iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

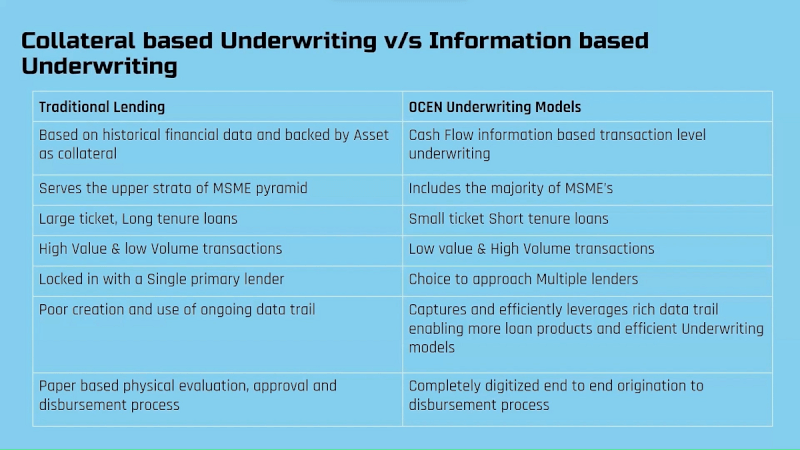

📢Calling all lenders to understand how a short tenor loan can become both an effective and profitable business opportunity under OCEN 4.0. 🔑📈

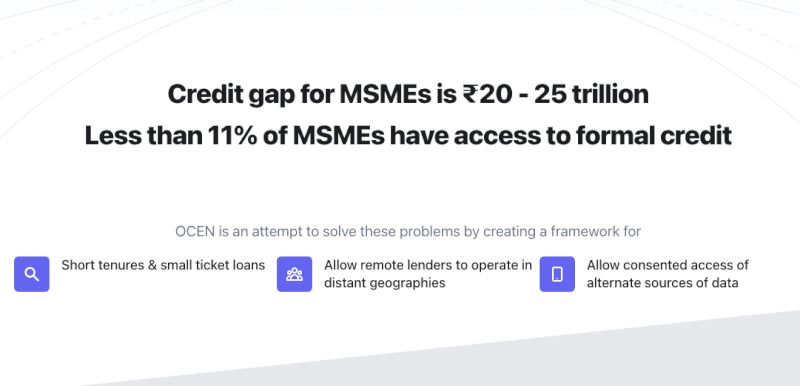

If you are a lender looking for the next big opportunity in lending to the thousands of MSMEs currently unable to access loans, then don’t miss this introduction to OCEN 4.0. 💡

Here we deep-dive into how a new underwriting model enabled by OCEN 4.0 makes it viable and profitable to provide loans to MSMEs traditionally considered unfavourable candidates for loans given the associated high delinquency rates. Our OCEN pilots show, in some cases, it is even possible to create short tenor loans that are twice as profitable as long tenor loans. 🌟🚀🚀

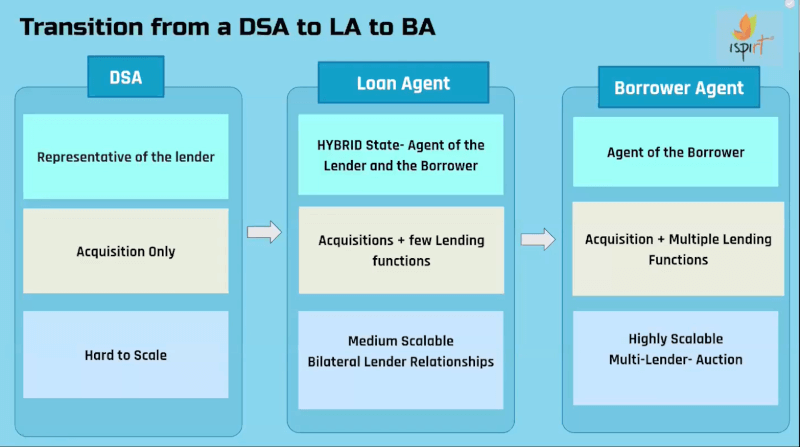

📢Calling all loan agents keen to understand the OCEN 4.0 business opportunity. 🔑📈

OCEN 4.0 introduces a new and powerful role – the Borrowers Agent(BA). If you are looking to play a pivotal role in the MSME lending ecosystem without lending from your own balance sheet, this new role of a BA may be what you want to understand really well. 💡

The BA role is critical to the OCEN story. In this session, we deep-dive on what this role entails, why it is the linchpin of the OCEN 4.0 model, how BAs enable lenders to go remote, and how this role wields a lot of power. We also talk through how to get started, possible business models for BAs and what to focus on to be a successful Borrowers Agent. 🌟🚀🚀

📢👷🧑💻Calling all TSPs and participants eager to dive into OCEN 4.0 APIs.

If you are wanting to understand the tech, the APIs and get started on building for OCEN 4.0, our second open house on OCEN 4.0 is here for you !! 💡

In this session, we do a deep-dive on the architecture, the loan journey on OCEN 4.0 components, the APIs in the OCEN spec and share how you can build for a participant by mocking the APIs of the other. 📝🔑🧑💻

We’re thrilled to unveil OCEN 4.0, the latest advancement in our Open Credit Enablement Network protocol, revolutionizing cash flow-based MSME lending. 🌟

OCEN 4.0 represents a significant leap forward from our ongoing GeM SAHAY and GST SAHAY pilots. In this iteration, along with updated API specifications, we have also added the OCEN Registry, Product Network and rules, specialized participant roles and much more. All these features help us unlock cash-flow-based lending to match the scale, complexity and needs of Bharat. 🔑📈

Check out our introductory open house session on OCEN 4.0

🔍 More details? The API and documentation of OCEN 4.0 are publicly available at http://ocen.dev and will be updated with FAQs from the open house sessions.

🔮 What’s next? Yes, a lot is happening. We have more open house sessions coming out in the following weeks. We are also actively onboarding Wave 1 partners for OCEN 4.0.

❓Questions? Submit your questions here. 📩Contact? Reach the OCEN 4.0 team at [email protected]

Please note: The blog post is authored by our volunteers, Aravind R andSagar Parikh.

India has made rapid progress in digitisation of the economy in the last decade becoming a world leader in identity systems, digital payments and tax, and a new data sharing and empowerment framework. However, many deep-rooted issues still exist, such as extending true financial inclusion; formalisation and creating a higher trust economy, that is essential for growth of mostly small businesses.

In this blog post, we look at innovations in blockchain, distributed ledger and other technologies such as zero-knowledge proofs as potential solutions to build a stronger fabric for the economy for decades ahead. The unique opportunity India has is to boost commerce by enhancing trust, thereby culminating the transformation already underway through existing building blocks of digital identity, payments and data sharing to boost commerce. Unlike many other countries, faster and interoperable payments or reducing the dominance of private money are solved problems for India; the missing piece is to digitise commercial contract enforcement, which on the other hand is a solved problem for developed countries. Lack of adequate contract enforcement caused by contracting parties having different versions of the truth; due to data systems that don’t interoperate reduces trust and creates friction for economic growth. Solution requires connecting the goods and services ledger to the money ledger, so that contracts of any kind become binding promises that can be executed programmatically. Using technology to solve this trust problem is a unique opportunity for India.

BADAL (also happens to be a word for Cloud in local language), a techno-legal solution in the form of “Distributed Ledger for Privacy-preserving Trustful Commerce; is proposed as an interoperable fabric underlying a future programmable economy across large and small businesses to create high trust economy.

We also look at the emergence of Central Bank Digital Currency (CBDC) which is one of the core money applications of this framework and global backdrop in Annexure. There are many other use cases being proposed from land records to decentralised clinical trials for blockchain and allied technologies in different areas of government and business1https://www.meity.gov.in/content/national-strategy-on-blockchain likewise, that can be implemented in BADAL.

First of all, why is trust important?

Trust is the basic glue that connects strangers and promotes economic activity. Money is the basic economic institution in a society building that trust2https://press.princeton.edu/books/paperback/9780691146461/the-company-of-strangers. However, trust builds slowly due to a combination of various factors such as the nature of institutions (political and legal) and the level of formalisation. While formalisation of even small businesses is increasingly addressed by the successful rollout of GST for India, formalisation of trust still remains elusive. At a core fundamental level, trust is a public good that creates friction-free commerce and is a recipe for rapid economic growth.

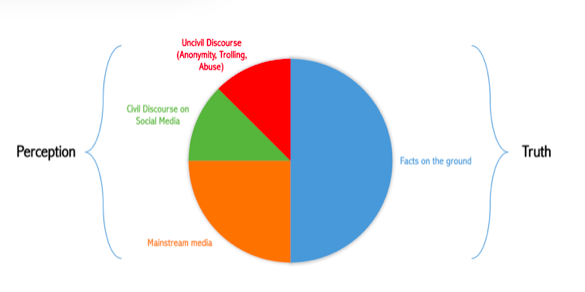

There is a high correlation between the level of trust in society and GDP per capita3https://ourworldindata.org/trust-and-gdp. A study conducted by World Value Survey attempted to measure the level of trust in a country by recording the positive responses received to the question ‘most people can be trusted’. It found that countries with high GDP per capita such as Sweden, Norway and Netherlands recorded high levels of trust exceeding 60% determined in this manner as the graphic below shows.

Douglass C. North, Nobel laureate in economics4https://www.nobelprize.org/prizes/economic-sciences/1993/north/lecture/, found that ‘the inability of societies to develop effective, low-cost enforcement of contracts is the most important source of both historical stagnation and contemporary underdevelopment.’ The Union Minister of Finance and Corporate Affairs has rightly acknowledged the role of the “Hand of Trust”5https://pib.gov.in/PressReleasePage.aspx?PRID=1601273when presenting the Economic Survey of 2019-20.

In societies like India, with limited ability to efficiently enforce routine civil or property contracts, businesses tend to restrict working with those similar to them based on caste, religion etc. (called associational activity) where there is an implicit social and moral enforcement mechanism or with members who have clearly demonstrated reputation in the past (usually the large or the older players). In both these situations, the economic benefit that a new firm can bring with new ideas or new techniques will be muted as its absorption is slower. Similarly, a new player will find it very difficult to compete with incumbents even if such players are economically more efficient. Economist Olson6Olson, M. (1974). The logic of collective action. Harvard University Press showed that associational activity is often more detrimental than favourable for an emerging economy. So we need better ways to break this trust logjam. Trust in the money system in India is comparatively high, as promises tend to be kept with sufficient legal backing and can be digitised with e-mandates or automated payments/ collections; but the same is not the case for goods (or services) ledger, leaving room for delays cascading into a logjam resulting in low trust. This is often felt in day to day life by citizens not getting routine services despite advance payment or small businesses not getting paid despite having supplied goods. Delays, defaults and disputes can become the norm if parties have different versions of the truth.

Every economic activity is thus like a mini-contract with one side on the money ledger (payment from party A to B) and the other side, on the goods/services ledger (from B to A) between counterparties, and can be converted into an electronic contract that automatically executes on both ledgers subject to interoperability. To assure the performance of contracts, the money ledger and the goods/ services ledger need to be connected in a way that is scalable, privacy-enhancing, non-repudiable and programmable. This enables a contract agreed between parties becomes a commitment, and fulfilment is guaranteed by code through the electronic contract. Assuring performance of contracts is critical for a country that is seeking to grow through startup activity, not just in tech but other sectors too.

Currently, litigants lose nearly ₹ 50,000 crores annually in wages or business lost which comes to 0.5% of the country’s GDP, because of litigation, an indication of how expensive litigation can be. The majority of civil disputes in courts are related to recovery of money (30.2 per cent) and land-or property-related matters (29.3 per cent) As reported in the 2016 survey carried out by DAKSH. Common reasons for dispute are different versions of the truth of contracting parties, prior to contract (past) or during the performance of contract (future). Having the same truth and programmability inherent in electronic contracts is a boon in this regard.

In an earlier blog, we have explored the benefits of adapted blockchain technologies to solve the problem of SME financing in India with a related post by global experts7https://balajis.com/add-crypto-to-indiastack/. We build further on that and believe that India can harness recent advances associated with blockchain technology to enable trust between unrelated parties by combining the best of the scalable and centralized legacy world with a secure and private decentralized world. This can benefit the real economy vastly along with the financial world.

Innovations in distributed ledger technologies and BADAL

Distributed Ledger technology can help in two ways – first by being able to verify past performance before one party strikes a deal with another, and second, by being able to enforce a contract in most situations as performance unfolds in future. Thus, building trust about the past as well as the future.

We thus imagine a fabric based on the following basic principles to help create and grow a large number of applications to record economic activity even while reconciling with other activities and past data and help inject a level of trust by creating a reliable, immutable record of trusted data records and programmable contracts

Single platform to allow standards bodies and organisations to publish their schemas, and reuse other schema elements in composing workflows

Fully privacy-preserving capabilities to allow participants to publish relevant zero-knowledge proofs which do not require private data to be shared beyond the participating entities

A programmatic contracts capability that can help automatically carry out the relevant tasks as agreed on without any further manual intervention

By connecting a new digital money ledger (such as Central Bank Digital Currency, or stablecoins) with the new goods & services ledger, we envisage a boost to trust across economy and commerce. As such, BADAL is the first such framework we are aware of globally, uniquely suited to India’s needs, opportunities and strengths.

We have discussed the early version of this in detail in an earlier open-source document8https://github.com/iSPIRT/ppl, called Public Private Ledger. BADAL is thus a privacy supporting, trust enhancing mechanism of coordinating economic activity, and information recording and sharing. Originally this group started out of a process to explore the domain around and figure out the appropriate model to support CBDC, support data sharing between participants, and coordination and automation of event-based standing instructions across events in the goods and services ecosystem and/or money flow.

We then reviewed exciting developments in related areas first to understand their relevance given India’s unique needs. Blockchain technologies generally are seen to enable unrelated parties to trust each other and transact without depending on a central institution or intermediary. These technology innovations are around three key areas:

Maintaining immutability and integrity of data across the distributed ledgers of parties.

Governance mechanisms, especially for decentralised networks

The programmability of such transactions to allow automatic execution.

Public blockchain technologies like Bitcoin and Ethereum, on the other hand, are based on a philosophy of distrust of centralised institutions like Central Banks and are designed for unrestricted access and decentralised decision-making. But they have had to develop new approaches to contend with a few challenges, especially given the huge growth off late that see further wor:

The enormous consumption of resources to establish ‘proof of work’ that limits efficiency and scalability, leading to newer approaches

Exposing all transactions on these networks that generally do not allow sensitive data to be private on the key layer, is as critical for confidential business data as it is for personal data

Rise of many networks that are not interoperable with each other or with the mainstream economy, though some bridges do exist

May have ability to operate outside banking conduits and regulatory frameworks that challenges government’s sovereignty and financial stability through greater oversight has been coming recently

Research on amending throughput, reducing costs and enhancing privacy/auditability/KYC compliance has been ongoing at a rapid pace, especially over the last couple of years.

Despite these unresolved issues, Public blockchain-based tokens, so-called cryptocurrencies, NFTs etc have become an unregulated asset class, especially amongst the young rapidly given the ease of use, creating concerns on possible misuse as well as potential opportunities. We were also part of the recent consultation of the Parliamentary Committee on Finance on ‘Cryptoassets: Opportunities and Challenges’ and had shared with them some of our ideas above in our submission here9https://docs.google.com/document/d/e/2PACX-1vShkuTno_bSILFZPf-Cb_KNwwgM6A_6OgyRiASNS0tXB3ViriHztovrkL7sebiAC7O54y0uwQheTdin/pub.

Various solutions have been employed to address some of these challenges:

Permissioned blockchains, such as Hyperledger Fabric and Corda, allow only trusted parties to participate. Corda uses Notaries for verifying transactions. Such solutions have been successfully used in finance, supply chain, property rights, healthcare, education and e-governance

Zero-knowledge Proofs (ZKPs) allow proving/verification of specific aspects of data without actually making the data public

BADAL builds on the above primitives and is offered as an open and interoperable platform to enable money ledgers such as CBDC/stablecoin along with applications relevant for finance and commerce. This can be designed as a permissioned network relying upon a few regulated entities, and interoperable to ensure that its benefits are widespread and at much lower costs than permissionless systems. It consists of a private ledger that holds sensitive user data withaccess restricted to participating entities only, and a public ledger that contains notarised zero-knowledge proofs about transactions between users. It supports different schemas (configurations) that enable usage across different use-cases.

This programmability coupled with immutability akin to electronic contracts, allows applications in BADAL to be used to leapfrog the trust logjam, without diluting sovereign privileges of control of money given India’s stage of development. BADAL will thus establish provenance that helps establish credibility and reputation of transacting parties, proof of title/ownership of goods and assets, proof of the history of transactions including promises made and ambiguously defined and fulfilled; automatic execution of terms of contracts along with privacy as a fundamental right.

Historically, monetary accounting has solved for only one side of this metaphorical coin- the monetary value. All monetary systems denote a money value to any transfer of goods or services. BADAL, being a ledger that can record value in any domain, solves for the non-monetary aspect of the transaction. Integrated with electronic contracts for a variety of applications, BADAL will enable digital claims on non-monetary assets, including new age asset classes such as crypto assets, NFTs, where claims can be financialized and liquidated. An inherent promissory layer can be enabled into the current transaction mechanism. This extends to all data types, from land records to hospital quality service quality etc, rather than just transactions involving money and goods/ services.

The ability to connect any of the data types across domains can give rise to massive amount of efficiency gains with automated execution thanks to new data from machines like cars, consumer durables like refrigerators or health wearables coming from advances in IoT (Internet of Things), 5G, Imagine a use case of automated crop insurance with sensors that monitor weather from a satellite in space to moisture in soil etc. and deliver claim benefit to the farmer with zero friction in real-time.

One of the biggest problems BADAL could solve at bottom of the pyramid is financial inclusion in India. This is not only in the form of increased monetary transactions through it, but also the ability for MSME’s to gain cheaper credit. This is a possibility as MSME’s will find it easier to prove their liquidity and income to banks and other lenders due to the monetary traceability the system will provide. An increased ability to prove financial stability will lead to greater leverage for borrowers and more systemic trust for lenders. This increase in the systemic trust will not only lead to an increase in credit creation but catalyse an increase in money velocity in India as a whole.

In a subsequent blog post, we will detail the potential use cases; as well as preliminary design of a prototype of one sample use case that is being built currently.

BADAL fabric supporting India Stack could boost digital India

India has pioneered transformations in Identity, Payments, and Data empowerment (these building blocks are popularly called the India Stack) through a techno-legal approach. These address friction of doing business, information asymmetry, and distributed systems. Breakthroughs along the way were public platform (identity), public protocols and standards, and techno-legal approaches to solving big societal problems.

The recent launch of the Account Aggregator (AA) model (based on Data Empowerment and Protection Architecture, DEPA) allows the controlled sharing of private financial data by citizens with various financial institutions to get the best deals. This is a global first and in some sense, an export of a truly global standard12https://twitter.com/Product_nation/status/1435997280692158464?s=20 from India.

Open Credit Enablement Network (OCEN) is creating a way to democratise access to credit, to the level of making it accessible to a street vendor for small sums. These public goods prevent any large player from monopolising the data ecosystem and at the same time reduce the cost of providing service. For instance, microloans as small as Rs.300 can be availed on GeM-SAHAY leading to true inclusion at the bottom of the pyramid.

These techno-regulatory concepts are now being considered for adoption by several countries across the world. Overall, India is arguably ahead of most countries in adopting technology for promoting financial inclusion as well13https://www.bis.org/publ/bppdf/bispap106.pdf.

Image Courtesy: Ananya Phadke

The next building block now is the trust layer through BADAL, ensuring every commitment is met and every contract is enforceable, boosting transparency and growth over the next decade. Trust permeates through all three ends of this triangle as identity is the ‘who’; and data and payment relate to ‘what’ of commerce. In BADAL, identity and data sharing can be achieved without diluting privacy to enable trusted payments (& commerce).

Annexure: CBDC Developments

While BADAL provides fabric to money or goods ledgers, we describe CBDC in detail here, given its importance. Money was traditionally issued by the sovereign (through a Central Banker) and circulated in the economy through layers of banking intermediaries. With the advent of permissionless public blockchains, some of which also seek to portray themselves as alternate currencies, the sovereigns have taken note and introduced their own variant as a public good to protect the financial stability of the nation-states. This sovereign/state-issued digital currency is popularly known as Central Bank Digital Currency (CBDC).

While there are different types of CBDCs such as wholesale/ retail and account-based/ token-based, ultimately a payment using CBDC can be immediately settled. This is akin to using paper money and unlike a cheque or money transfer between bank accounts that require a process of clearing and settlement adding to inefficiency and costs. CBDC can potentially thus leapfrog depending upon the development of existing banking systems in different countries.

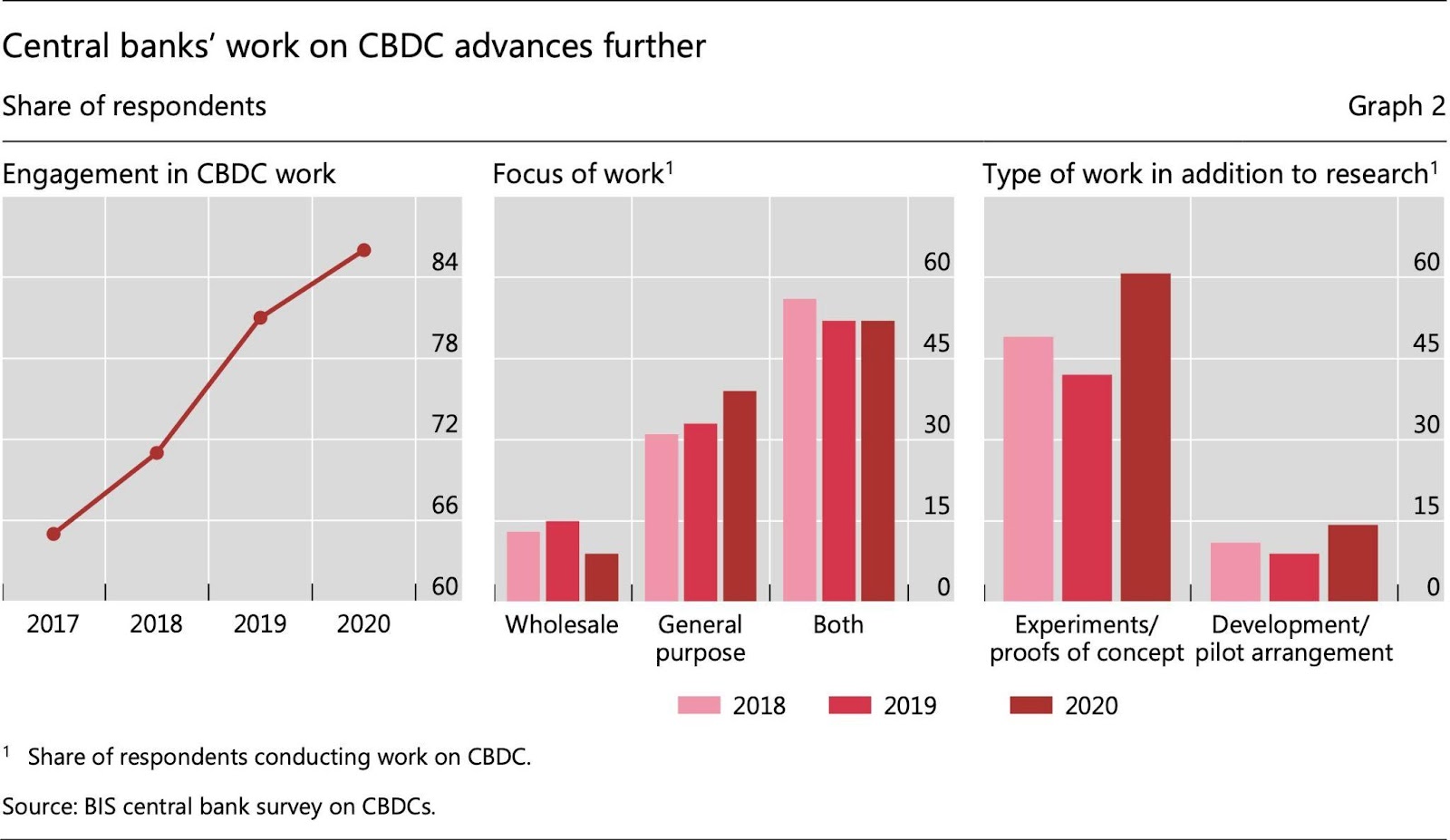

Advanced Economies (AEs) and Emerging Markets and Developing Economies (EMDEs) have different motivations for issuing CBDC to end-users (via Retail CBDC) and financial institutions (via Wholesale CBDC), illustrated in the diagram below.

In the USA, payments are expensive due to its legacy system of banking. This has led to a burst of digital payment options, the latest being ‘stablecoin assets’ (digital currencies backed by real assets like US dollar, treasuries, etc) that also compete with their money-market funds. Stablecoin assets have crossed $100 billion25https://www.statista.com/statistics/1255835/stablecoin-market-capitalization/ in market value and are a popular choice to transact in Decentralised Finance (DeFI). DeFi is a parallel financial system evolving around crypto-assets. DeFI is not subject to transparency and compliance required in the conventional financial world at this point in time. As DeFi becomes big and interacts with the conventional financial world, there is a growing systemic risk arising from failure or fraud in DeFi. The US Government, therefore, wants to regulate some aspects of DeFI26https://www.federalreserve.gov/monetarypolicy/fomcminutes20210728.htm and may thereby bless some stablecoins and crypto-assets as explicitly permitted financial products. Earlier in 2015, Bitcoin was determined to be a commodity27https://www.cftc.gov/sites/default/files/2019-12/oceo_bitcoinbasics0218.pdf by some authorities there. The US Fed has also begun a consultation process towards design choices and feasibility of CBDC implementation.

Indian perspective

In India, the focus of policy has rightly been on promoting financial inclusion to formalise the economy and drive economic growth. One important factor which drives the usage of unregulated informal value transfer systems is the lack of banking facilities and corresponding amenities for managing money, which leaves rural communities without alternatives other than a person-to-person method of transferring monetary value. Even though India has seen a significant increase in the number of bank accounts created, Reserve bank data still highlights little improvement in account usage and institutional borrowings, which feeds into the broader issue of financial inclusivity.

Initiatives like Pradhan Mantri Jan-Dhan Yojana (PMJDY) opened doors to big change. UPI has been very successful as a payment mode but still needs underlying bank accounts to transact and thus depends on the banking system & its motivation to provide access to the poor. The PMJDY scheme announced in 2014 has increased the number of adults with bank accounts to 43.47cr 28Progress Report as on 22-Sep-21, PMJDY, MOF, GOI, https://pmjdy.gov.in/account (~46% of 93.55cr adults with an Aadhaar29https://uidai.gov.in/images/Saturation_Report_State-UT_Agewise_31-08-2021.pdf). Despite this headway, there is still a lot to be achieved. The Financial Inclusion Index (FI) recently launched by RBI shows that India is at 53.9 on March 21 (vs 43.4 in March 2017) – a little more than halfway towards complete financial inclusion (FI of 100)30https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52068. Presently, the banking system acts as the main gateway to financial inclusion as the banking system is the main distributor of cash. Hence, various government programmes (like PMJDY) rely upon banks for financial inclusion, despite those being not remunerative for banks. The accounts also have various restrictions on the number of debits/withdrawals to ensure low cost.

Even with the existence of such low-cost bank accounts, the poor do not have an incentive to use a bank account regularly as they do not save enough to use the bank account as a store of value. They use these accounts mainly to collect remittances and withdraw cash at ATMs as bulk of their transactions is in cash, not leaving a visible money trail that in turn makes financial inclusion difficult. Cash in circulation in India even now is Rs 29.38 trillion31https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52274 (~14.9% of estimated GDP for 2020-2132http://mospi.nic.in/sites/default/files/press_releases_statements/Statement_12_1st+September+2021.xls) despite the availability of these cheaper accounts, demonetisation in 2017 and the subsequent formalisation of the economy with GST, RERA, etc.

In addition, the cost of handling cash by the central bank and commercial banks (currency printing, operating currency chests, logistics of moving currency, ATM operations, etc.) has been estimated to be ~Rs 21,000 cr (Rama Bijapurkar) and ~1.7% of GDP ( (Visa Inc., 2016). High adoption of CBDC can help in reducing this cost while creating enormous amounts of data and enabling policymakers to diagnose and regulate better. At a later stage, CBDC can also be used for targeted monetary policy actions when its impact on the financial system is well understood. Experts are concerned that CBDC may result in the disintermediation of the financial system. This risk can be mitigated by following design principles set out by the Bank for International Settlements (BIS)33https://www.bis.org/press/p201009.htm (i) “do no harm” to monetary and financial stability; (ii) coexist with cash and other types of money in a flexible and innovative payment ecosystem; and (iii) promote broader innovation and efficiency.

CBDC inherently provides an alternative to cash to directly reach a customer and can complement the banking network to make adoption quicker. By providing a digital alternative to cash will enable building verifiable money trails that can lead to greater financial inclusion by private players providing customised health, insurance, investment & education products in compliance with privacy laws. In the financially excluded segments, CBDC, being a form of central bank currency, is likely to be well trusted and be adopted easily.

The blog post is co-authored by Sanjay Phadke, Dhananjay Nene, Sharad Sharma, Navin Kabra, R Barve, K Babel, V Agarwal, K Gokarn, Kalyan Narguru, Shashank B, Arun Maharajan, Karan Sirdesai, P Sahu, P Rao, A Kulkarni, Krishna Iyer, V Nene and A Lath.

If you have any queries or comments, please contact us at [email protected].

There are no atheists in foxholes, and there appear to be no capitalists in a global pandemic either. The head of Honeywell’s billion-dollar GoDirect Trade platform, which uses a permission-based blockchain to buy and sell aviation parts, declared on March 20 that American corporations had a “walled-garden” approach to data. “They need to start sharing data, a huge paradigm shift”, said Lisa Butters. Only a couple of weeks ago, Honeywell had been defending the virtues of a permission-based system, saying enterprises “needed some constraints to operate in”.

What a difference a few days can make.

Historically, the aviation industry has been one of the most secretive among ‘Big Tech’ sectors, with its evolution tied intimately to the Second World War, and the US-Soviet Cold War rivalry that followed soon after. Concerns around China’s theft of aerospace IP was among the foremost drivers behind the Obama administration’s negotiation of the 2015 agreement with China to prohibit “economic espionage”. It is the ultimate “winner-takes-all” market — but Boeing, its lynchpin, has now approached the US government for an existential bailout. Honeywell’s call for a “paradigm shift” is proof that the sector is not thinking just in hand-to-mouth terms. The aviation sector may get a lifeline for now, but as an industry forged by a global war, it knows more than most that a transformational moment for technology is upon it, which needs to be seized.

As the economist Branko Milanović has highlighted, the correct metaphor for the Covid-19 pandemic and ensuing crisis is not the Great Recession of 2008, but the Second World War. To win WWII, and retain its military superiority, the United States pioneered technology complexes that placed innovation at the trifecta of a university lab, government, and market. (The blueprint for this model was drawn up in 1945 by Vannevar Bush, founder of Raytheon and director of the Office for Scientific Research and Development, and presented to the US government. The document was titled, “Science: The Endless Frontier”.) This was by no means a Western endeavour alone. Several countries, including India, followed suit, trying to perfect a model of “organised science”. In India, the Council for Scientific and Industrial Research was the totem for this effort and created a centralised network of national labs. The primary difference between Western models and ones in developing countries like India was the role of the state. In the US, the state retained regulatory agency over the process of technological innovation, but gradually ceded into the background as the Boeings, Westinghouses, GEs, Lockheed Martins, and IBMs took over. In India, the state became both the regulator and purveyor of technology.

India’s attempts to create “national champions” in frontier technologies (think Hindustan Antibiotics Ltd, Electronics Corporation of India Ltd, Defence Research and Development Organisation, etc) failed because the state could not nimbly manufacture them at scale. Even as India pursued “moonshots”, those businesses in the United States that were incubated or came of age during the Second World War began to occupy pole positions in their respective technology markets. Once those markets matured, it made little sense for America to continue creating “organized” technology complexes, although research collaborations between universities and the federal government continued through the National Science Foundation. The banyan-ization of the internet and Silicon Valley — both seeded by generous assistance from the US Department of Defence — into a market dominated by the FAANG companies affirms this shift.

In the wake of the Covid-19 pandemic, however, the tables are turning. The United States is not only shifting away from “moonshots” but also pivoting towards “playgrounds”, settling on a model that India has perfected in the last decade or so.

The United States has often sought to repurpose private technologies as public utilities at key moments in its history. Communications technology was built and moulded into a public good by the American state. It was US law that enabled patent pooling by Bell Labs in the 19th century, leading to the creation of a “great new corporate power” in telephony. A few decades into the 20th century, American laws decreed telephone companies would be “common carriers”, to prevent price and service discrimination by AT&T. Meanwhile, both railroads and telecommunications providers were recognised as “interstate” services, subject to federal regulation. This classification allowed the US government to shape the terms under which these technologies grew. IT is precisely this template that Trump has now applied to telehealth technology in the US. Tele-medicine services could not previously be offered across state lines in the US, but the US government used its emergency powers last week to dissolve those boundaries. And on March 18, President Trump invoked the Defence Production Act, legislation adopted during the Korean War and occasionally invoked by American presidents, that would help him commandeer private production of nearly everything, from essential commodities to cutting-edge technologies.

Invoking the law is one thing, executing it is another. Rather than strong-arming businesses, the Trump administration is now trying to bring together private actors to create multiple “playgrounds” with an underlying public interest. The Coronavirus Task Force was the first of its kind. The Task Force brought together Walmart, Google, CVS, Target, Walgreens, LabCorp and Roche, among others to perform singular responsibilities aimed at tackling the coronavirus pandemic. Walmart would open its parking lots for testing, Google would create a self-testing platform online, Roche would develop kits, LabCorp would perform high-throughput testing, and so on. The COVID-19 High-Performance Computing Consortium, created on March 23, is another such playground. It includes traditional, 20th-century actors such as the national laboratories but is doubtless front-ended by Microsoft, IBM, Amazon and Google Cloud. The Consortium aims to use its high computational capacity to create rapid breakthroughs in vaccine development. Proposals have been given an outer limit of three months to deliver.

In some respects, the United States is turning to an approach that India has advanced. To be sure, we may not currently be in a position to develop such a playground for vaccine R&D and testing at scale. But India is well-positioned to create the “digital playgrounds” that can help manage the devastating economic consequences of the Covid-19 epidemic. There is a universal acknowledgement that India’s social safety nets need to be strengthened to mitigate the fallout. One analyst recommends “a direct cash transfer of ₹3,000 a month, for six months, to the 12 crores, bottom half of all Indian households. This will cost nearly ₹2.2-lakh crore and reach 60 crore beneficiaries, covering agricultural labourers, farmers, daily wage earners, informal sector workers and others.” The same estimate suggests “a budget of ₹1.5- lakh crore for testing and treating at least 20 crore Indians through the private sector.”

The digital public goods India has created — Aadhaar, UPI and eKYC — offer the public infrastructure upon which these targeted transfers can be made. However, cash transfers alone will not be enough: lending has to be amplified in the months to come to kickstart small and medium businesses that would have been ravaged after weeks of lockdown. India’s enervated banking sector will have meagre resources, and neither enthusiasm or infrastructure to offer unsecured loans at scale. “Playgrounds” offers private actors the opportunity to re-align their businesses towards a public goal, and for other, new businesses to come up. Take the example of Target, which is an unusual addition to the Coronavirus Task Force, but one whose infrastructure and network makes it a valuable societal player. Or Amazon Web Services in the High-Performance Computing Consortium, which has been roped in for a task that is seemingly unrelated to the overall goal of vaccine development.

If digital playgrounds are so obvious a solution, why has India not embraced it sooner? None of this is to discount the deficit of trust between startup founders and the public sector in India. Founders are reluctant to use public infrastructure. It is the proverbial Damocles’ sword: a platform or business’ association with the public sector brings it instant legitimacy before consumers who still place a great deal of trust in the state. On the other hand, reliance on, or utilisation of public infrastructure brings with it added responsibilities that are unpredictable and politically volatile. To illustrate, one need only look at the eleventh-hour crisis of migrating UPI handles from YES Bank in the light of a moratorium imposed on the latter earlier this month. On the other hand, the government retains a strong belief that the private sector is simply incapable of providing scalable solutions. In most markets where the India government is both player and regulator, this may seem a chicken-and-egg problem, but c’est la vie.

Nevertheless, there are milestones in history where seemingly insurmountable differences dissolve to reveal a convergence of goals. India is at one such milestone. A leading American scientist and university administrator have called the pandemic a “Dunkirk moment” for his country, requiring civic action to “step up and help”. By sheer chance and fortitude, India’s digital platforms are poised to play exactly the role that small British fishing boats played in rescuing stranded countrymen on the frontline of a great war: they must re-imagine their roles as digital platforms, and align themselves to strengthen the Indian economy in the weeks to come.

Arun Mohan Sukumar is a PhD candidate at the Fletcher School, Tufts University, and a volunteer with the non-profit think-tank, iSPIRT. His book, Midnight’s Machines: A Political History of Technology in India, was recently published by Penguin RandomHouse.

In 1941, soon after he had secured an unprecedented third term as President of the United States, Franklin D. Roosevelt mobilised the US Congress to pass the Lend-Lease Act. Its context and history are storied. British Prime Minister Winston Churchill famously wrote to FDR requesting material assistance from the United States to fight Nazi Germany — “the moment approaches when we shall no longer be able to pay [to fight the war]”. FDR knew he would not get the American public’s approval to send troops to the War (Pearl Harbor was still a few months away). But the importance of securing the world’s shipping lanes, chokepoints, manufacturing hubs and urban megalopolises was not lost on the US President. Thus, the Lend-Lease Act took form, resulting in the supply of “every conceivable” material from the US to Britain and eventually, the Allied Powers: “military hardware, aircraft, ships, tanks, small arms, machine tools, equipment for building roads and airstrips, industrial chemicals, and communications equipment.” US Secretary of War Henry Stimson defended the Act eloquently in Congress. “We are buying…not lending. We are buying our own security while we prepare,” Stimson declared.

The analogy is not perfect, but FDR’s Lend-Lease Act offers important lessons for 21st century India’s digital economy. Our networks are open; our public, electronic platforms are free and accessible to global corporations and start-ups; our digital infrastructure is largely imported; and — pending policy shifts — we believe in the free flow of information across territorial borders. India has made no attempt, and is unlikely in the future, to wall off its internet from the rest of the world, or to develop technical protocols that splinter its cyberspace away from the Domain Names System (DNS). While we have benefited immensely from the open, global internet, what is India doing to secure and nourish far-flung networks and digital platforms? The Land-Lease Act was not just about guns and tanks; a quarter of all American aid under the programme comprised agricultural products and foodstuff, including vitamin supplements for children. The United States knew it needed to help struggling markets in order to build a global supply chain that would serve its own economic and strategic interests. Indeed, this was the very essence of the Marshall Plan that followed a few years later.

In fact, India’s digital success story itself is a creation of global demand. When the Y2K crisis hit American and European shores, Indian companies stepped up to the plate and offered COBOL-correction ‘fixes’ at competitive rates. In the process, Western businesses saved billions of dollars — and Y2K made computing ubiquitous in India, which in turn, added great value to the country’s GDP.

Therefore, there are both security-related concerns and economic consequences that should prompt India to develop “digital public goods” for economies across Asia, Europe and Africa. Can India help develop an identity stack for Nigeria — a major source of global cyberattacks — that helps Abuja mitigate threats directed at India’s own networks? Can we develop platforms for the financial inclusion of millions of undocumented refugees across South and Southeast Asia, that in turn reduces economic and political stress on India and her neighbours when confronted with major humanitarian crises? Can we build “consent architecture” into technology platforms developed for markets abroad that currently have no data protection laws? Can we nurture the creation of an open, interoperable and multilateral banking platform that replaces the restrictive, post-9/11, capital controls system of today with a more liberal regime — thus spurring financial support for startups across India and Asia? Can India — like Estonia — offer digital citizenship at scale, luring investors and entrepreneurs who want to build for the next billion, but do not have access to Indian infrastructure, markets and data? These are the questions that should animate policy planners and digital evangelists in India.

The Indian establishment is not unmindful of the possibilities: in 2018, Singapore and India signed a high-level agreement to “internationalise” the India Stack. The agreement has been followed up with the creation of an India-Singapore Joint Working Group on fintech, with a view towards developing API-based platforms for the ASEAN region. As is now widely known, a number of countries spanning regions and continents have also approached India with requests to help build their own digital identity architecture.

But the time has come to elevate piecemeal or isolated efforts at digital cooperation to a more coordinated, all-of-government approach promoting India’s platform advancements abroad. The final form of such coordination may look like an inter-ministerial working group on digital public goods, or a division in the Ministry of External Affairs devoted exclusively to this mission. Whatever the agency, structure or coalition looks like within government, its working should be underpinned by a political philosophy that appreciates the strategic and economic value accrued to India from setting up a “Global Stack”. In 1951, India was able to successfully tweak the goals of the Colombo Plan — which was floated as a British idea to retain its political supremacy within the Commonwealth — to meet its economic needs. Working together with our South Asian partners and like-minded Western states like Canada, we were able to harvest technology and foreign expertise for a number of sectors including animal husbandry, transportation and health services. India was also able, on account of skilful diplomacy, to work around Cold War-era restrictions on the export of sensitive technologies to gain access to them.

That diplomacy is now the need of the hour. The world today increasingly resembles FDR’s United States, with very little appetite to forge multilateral bonds, liberal institutions, or rules to create effective instruments of global governance. It took tact and a great deal of internal politicking from Roosevelt to pry open the US’ closed fist and extend it to European allies through the Lend-Lease Act. India, similarly, will need to convince its neighbours in South Asia of the need to create platforms at scale that can address socio-economic problems common to the entire region. This cannot be done by a solitary bureaucrat working away from some corner of South Block. New Delhi needs to bring to bear the full weight of its political and diplomatic capital behind a “Global Stack”. It must endeavour to create centripetal digital highways, placing India at the centre not only of wealth creation but also global governance in the 21st century.

The blog post is authored by Arun Mohan Sukumar, PhD Candidate at The Fletcher School at Tufts University, and currently associated with Observer Research Foundation. An edited version of this post appeared as an op-ed in the Hindustan Times on October 21, 2019.

Last week we wrote about India’s Health Leapfrog and the role of Health Stack in enabling that (you can read it here). Today, we talk about one component of the National Health Stack – Federated Personal Health Records: its design, the role of policy and potential use cases.

Overview

A federated personal health record refers to an individual’s ability to access and share her longitudinal health history without centralised storage of data. This means that if she has visited different healthcare providers in the past (which is often the case in a real life scenario), she should be able to fetch her records from all these sources, view them and present them when and where needed. Today, this objective is achieved by a paper-based ‘patient file’ which is used when seeking healthcare. However, with increasing adoption of digital infrastructure in the healthcare ecosystem, it should now be possible to do the same electronically. This has many benefits – patients need not remember to carry their files, hospitals can better manage patient data using IT systems, patients can seek remote consultations with complete information, insurance claims can be settled faster, and so on. This post is an attempt to look at the factors that would help make this a reality.

What does it take?

There are fundamentally three steps involved in making a PHR happen:

Capture of information – Even though a large part of health data remains in paper format, records such as diagnostic reports are often generated digitally. Moreover, hospitals have started adopting EMR systems to generate and store clinical records such as discharge summaries electronically. These can act as starting points to build a PHR.

Flow of information- In order to make information flow between different entities, it is important to have the right technical and regulatory framework. On the regulatory front, the Personal Data Protection Bill which was published by MeitY in August last year clearly classifies health records as sensitive personal data, allows individuals to have control over their data, and establishes the right to data portability. On the technical front, the Data Empowerment and Protection Architecture allows individuals to access and share their data using electronic consent and data access fiduciaries. (We are working closely with the National Cancer Grid to pilot this effort in the healthcare domain. A detailed approach along with the technical standards can be found here.)

Use of information – With the technical and regulatory frameworks in place, we are now looking to understand use cases of a PHR. Indeed, a technology becomes meaningless without a true application of it! Especially in the case of PHR, the “build it and they will come” approach has not worked in the past. The world is replete with technology pilots that don’t translate into good health outcomes. We, in iSPIRT, don’t want to go down this path. Our view is that only pilots that emerge from a clear focus on human-centred design thinking have a chance of success.

Use cases of Personal Health Records

Clinical Decision Making

Description: Patient health records are primarily used by doctors to improve quality of care. Information about past history, prior conditions, diagnoses and medications can significantly alter the treatment prescribed by a medical professional. Today, this information is captured from any paper records that a patient might carry (which are often not complete), with an over-reliance on oral histories – electronic health records can ensure decisions about a patient’s health are made based on complete information. This can prove to be especially beneficial in emergency cases and systemic illnesses.

Problem: The current fee-for-service model of healthcare delivery does not tie patient outcomes to care delivery. Therefore, in the absence of healthcare professionals being penalised for incorrect treatment, it is unclear who would pay for such a service; since patients often do not possess the know-how to realise the importance of health history.

Chronic Disease Management

Description: Chronic conditions such as diabetes, hypertension, cardiovascular diseases, etc. require regular monitoring, strict treatment adherence, lifestyle management and routine follow-ups. Some complex conditions even require second opinions and joint decision-making by a team of doctors. By having access to a patient’s entire health history, services that facilitate remote consultations, follow-ups and improve adherence can be enabled in a more precise manner.

Problem: Services such as treatment adherence or lifestyle management require self-input data by the patient, which might not work with the majority. Other services such as remote consultations can still be achieved through emails or scanned copies of reports. The true value of a PHR is in providing complete information (which might be missed in cases of manual emails/ uploads, especially in chronic cases where the volume and variety of reports are huge) – this too requires the patient to understand its importance.

Insurance

Description: One problem that can be resolved through patient records is incorrect declaration of pre-existing conditions, which causes post-purchase dissonance. Another area of benefit is claims settlement, where instant access to patient records can enable faster and seamless settlement of claims. Both of these can be use cases of a patient’s health records.

Problem: Claim settlement in most cases is based on pre-authorisation and does not depend solely on health records. Information about pre-existing conditions can be obtained from diagnostic tests conducted at the time of purchase. Since alternatives for both exist, it is unclear if these use cases are strong enough to push for a PHR.

Research

Description: Clinical trials often require identifying the right pool of participants for a study and tracking their progress over time. Today, this process is conducted in a closed-door setting, with select healthcare providers taking on the onus of identifying the right set of patients. With electronic health records, identification, as well as monitoring, become frictionless.

Problem: Participants in clinical trials represent a very niche segment of the population. It is unclear how this would expand into a mainstream use of PHR.

Next steps

We are looking for partners to brainstorm for more use cases, build prototypes, test and implement them. If you work or wish to volunteer in the Healthtech domain and are passionate about improving healthcare delivery in India, please reach out to me at [email protected].

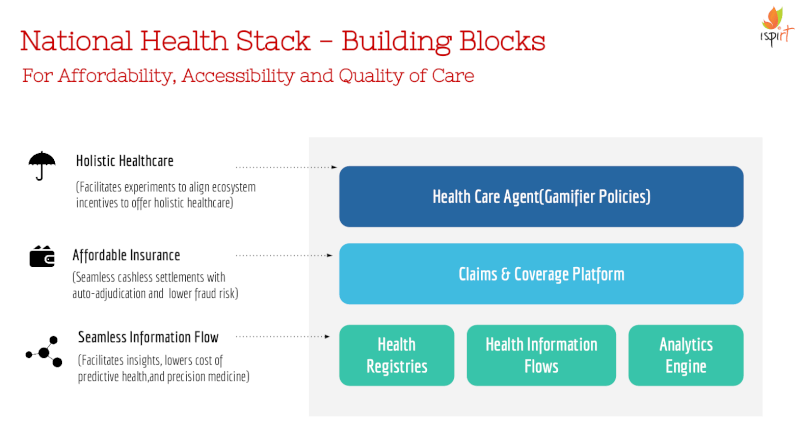

In July 2018, NITI Aayog published a Strategy and Approach document on the National Health Stack. The document underscored the need for Universal Health Coverage (UHC) and laid down the technology framework for implementing the Ayushman Bharat programme which is meant to provide UHC to the bottom 500 million of the country. While the Health Stack provides a technological backbone for delivering affordable healthcare to all Indians, we, at iSPIRT, believe that it has the potential to go beyond that and to completely transform the healthcare ecosystem in the country. We are indeed headed for a health leapfrog in India! Over the last few months, we have worked extensively to understand the current challenges in the industry as well as the role and design of individual components of the Health Stack. In this post, we elaborate on the leapfrog that will be enabled by blending this technology with care delivery.

What is the health leapfrog?

Healthcare delivery in India faces multiple challenges today. The doctor-patient ratio in the country is extremely poor, a problem that is further exacerbated by their skewed distribution. Insurance penetration remains low leading to out-of-pocket expenses of over 80% (something that is being addressed by the Ayushman Bharat program). Additionally, the current view on healthcare amongst citizens as well as policymakers is largely around curative care. Preventive care, which is equally important for the health of individuals, is generally overlooked.

The leapfrog we envision is that of public, precision healthcare. This means that not only would every citizen have access to affordable healthcare, but the care delivered would be holistic (as opposed to symptomatic) and preventive (and not just curative) in nature. This will require a complete redesign of operations, regulations and incentives – a transformation that, we believe, can be enabled by the Health Stack.

How will this leapfrog be enabled by the Health Stack?

At the first level, the Health Stack will enable a seamless flow of information across all stakeholders in the ecosystem, which will help in enhancing trust and decision-making. For example, access to an individual’s claims history helps in better claims management, a patient’s longitudinal health record aids clinical decision-making while information about disease incidence enables better policymaking. This is the role of some of the fundamental Health Stack components, namely, the health registries, personal health records (PHR) and the analytics framework. Of course, it is essential to maintain strict data security and privacy boundaries, which is already considered in the design of the stack, through features like non-repudiable audit logs and electronic consent.

At the second level, the Health Stack will improve cost efficiency of healthcare. For out-of-pocket expenditures to come down, we have to enable healthcare financing (via insurance or assurance schemes) to become more efficient and in particular, the costs of health claims management to reduce. The main costs around claims management relate to eligibility determination, claims processing and fraud detection. An open source coverage and claims platform, a key component of the Health Stack, is meant to deal with these inefficiencies. This component will not only bring down the cost of processing a claim but along with increased access to information about an individual’s health and claims history (level 1), will also enable the creation of personalised, sachet-sized insurance policies.

At the final level, the Health Stack will leverage information and cost efficiencies to make care delivery more holistic in nature. For this, we need a policy engine that creates care policies that are not only personalized in nature but that also incentivize good healthcare practices amongst consumers and providers. We have coined a new term for such policies – “gamifier” policies – since they will be used to gamify health decision-making amongst different stakeholders.

Gamifier policies, if implemented well, can have a transformative impact on the healthcare landscape of the country. We present our first proposal on the design of gamifier policies, We suggest the use of techniques from microeconomics to manage incentives for care providers, and those from behavioural economics to incentivise consumers. We also give examples of policies created by combining different techniques.

The success of the policy engine rests on real-world experiments around policies and in the document we lay down the contours of an experimentation framework for driving these experiments. The role of the regulator will be key in implementing this experimentation framework: in standardizing the policy language, in auditing policies and in ensuring the privacy-preserving exchange of data derived from different policy experiments. Creating the framework is an extensive exercise and requires engagement with economists as well as computer scientists. We invite people with expertise in either of these areas to join us on this journey and help us sharpen our thinking around it.

Do you wish to volunteer?

Please read our volunteer handbook and fill out this Google form if you’re interested in joining us in our effort to develop the design of Health Stack further and to take us closer to the goal of achieving universal and holistic healthcare in India!

Matrix India recently hosted two firebrands of the financial services world, Mr Sanjay Agarwal, founder AU Small Finance Bank and Mr Sharad Sharma, founder iSPIRT Foundation, Volunteer at India Stack, for a no holds barred discussion at the Matrix Rooftop in Bangalore. Here is an excerpt from the evening and some of our learnings for fin-tech entrepreneurs.

Part 1 of the two-part series features the untold story of AU Bank, in the words of Sanjay Agarwal himself, as below:

Sanjay Agarwal – on his background and early days before starting AU:

“In my early Chartered Accountancy days, I started out by doing audit work, taxation, and managing clients. I had studied hard and was naïve and enthusiastic at that time hoping, to solve the world’s problems. This pushed me to work harder and I had a desire to do something more.

I believe that we are the choices we make. While evaluating various choices, I eliminated all the options that I didn’t want to pursue e.g. to work for a fee or commission and then I started digging deeper on what really interests me – that was when the concept of AU Financiers was formed.

In 1996, as 26 years old, I began approaching HNIs to raise capital, as back then, there were no VCs. I was fortunate to raise INR 10 cr at a 12% hurdle rate and I had to secure the funding with a personal guarantee. But what is the guarantee of the guarantor? No one questioned this at that time. So, I technically became one of the first P2P lenders, and structured a product that didn’t exist– short term, secured and at a 30% rate of interest. That was the start of the AU journey.”

The Early Days of AU:

“I started off AU as a one-man army. I was everything from the treasurer to the collector. Slowly we built our team and rotated the 10 cr of capital to disburse 100 cr of loans – not a single rupee was lost. There were several challenges at that time for e.g., there was no CIBIL score, financial discipline was lacking, people were still learning how to take a loan and repay it and customer ids didn’t even have a photograph. But somehow, we managed.

The period from 1996 to 2002 taught me everything I needed to learn – how to lend, how to collect, how to manage people, read people’s body language, and most importantly how to manage yourself in different situations. I follow all of that until today, and my team also benefits or suffers from those learnings of mine even today. In those 7 years, we would have dealt with 2000 customers out of which 500 defaulted. That was the ratio of defaulters – 25%. But we managed and there were actually no NPL’s.”

Partnering with HDFC Bank

“In 2002, retail credit was beginning to take off, but our HNIs started pulling their money out, as they wanted a higher return. However, at that time, the most premium bank in the country, HDFC Bank, appointed us as their channel partner. The model we followed was very simple – AU was responsible for sourcing the customer, KYC processing and doing on the ground diligence while loans were booked on HDFC’s balance sheet. HDFC is perceived to be a conservative bank, and it is – however, they gave me Rs 400 cr, on a net worth of only Rs 5 cr! They made an exception in our case due to our strong track record, through execution, sound knowledge of the market, and most importantly our integrity.

By 2008, our net worth had increased to Rs 10 crore through internal accruals. At that time, HDFC told us that we can’t give you any more capital, as we were overleveraged, and that we now needed to bring in equity capital if we wanted to grow.”

Growing the balance sheet and partnering right

“I had two choices at that point, I could continue in Jaipur, keep my ambition under control and live comfortably or figure out what else is possible. I chose the latter and this marked the beginning of my partnership with Motilal Oswal. Its easier to raise equity now, back in the day shareholder agreements used to look like loan agreements with min IRR requirements, etc. As luck would have it, a few months after we raised equity, the Lehman Brothers crisis broke out and most banks stopped funding. We were supported once again by HDFC – they were our saviour and I will cherish my relationship with them always. Once the market settled down, having survived this negative environment, there was no looking back.

Our next major investor was IFC. For the entrepreneurs here, I want to say that you have to be selective about your investors, who will help with not just capital – there should be added value they bring to the table apart from money. IFC was giving me 20% lower valuation, but I knew that I didn’t have any lineage to fall back on. As a first-generation entrepreneur, I had to raise money on the strength of my balance sheet and not basis my family name. I knew that partnering with IFC would shift the perception of AU within the industry, especially for PSU banks. After their investment, we grew from one bank relationship with HDFC to 40 bank partnerships. One thing led to another and Warburg Pincus, ChrysCapital, and Kedaara Capital all came on board after that.”

Consistent performance

“From 2008 onwards, we started diversifying from vehicle lending and got into other forms of secured lending like a loan against property, home loans etc. We never tried unsecured lending and never ventured into microfinance or gold finance. Those were very popular products at that time but focusing on what we were good at resulted in a consistently strong performance. We never had a bad year. In the world of finance, the margin of error is very less. If you have a bad year you can almost never come back. Good companies survive regardless of the market condition, you can never blame the market for your company’s poor performance. In 2015-16, we were a successful NBFC, our RoA was close to 3% with an asset base of close to 8,000 crores, with a RoE of 27-28% and everyone was chasing us – the question at that time before us was, what next?”

How we became a bank

“As an NBFC, it is very hard to manage a book of Rs 50,000 cr with the same efficiency and effectiveness as it’s a people dependent business, there are limits to the kind of products you can do and you can’t keep raising capital. Hence, we became a bank because we wanted to be there for the next 100 years and that perpetual platform can only be created through a bank. That is the biggest platform and it is not available at a price. It’s available through your integrity, business plan and execution. Today, we receive Rs 100 cr of money every single day. This is the same person who was struggling to raise Rs 10 cr in 1996, and is now getting money at the speed of Rs 100 cr every day – it feels amazing but there is a lot of responsibility!”

Part 2 of the two-part series features insights from Sharad Sharma:

Recognizing the Athletic Gavaskar moment in Indian Financial Services

“Indian financial services industry is going through its equivalent of the Athletic Gavaskar project of Indian cricket. The motive behind this project was to instil the importance of being athletic to successfully compete in the modern game. A new team was created with the rule that if you are not athletic, you cannot be a part of the team, regardless of other skills that you bring to the table. Virat Kohli eventually became the captain of this team and the results are for everyone to see. Similar yet contrasting stories played out in hockey and wrestling. In hockey, we lost for 20 years because we refused to adapt to the introduction of astroturf. However, in wrestling, the Akhadas in Haryana embraced the move from mud to mat with rigour, and Indian wrestling is already punching above its weight class and hopefully will do even better over time. The idea of sharing this is that similar to sports, sometimes an industry goes through a radical shift. Take the telecom space, for example, if Graham Bell came alive in 1995, he would recognize the telephone system, 20 years later he wouldn’t recognize it at all. The banking industry is going to go through a hockey/wrestling or communications type disruption and a lot of us are working hard to make it happen.”

Infrastructure changes lead to New Playgrounds

“All the banks and NBFCs put together are not serving the real India today. We have 10 million+ businesses that have GST id’s, out of which 8 million+ are big enough to pay GST on a monthly basis, but only 1.2 million have access to NBFC or bank finance. This is a gap that needs to be addressed and it cannot be solved through incremental innovations.

Entrepreneurs and incumbents should learn from what happened in the TV industry when new infrastructure became available. When India went from state-run TV towers in 34 cities to cable and satellite TV in pretty much every town, there was a massive new market that was unlocked that did not want to watch the same Ramayan or Hum Log TV serials. What transpired was an explosion of entertainment products because of the high demand stemming from the new markets and the TV channel players that reinvented their content is thriving today while others that did not, are barely surviving or have shut down.

So where does this leave the bankers? I think it is the biggest opportunity for the right banker who understands this problem, wants to serve this section of the market and is willing to reinvent the way they do their business and take advantage of the new infrastructure that will be available.”

Dual-immersed entrepreneurs have the biggest advantage

“Entrepreneurs who are immersed in the messiness of both the new infrastructure and the old problem are “dual immersed entrepreneurs”. They are the ones that succeed when a market shift is underway. Today this is not happening. Some of our city-bred entrepreneurs are more comfortable with California rather than Bharat. And some of our sales-oriented entrepreneurs are intimidated by the messiness of the new technology infrastructure.”

New Playgrounds need new Gameplay

“In a world where eKYC exists, and we can transfer money through UPI from a phone, and sign documents digitally – we are ready to deliver financial products on the phone and this is the disruption that is required. Access to credit drives the economy and with this new infrastructure, it is now possible to lend to the real India. However, it’s easy to give money, but the ability to get it back and keeping defaults at a minimum is the real trick. Even there we are moving towards seeing a radical improvement. Debt providers now have powers they never had and defaulters are being brought to book. Customers are now incentivized to build their own credit history to get better and lower interest rates over time. A new Public Credit Registry is coming to enable this at scale. But the biggest innovation is related to the dramatic shortening of the tenor. One can structure a one-year loan into 12 monthly loans or 52 weekly loans. This rewards positive customer behaviour and brings about the behaviour change that is needed.

There is no secret sauce here, it requires gumption – like that shown by Reed Hastings, founder of Netflix. He disrupted the TV and home video industry by first having the wisdom to go from ground to cloud and then again when they started developing original content. In both cases, he had little support from the board or investors. If you can reinvent yourself before it becomes necessary, you’re a winner but this is harder to do for a successful company. The legacy of success provides resisters with the clout to block change. The real beneficiary of Aadhaar based eKYC in the telecom world was not the incumbents but Jio – eKYC allowed Jio to acquire customers at an unprecedented scale and they saved INR 5000 crores on KYC costs as well.”

About iSPIRT

iSPIRT is a non-profit think tank that builds public goods for Indian product startup to thrive and grow. iSPIRT aims to do for Indian startups what DARPA or Stanford did in Silicon Valley. iSPIRT builds four types of public goods – technology building blocks (aka India stack), startup-friendly policies, market access programs like M&A Connect and Playbooks that codify scarce tacit knowledge for product entrepreneurs of India.

About AU Small Finance Bank:

AU Small Finance Bank Limited (AU Bank) started in 1996 as a vehicle financing NBFC, AU Financiers and scaled to touch over a million underbanked and unbanked customers across 11 states of North, West and Central India, prior to becoming a bank in April 2017. During this time, AU attracted equity investments from marquee investors such as IFC, Warburg Pincus, Chrys Capital, Kedaara Capital and recently went public when its IPO was oversubscribed ~54 times. Over the years, AU Bank, led by its founder Sanjay Agarwal, has created significant shareholder value with its equity value growing from ~$120 million in 2012 to current market capitalization of ~$3 billion.

Please Note: The blog was first published and authored by Matrix India Team and you can read the original post here: matrixpartners.in/blog

On behalf of iSPIRT, Sanjay Jain recently published an opinion piece regarding the recent supreme court judgement on the validity of Aadhaar. In there, we stated that section 57 had been struck down, but that should still allow some usage of Aadhaar by the private sector. iSPIRT received feedback that this reading may have been incorrect and that private sector usage would not be allowed, even on a voluntary basis. So, we dug deeper, and analyzed the judgement once again, this time trying to disprove Sanjay’s earlier statement. So, here is an update:

Section 57 of the Aadhaar act has NOT been struck down!

Given the length of the judgement, our first reading – much like everyone else’s was driven by the judge’s statement and confirmed by quickly parsing the lengthy judgement. But in this careful reanalysis, we reread the majority judgement at leisure and drilled down into the language of the operative parts around Section 57. Where ambiguities still remain, we relied on the discussions leading up to the operative conclusions. Further, to recheck our conclusions, we look at some of the other operative clauses not related to Section 57. We tested our inference against everything else that has been said and we looked for inconsistencies in our reasoning. Having done this, we are confident in our assertion that the judges did not mean to completely blockade the use of Aadhaar by private parties, but merely enforce better guardrails for the protection of user privacy. Let’s begin!

Revisiting Section 57

Here is the original text of section 57 of the Aadhaar Act

Nothing contained in this Act shall prevent the use of Aadhaar number for establishing the identity of an individual for any purposea purpose backed by law, whether by the State or any body corporate or person, pursuant to any law, for the time being in force, or any contract to this effect:

Provided that the use of Aadhaar number under this section shall be subject to the procedure and obligations under section 8 and Chapter VI.

Now, let us simply read through the operating part of the order with reference to Section 57, ie. on page 560. This is a part of paragraph 447 (4) (h). The judges broke this into 3 sections, and mandated changes:

‘for any purpose’ to be read down to a purpose backed by law.

‘any contract’ is not permissible.

‘any body corporate or person’ – this part is struck down.

Applying these changes to the section, we get:

Nothing contained in this Act shall prevent the use of Aadhaar number for establishing the identity of an individual for any purposea purpose backed by law, whether by the State or any body corporate or person, pursuant to any law, for the time being in force, or any contract to this effect:

Provided that the use of Aadhaar number under this section shall be subject to the procedure and obligations under section 8 and Chapter VI.

Cleaning this up, we get:

Nothing contained in this Act shall prevent the use of Aadhaar number for establishing the identity of an individual pursuant to any law, for the time being in force:

Provided that the use of Aadhaar number under this section shall be subject to the procedure and obligations under section 8 and Chapter VI.

It is our opinion that this judgement does not completely invalidate the use of Aadhaar by private players, but rather, specifically strikes down the use for “any purpose [..] by any body corporate or person [..] (under force of) any contract”. That is, it requires the use of Aadhaar be purpose-limited, legally-backed (to give user rights & protections over their data) and privacy-protecting. As an exercise, we took the most conservative interpretation – “all private use is struck down in any form whatsoever” – and reread the entire judgement to look for clues that support this conservative view.

Instead, we found that such an extreme view is inconsistent with multiple other statements made by the judges. As an example, earlier discussions of Section 57 in the order (paragraphs 355 to 367). The conclusion there – paragraph 367 states:

The respondents may be right in their explanation that it is only an enabling provision which entitles Aadhaar number holder to take the help of Aadhaar for the purpose of establishing his/her identity. If such a person voluntary wants to offer Aadhaar card as a proof of his/her identity, there may not be a problem.

Some pointed out that this is simply a discussion and not an operative clause of the judgement. But even in the operative clauses where the linking of Aadhaar numbers with bank accounts and telecom companies is discussed, no reference was made to Section 57 and the use of Aadhaar by private banks and telcos.

The court could have simply struck down the linking specifically because most banks and telcos are private companies. Instead, they applied their mind to the orders which directed the linking as mandatory. This further points to the idea that the court does not rule out the use of Aadhaar by private players, it simply provides stricter specifications on when and how to use it.

What private players should do today

In our previous post, we had advised private companies to relook at their use of Aadhaar, and ensure that they provide choice to all users, so that they can use an appropriate identity, and also build in better exception handling procedures for all kinds of failures (including biometric failures).

Now, in addition to our previous advice, we would like to expand the advice to ask that each company look at how their specific use case draws from the respective acts, rules, regulations and procedural guidelines to ensure that these meet the tests used by this judgement. That is, they contain adequate justification and sufficient protections for the privacy of their users.

For instance, banks have been using Aadhaar eKyc to open a bank account, Aadhaar authentication to allow operation of the bank accounts, and using the Aadhaar number as a payment address to receive DBT benefits. Each of these will have to be looked at how they derive from the RBI Act and the regulations that enable these use cases.

These reviews will benefit from the following paragraphs in the judgement.

The judgement confirmed that the data collected by Aadhaar is minimal and is required to establish one’s identity.

Paragraph 193 (and repeated in other paras):

Demographic information, both mandatory and optional, and photographs does not raise a reasonable expectation of privacy under Article 21 unless under special circumstances such as juveniles in conflict of law or a rape victim’s identity. Today, all global ID cards contain photographs for identification alongwith address, date of birth, gender etc. The demographic information is readily provided by individuals globally for disclosing identity while relating with others and while seeking benefits whether provided by government or by private entities, be it registration for citizenship, elections, passports, marriage or enrolment in educational institutions …

The judgement has a lot to say in terms of what the privacy tests should be, but we would like to highlight two of those paragraphs here.

Paragraph 260:

Before we proceed to analyse the respective submissions, it has also to be kept in mind that all matters pertaining to an individual do not qualify as being an inherent part of right to privacy. Only those matters over which there would be a reasonable expectation of privacy are protected by Article 21…

Paragraph 289:

‘Reasonable Expectation’ involves two aspects. First, the individual or individuals claiming a right to privacy must establish that their claim involves a concern about some harm likely to be inflicted upon them on account of the alleged act. This concern ‘should be real and not imaginary or speculative’. Secondly, ‘the concern should not be flimsy or trivial’. It should be a reasonable concern…