabled via the OCEN network works for all participating parties.

GeM as a Loan Agent allows the Goods and Service Providers on GeM to apply for Loans against Purchase orders received through various Government buyers on the GeM portal.

GeM as a Loan agent helps onboard borrowers for lenders reducing the acquisition cost for the lenders

GeM being a loan agent also acts as a Derived Data Provider as it carries rich data of the participating MSME borrowers in terms of past number of orders, value of orders executed, quality incidences, completion timelines, etc and these data points help the participating Lenders to underwrite the MSME loan application.

GeM facilitates digital loan process for MSMEs on its GeM SAHAY portal by ensuring integration with multiple lending institutions and helps the Borrower MSMEs to receive multiple offers for its loan applications. Allowing the MSME to choose the best suitable loan offer creates a market shift from Lender’s market to Borrower’s market.

GeM also acts as a Collection partner for the Lending institutions as it helps the lender with repayment of the loan for the purchase order though the Escrow account where the payment for the orders executed is credited by the purchasing entities.

A second pilot that expanded on the above is the GST SAHAY pilot project. This pilot uses GST data to enable working capital loans where SIDBI is acting as the Loan Agent. An additional parameter for validation on this pilot was the inclusion of the Account Aggregator data for loan underwriting.

In GST SAHAY, borrowers can seek loans against unpaid B2B Invoices for supply of Goods and Services to other businesses. Any business registered with GSTN and filing the statutory returns on GSTN can seek financing against Invoices where goods or services are supplied on credit period.

Borrower can register on GST SAHAY application and upload Invoices against which it seeks to avail financing.

The GST SAHAY application, after seeking the consent of borrower will pull details available from the GST network for its past invoice transactions filed with GSTN, periodic return filings and share the same with Lenders for evaluation and underwriting and credit decisioning.

Similarly, GST SAHAY application after seeking the consent of the borrower will pull details of the Bank statements available from Account Aggregator framework for its past banking data and share the same with Lenders for evaluation and underwriting and credit decisioning.

Lenders will parallelly also check the Credit Bureau of the borrower to assess credit worthiness and past performance on existing credit facilities from other lenders, if available.

Lending institutions will digitally consume all these data points, along with details available on the Invoice to be financed and by using its proprietary rule engine for underwriting and scoring model, will provide an offer to the borrower for the respective Invoice to be financed.

Borrowers may receive multiple offers (higher loan amount, lesser interest rate, longer tenure) from different Lenders based on their evaluation criteria and will have a choice to select the best suitable offer for seeking the disbursement in a digital way by e-signing the loan agreements, e-Nach / Standing instructions, wherein the amount will be credited to the borrower’s account within few minutes.

There are other OCEN innovative product networks which are at various stages of development and are expected to go live to provide seamless credit to the credit starved MSMEs using OCEN API specifications for communication between the parties (Borrowers, Lenders, Loan Agents and other participants)

In this recent OpenHouse, Sagar Parikh discusses with Dr Ravi Modani how democratizing credit through short-tenor and small-ticket loans can help finance Indian MSMEs, 99% of which are micro-enterprises. Dr Modani shares his insights and invaluable guidance to navigate the complex world of B2B financing for MSMEs.

He also delves deep into the challenges faced by them in accessing financing, particularly in the realm of B2B transactions. Drawing from his extensive experience and research, he offers a fresh perspective on the traditional lending landscape and presents innovative solutions to empower MSMEs.

Key Insights from the Video:

The MSME Financing Dilemma: Dr. Modani highlights the significant hurdles that MSMEs encounter when seeking short-tenor and small-ticket loans. He emphasizes the need for a paradigm shift in lending practices to better serve the unique needs of these businesses.

A New Way Of Financing for MSMEs: Dr. Modani advocates for a pioneering financing approach for MSMEs, highlighting the effectiveness of short-tenor and small-ticket loans. These loans, being revolving in nature throughout the year, allow lenders to disburse a higher volume of loans. Consequently, lenders can potentially amplify their AUM by up to 8 times, surpassing the typical 5-6 times AUM ratio associated with traditional lending practices.

Comparing Financial Platforms: Dr. Modani provides a comprehensive comparison between TReDs and OCEN, offering insights into the advantages of leveraging public networks like OCEN for enhanced interoperability and accessibility.

The Power of Public Networks: Leveraging platforms like OCEN and GeM can significantly reduce operational costs for lenders, ultimately leading to lower lending costs and improved efficiency. Dr. Modani illustrates how these public networks can drive down the cost of lending, benefiting both lenders and borrowers alike.

The Time Sensitivity of MSME Financing: Dr. Modani underscores the time-critical nature of MSME lending and stresses the importance of streamlining the loan journey to ensure timely access to funds for businesses.

His illustrations and learnings help in navigating the complex world of MSME financing by embracing innovative approaches. He believes that leveraging public networks like OCEN will only help lenders unlock new growth and success in today’s lending landscape by opening multifold opportunities to them.

In our most recent OpenHouse, we embark on an insightful exploration of the transformative landscape in MSME lending, featuring Bhavik Vasa, the Founder of GetVantage, and Sagar Parikh. The conversation delves into the potential of creating groundbreaking impact through interoperable networks, particularly focusing on OCEN. The discussion navigates the dynamic intersection of finance and technology, highlighting how inventive solutions are reshaping the lending panorama. Emphasizing the crucial role of interoperability, the dialogue underscores its significance in bridging the credit gap, propelling the MSME sector into a new era of unprecedented growth.

Key Takeaways:

Network Effects Unleashed: OCEN catalyzes network effects, narrowing the credit gap and expanding the market, fostering inclusivity and vibrancy.

Efficiency through Interoperability: Standardized protocols cut costs and efforts, providing high-quality data for lenders while empowering MSMEs with smoother access to loans.

Addressing Unmet Needs: Explore how interoperable networks bridge gaps in unsecured lending, catering to shorter tenures and smaller loan sizes.

Tech-Enabled Business Growth: Witness the role of unsecured lending in a tech-driven landscape, fostering a circular consumption economy for economic growth.

Personalized FinTech Solutions: Bhavik advocates for a borrower-centric approach, urging lenders to view lending through a tech and data-driven lens, benefiting both parties.

Collaboration Dynamics: Conclude with insights on how NBFCs and banks can coexist and collaborate, playing to their strengths for a more robust lending environment.

Ready to unlock the future of MSME lending? Join the conversation now!

Intermediaries and Fintechs have played an important role in the lending ecosystem, but the impact is mostly seen in consumer lending and not so much in MSME lending, especially for unsecured, small ticket and short duration loans. What are the missing pieces in the lending process for which advanced tech and a mindset shift can utilise a digital infrastructure like OCEN (Open Credit Enablement Network) and unlock this credit supply for MSMEs?

Recently, we hosted Lizzie Chapman in an insightful conversation with Sagar Parikh. She shared her views on where the intermediaries and FinTechs can further become a value add in a profitable manner by pushing the boundaries of technology.

Points discussed:

Digital infrastructure & its impact on the costs, penetration & process for lending eco-system

Unsecured MSME loans not as solved as unsecured consumer loans. Cashflow lending addresses the concerns around unsecured lending to MSMEs.

DPI such as OCEN facilitating the availability, quality, aggregation of data for credit underwriting along with loan disbursement for MSMEs

Need for Intermediaries & Fintechs to harness technology to conceptualise innovative lending products, advanced ways of pricing and matching risks & address the opex challenges in collections & repayments

Investors tend to prefer businesses that touch the customer end to end. They should see that being part of the value chain can be as profitable as owning the value chain.

OCEN is creating dispute resolution mechanisms but intermediaries should also innovate for transparency and building trust with the customers so as to enable a safe, stable, secure growth in short term cashflow lending for MSME credit.

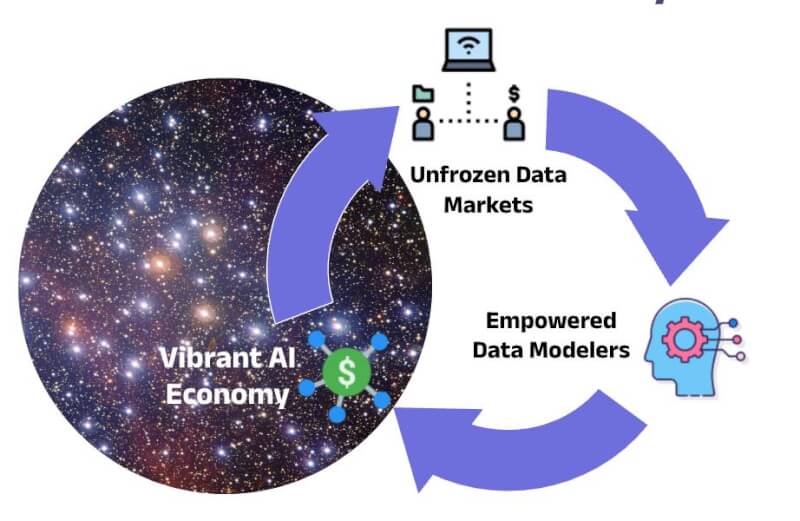

This is the 4th blog in a series of blogs describing and signifying the importance of DPI for AI, a privacy-preserving techno-legal framework for AI data collaboration. Readers are encouraged to first go over the earlier blogs for better understanding and continuity.

We are at the cusp of history with regard to how AI advancements are unfolding and the potential to build a man-machine society of the future economically, socially, and politically. There is a great opportunity to understand and deliver on potentially breakthrough business and societal use cases while developing and advancing foundational capabilities that can adapt to new ideas and challenges in the future. The major startups in Silicon Valley and big techs are focused first on bringing the advancements of AI to first-world problems – optimized and trained for their contexts. However, we know that first world’s solutions may not work in diverse and unstructured contexts in the rest of the world – may not even for all sections of the developed world.

Let’s address the elephant in the room – what are the critical ingredients that an AI ecosystem needs to succeed – Data, enabling regulatory framework, talent, computing, capital, and a large market. In this open house

we make a case that India is the place that excels in all these dimensions, making it literally a no-brainer whether you are an investor, a researcher, an AI startup, or a product company to come and do it in India for your own success.

India has one of the most vibrant, diverse, and eager markets in the world, making it a treasure chest of diverse data at scale, which is vital for AI models. While much of this data happens to be proprietary, the DPI for AI data collaboration framework makes it available in an easy and privacy-preserving way to innovators in India. Literally, no other country has such a scale and game plan for training data. One may ask that diversity and scale are indeed India’s strengths but where is the data? Isn’t most of our data with the US-based platforms? In this context, there are three types of Data:

a. Public Data, b. Non-Personal Data (NPD), and c. Proprietary Datasets.

Let’s look at health. India has far more proprietary datasets than the US. It is just frozen in the current setup. Unfreezing this will give us a play in AI. This is exactly what DPI for AI is doing – in a privacy-preserving manner. In the US, health data platforms like those of Apple and Google are entering into agreements with big hospital chains – to supplement their user health data that comes from wearables. How do we better that? This is the US Big Tech-oriented approach – not exactly an ecosystem approach. Democratic unfreezing of health data with hospitals is the key today. DPI for AI would do that even for all – small or big, developers or researchers! We have continental-scale data with more diversity than any other nation. We need a unique way to unlock them to enable the entire ecosystem, not just big corporations. If we can do that, and we think we can via DPI for AI, we will have AI winners from India.

Combine this with India’s forward looking regulatory thought process that balances Regulation for AI and Regulation of AI in a unique way that encourages innovation without compromising on individual privacy and other potential harms of the technology. The diversity and scale of the Indian market act like a forcing function for innovators to think of robustness, safety, and efficiency from the very start which is critical for the innovations in AI to actually result in financial and societal benefits at scale. There are more engineers and scientists of Indian origin who are both creating AI models or developing innovative applications around AI models. Given our demographic dividend, this is one of our strengths for decades to come. Capital and Compute are clearly not our strong points, but capital literally follows the opportunity. Given India’s position of strength on data, regulation, market, and talent, capital is finding its way to India!

So, what are you all waiting for? India welcomes you with continental scale data with a lightweight but safe regulatory regime and talent like no place else to come build, invest, and innovate in India. India has done it in the past in various sectors, and it is strongly positioned to do it again in AI. Let’s do this together. We are just getting started, and, as always, are very eager for your feedback, suggestions, and participation in this journey!

This is the third in a series of blogs describing the structure and importance of Digital Public Infrastructure for Artificial Intelligence (DPI for AI), a privacy-preserving techno-legal framework for data and AI model building collaborations. Readers are encouraged to go over the first and second blogs for better understanding and continuity.

The techno-legal framework of DEPA, elaborated upon in the earlier blogs, provides the foundations. From multiple discussions and history, it is clear that building and growing a vibrant AI economy that can create a product nation in India, requires a regulatory framework. This regulatory structure will serve as the legal partner to the technology aspect and work hand in hand with it. Upon this reliable techno-legal foundation will the ecosystem and global product companies from India be materialized.

‘Data Empowerment And Protection Architecture’ – or DEPA’s – worldview of ‘regulation for AI’, rather than the more conventional ‘Regulation of AI’ espoused by US, EU and so on sets DEPA apart and drives India towards an AI product nation with a global footprint.

How does one envisage the form and function of ‘Regulation for AI’? In this open house, we have a dialog between technology and legal sides of the approach to explain the significant facets.

In a nutshell, ‘Regulation for AI’ will focus on

what standards the AI models need to adhere to

define a lightweight but foolproof path for getting there for startups as well as the big players

provide an environment which deals with many of the compliance and safety aspects ab initio

define ways to remove hurdles from the innovator’s paths

In contrast, ‘Regulation of AI’ deals with what AI models cannot be and do and the tests and conditions that they have to pass depending on the risk classes that they are placed into. This is akin to certification processes in many fields such as pharma, transportation and so on which impose heavy cost burdens, especially on new innovators. For instance, many pharma companies which develop potentially good drug candidates run out of steam trying to meet the clinical trial conditions. Very often they are unable to find a valid and sizeable sample population to test their products as a part of the mandatory certification process.

The current standards in the new Regulation of AI in the US, EU and so on leave many aspects such as the risk model classification process undefined, leading to regulatory uncertainty. This also works against investment driven innovation and consequent growth of the ecosystem in multiple ways.

The path to value both for the economy and the users, lies in the power of the data being projected into the universe of applications. These applications will be powered by the AI models in addition to other algorithmic engines. The earlier blogs already addressed the need and the way for data to make their way into models.

For the models to exhibit their power, we must make sure they are reliable and used widely. This requires the AI models be accessible and available and most importantly, ‘do no harm’ when they are applied, through mistakes, misuse or malfeasance. In addition to this, humans or their agents must not be allowed to harm the markets and users through monopoly control of the AI models. Large scale monopolistic control of these models which have global use and relevance can lead to situations which are beyond national or international legislation to control or curb.

In the DEPA model, this benign, and in most ways, benevolent environment is created by a concinnous combination of technology and legal principles. Having analyzed the technological aspects of data privacy in the earlier blogs in this chain, here we will talk about the regulations implemented via a Self-Regulatory Organization – the SRO.

Though not fully fleshed out, the SRO provides functions such as registration and roles to participants such as TDP (Training Data Provider), TDC (Training Data Consumer) and CCRP (Confidential Clean Room Provider). Many of these functions have been implemented in part to support the tech stack that we have released with respect to the CCR (Ref: DEPA Open House #1). This tech stack currently supports registration and allows the interactions between participants to be mediated via electronic contracts (the technological counterpart of legal contracts).

The technology that validates the models through pre-deployment analysis based on complex adaptive system models is under development and is based on diverse research efforts across the world. This technology is designed for measuring the positive and negative impact of use of these models on societies at small and large scale and in short and long timescales.

‘Complex adaptive system models’ are dynamic models which can capture agents with their state information and the multiple feedback loops which determine the changes in the system at different scales, sometimes simultaneously. The large number of components and the many kinds of feedback loops with their dynamic nature are what make these models complex and adaptive. These models, while still in their infancy in many ways, are critical to the question of understanding the AI models’ impact on societies.

The SRO guides and supports the ecosystem players in building and deploying their models in a safe and secure way with lightweight regulatory ceilings so that large product companies in many fields like finance, healthcare, and education can grow and reach a happy consumer base. This is key to growing the ecosystem and connecting it to other parts of the India stack.

We envisage leveraging the current legal system in terms of the different Acts (DPDP, IT Act, Copyright etc.) and models of Data Protection through CDO ( Chief Data Office) and CGO ( Grievance Office) in companies in India in defining the SRO’s role and features further.

The regulatory model also looks at the question of data ownership and copyright issues, especially in the context of Generative AI. We require large foundation models independent of the ‘Big Tech’ to fight potential monopolies. These models should be reflective of the local diversity to serve as reliable engines in the context of India. We need these models built and deployed locally, to be able to play a role as a product nation without being subverted or subjugated in our cyberspace strategies.

To light up the AI sky with these many ‘fireflies’ in different parts of India, infrastructure for compute as well as market access is needed. The SRO creates policies that are not restrictive or protective but promotes participation and value realization. The data players, compute providers, market creators and users need to be able to play with each other in a safe space. Sufficient protection of copyright and creative invention will be provided via existing IP law to incentivize participation while not restricting to the point of killing innovation – this is the balance that the regulatory framework of SRO strives to reach.

Drawing upon ideas of risk-based categorization of models (such as in the EU AI Act) and regulatory models (including punitive and compensatory measures) proportional to them, the models in India Stack will be easily compatible with international standards, as well as a universal or global standard, should an organization such as a UN agency define it. This makes global market reach of AI models and products built in India, an easier target to achieve.

We conjecture that these different aspects of DEPA will release the data from its silos. AI models will proliferate with multiple players profiting from infrastructure, model building, and exporting them to the world. Many applications will be built which will be used both in India (as part of the India Stack) and the world. It is through these models and applications that the latent potential and knowledge in the vast stores of data in India will be realized.

In an era of evolving financial landscapes, the realm of lending is witnessing a significant shift—from the traditional collateral-based approach to the more contemporary cash flow lending model facilitated by OCEN (Open Credit Enablement Network). Recently, we hosted UGro Capital in an insightful conversation with Shachindra Nath, shedding light on this transformative paradigm in lending and delving into its profound implications.

Points discussed:

Transitioning from Collateral to Cash Flow Lending

OCEN plays a pivotal role in revolutionising MSME lending in India. This innovative open network is specifically designed to serve those new to credit, employing an omni-channel approach that democratises and simplifies access to lending.

Currently, the market lacks a scalable and profitable model for short-term, low-value MSME loans – a significant gap that OCEN has adeptly filled with itsGeM-SAHAY pilots.

Amidst the confusion and excitement surrounding OCEN versus ONDC, and the broader impact of open networks in the lending sphere, this blog aims to provide clarity and insight. Let’s dive in and explore these transformative developments.

🔀 OCEN or ONDC: Which is better for short tenure MSME lending?

There’s much debate about which lending framework potential partners should explore. Rahul Mathur (Associate Director, InsuranceDekho) captures this perfectly in his tweet, presented as a checklist below:

🗣️ “Turns out, the focus in lending for ONDC v/s OCEN is very different (see the

image below)

(1) 💰Type of loan: Type 1 personal loan v/s Type 4 MSME loan

(2) 🔎GTM: Online v/s Omni-channel (assisted)

(3) 🙇Persona: Eligible for credit v/s New to credit

(4) 🌟Objective: Bring credit to point of commerce v/s Democratize credit access

To summarize, there are some good reasons why ONDC has launched loans

independently of the OCEN network.

Over time, OCEN will expand to include further lending use-cases & products.

And, at that point, ONDC <> OCEN interoperability would make sense.”

Clearly, OCEN is the undisputed option for short tenure, low ticket size lending for new to credit MSMEs. Over time the lending use cases will be expanded to service the traditional form of loans.

OCEN and ONDC, while both operating in the lending space, are tailored for very different use cases and audiences. While they may overlap in some cases, the larger ecosystem benefits from introduction of newer networks. In the end, it’s all about solving the most challenging problems 🙂

Let’s further understand how OCEN addresses the MSME lending problem in India.

📈 OCEN makes small ticket size lending a reality

OCEN’s primary goal is to make short-term lending profitable. Something which we’ve achieved in our pilots with the Government e-Marketplace, through the GeM-SAHAY app.

One of our volunteers explains the economics in this blog post:Evaluating the short term lending opportunity, where he shows how lenders can earn 2.2x higher revenue with the same capital through the adoption of the OCEN framework.

The significant 2.2x increase in revenue is attributed to the introduction of a crucial role known as the borrower’s agent. These agents not only reduce the cost of servicing a loan but also heighten accountability within the system.

Borrower’s Agents (BAs) assume a variety of roles traditionally outsourced by lenders, BAs function as data providers, collections agents, escrow account managers, and product providers.

By integrating these services and cohesively binding the network, BAs enable lenders to efficiently service low-cost loans even in remote areas. In performing these four key roles, the borrower’s agent emerges as the cornerstone of the open network, vital for its effective operation.

The role of borrower’s agent has been discussed in depth in one of our open house sessions:

OCEN is changing the game by making even the tiniest loans worthwhile for both the lender and the borrower.

🌐 Efficacy of Open networks and streamlining the lending process

Some people we’ve spoken to, worry that open networks will lead to the commodification of lending, which, in turn, is bad for the overall market. However, this couldn’t be farther from the truth 🙂.

OCEN streamlines the lending process by introducing roles such as the borrower’s agent, KYC agents, and collection partners. These roles combine to create a bundle that lenders can easily integrate into their processes to start lending.

Newer and smaller lenders will benefit from the transparency and scale offered by open networks.

Closed network auctions, which are common today, see lenders bidding down for loans. However, their lack of transparency and scale often results in low profitability.

Open networks, on the other hand, provide scale and transparency that leads to low cost of servicing, more borrowers to choose from, and reliability in the system through a borrower’s agent.

Larger lenders benefit from the low cost of servicing a loan that comes with open networks

Larger lenders will benefit from open networks as it provides the technical chops of a borrower’s agent. BAs can help with KYC, collections and other parts of servicing a loan while absorbing some of the costs.

We’ve seen such effects before, with the introduction of Aadhaar and UPI, where KYC and collections became far cheaper enabling large lenders to facilitate smaller ticket size loans.

In conclusion

Through OCEN, the potential to unlock a ~$300 billion credit market in India becomes a tangible reality. This is demonstrated by the increased revenue potential and the introduction of the borrower’s agent role, enhancing loan servicing efficiency and accountability.

Moreover, OCEN’s streamlined lending process benefits the entire market, by offering scalability and cost-effectiveness to both emerging and established lenders.

Thus, embracing OCEN is not just a choice but a strategic direction for expanding market possibilities and empowering both lenders and borrowers in the dynamic credit landscape of India.

This is the 2nd blog in a series of blogs describing and signifying the importance of DPI for AI, a privacy-preserving techno-legal framework for AI data collaboration. Readers are encouraged to first go over the 1st blog for better understanding and continuity.

What is unique about the techno-legal framework in DPI for AI is that it allows for data collaboration without compromising on data privacy. Now let’s put this in perspective of Indian enterprises and users. This framework can potentially revolutionize the entire ecosystem to slingshot India towards an AI product nation where we are not just using AI models developed within India but exporting the same. What is the biggest roadblock in this dream? In this open house (https://bit.ly/DEPA-2), we make a case that privileged access to data from Indian contexts is not only necessary to develop AI-based systems that are much more relatable to Indians but in fact, gives Indian innovators a distinct advantage over much larger and better funded big tech companies from the west.

Let’s get started. Clearly, there is a race to build larger and larger AI models these days trained on as much training data as possible. Most training data used in the models is publicly available on the web. Given that Indian enterprises are quite behind in this race, it is unlikely that we will catch up by simply following their footsteps. But what many folks outside of AI research circles often miss is that there has been credible research that shows that access to even relatively small amounts of contextual data can drastically reduce the data and compute requirements to achieve the same level of performance.

This sounds great, right, but (there is always a but!) much of this Indian context data is not in one place and is hidden behind numerous government and corporate walls. What makes the situation worse is most of these data silos are enterprises of traditional nature and are not the typical centers of innovation, at least for modern technologies like AI. This is a fertile ground for DPI for AI. The three core concepts of DPI for AI ensure that this data sitting in silos can be seamlessly (thanks to digital contracts) and democratically shared with innovators around India in a privacy-preserving manner (thanks to differential privacy). The innovators also do not need to worry one bit about the confidentiality of their IP (thanks to confidential computing). The techno-legal framework makes it super easy for anyone to abide by the privacy regulations without sweat. This will keep them safe from future litigations as long as they follow easy-to-follow guidelines provided in the framework. This is what we refer to as the unfreezing of data markets in this Open House. This unfreezing is critical for our innovators to get easy access to contextual data to give them a much-needed leg up against the Western onslaught in the field of AI. This is India’s moment to leapfrog in the field of AI as we have done in so many domains (payments, identity, internet, etc.). Given the enormity of the goal and the need to get it right, we seek participation from folks from varied expertise and backgrounds. Please share your feedback here

In the last decade, we’ve seen an extraordinary explosion in the volume of data that we, as a species, generate. The possibilities that this data-driven era unlocks are mind-boggling. Large language models, trained on vast datasets, are already capable of performing a wide array of tasks, from text completion to image generation and understanding. The potential applications of AI, especially for societal problems, are limitless. However, lurking in the shadows are significant concerns such as security and privacy, abuse and mis-information, fairness and bias.

These concerns have led to stringent data protection laws worldwide, such as the European Union’s General Data Protection Regulation (GDPR) and California’s Consumer Privacy Act (CCPA), and the European AI Act. India has recently joined this global privacy protection movement with the Data Protection and Privacy Act of 2023 (DPDP Act). These laws emphasize the importance of individuals’ right to privacy and the need for real-time, granular, and specific consent when sharing personal data.

In parallel with privacy laws, India has also adopted a techno-legal approach for data sharing, led by the Data Empowerment and Protection Architecture (DEPA). This new-age digital infrastructure introduces a streamlined and compliant approach to consent-driven data sharing.

Today, we are taking the next step in this journey by extending DEPA to support training of AI models in accordance with responsible AI principles. This new digital public infrastructure, which we call DEPA for Training, is designed to address critical scenarios such as detecting fraud using datasets from multiple banks, helping with tracking and diagnosis of diseases, all without compromising the privacy of data principals.

DEPA for Training is founded on three core concepts, digital contracts, confidential clean rooms, and differential privacy. Digital contracts backed by transparent contract services make it simpler for organizations to share datasets and collaborate by recording data sharing agreements transparently. Confidential clean rooms ensure data security and privacy by processing datasets and training models in hardware protected secure environments. Differential privacy further fortifies this approach, allowing AI models to learn from data without risking individuals’ privacy. You can find more details how these concepts come together to create an open and fair ecosystem at https://depa.world.

DEPA for Training represents the first step towards a more responsible and secure AI landscape, where data privacy and technological advancement can thrive side by side. We believe that collaboration and feedback from experts, stakeholders, and the wider community are essential in shaping the future of this approach. Please share your feedback here