Over the past couple of days, a lot has been written/discussed about the so called ‘startup tax’ and its perceived ill effects on the startup ecosystem. Under iSPIRT’s new initiative, PolicyHacks, I attempt in this note to demystify the legal/tax jargon around this tax and to clarify the proposed rule for the benefit of ecosystem participants, particularly startups.

What is the law?

Simply put, if a private company issues shares to a resident Indian at a price above the fair market value (FMV) – say the FMV of a share is INR 100 and the company issues it at INR 110 – then the excess consideration (INR 10 in this case) is considered to be the company’s income (since, in a way, it deserved INR 100, but received INR 110). The amount of INR 10 is, therefore, liable to be taxed as the company’s income (which presently is at a rate of 30%). FMV is an important element here, and we will get back to it later. It is popularly called the ‘angel tax’.

Who are exempted from this?

As highlighted above, this provision is applicable only to investments received from resident Indians. Thus, at the first level, it does not affect foreign investments. In addition, the provision does not apply to investments made by SEBI-registered entities. One, therefore, need not worry about money received from angels/VCs/PEs which are either investing from foreign sources or have been registered with SEBI.

Who are hit by this?

Whoever is not covered under the above exemptions or otherwise exempted by the government. Prominently, the Indian angels (which constitute an overwhelming majority of the overall angel investors). Hence, the term ‘angel tax’.

What is ‘startup tax’ then?

As is clear from the above, the law is applicable to all private companies and does not single out startups. However, it has been reported in the media lately that startups which have raised down-rounds will be scrutinised by the tax department, and the valuations of such down-rounds will be considered to be the FMV of all previous (up) rounds.

In other words, if:

- in the last round:

- the valuation of the company was INR 1,10,00,000; and

- the FMV per share was INR 110;

- in the present (down) round:

- the valuation of the company is INR 1,00,00,000; and

- the FMV per share is INR 100,

then the valuation of the down-round, i.e., INR 100 will be considered to be the FMV of the previous round.

Hence, applying the law set out above, anything received by the company in excess of the FMV (in this case INR 10 per share) becomes its income, and is taxable as such.

So what is new in this?

Nothing. There is no change in the law. The issue that the industry has been facing since the introduction of this law is that the income-tax officers (who have wide ranging powers) were found to be using this provision to harass companies.

I have raised money from resident Indians and now I expect a down-round; will the tax department come after me?

Since this is not a new or proposed law, nothing stops the income-tax officer from going after any company even today. In fact, such proceedings have been initiated against quite a few companies in the past.

The key thing here to note is this – No tax can be levied on a company just because it has raised a down-round. The only money that this provision permits to tax is the consideration received by a company in excess of the FMV. It is a settled principle that each funding round can, and quite often, is raised at an FMV different than the previous round. So long as one can justify that in a down-round, the fall in FMV is on account of genuine external factors, and not because the FMV in the previous round was artificially inflated, one should be fine. Thus, even if one receives a notice from an income-tax officer in this respect, all one needs to demonstrate is that the FMV in the last round was calculated in accordance with the valuation mechanism provided under the IT Act, and there was no foul play in that respect. For startups falling in this category, there is nothing (or not much) to worry about, at least prima facie.

iSPIRT view and efforts

At iSPIRT, as part of the Stay-in-India initiative, we have been in continuous discussions with the government to rationalise this provision to ensure that genuine investments using legitimate money (such as angel investments) are not hit by this provision, and there is no unnecessary harassment.

Also, the government has exempted startups (which register on Startup India portal and are approved by the inter-ministerial board) from income-tax. Thus, ideally, such qualified startups should be exempt from this tax as well. We continue to discuss this with the government.

Author note and disclaimer: PolicyHacks, and publications thereunder, are intended to provide a very basic understanding of legal/policy issues that impact Software Product Industry and the startups in the eco-system. PolicyHacks, therefore, do not necessarily set out views of subject matter experts, and should under no circumstances be substituted for legal advice, which, of course, requires a detailed analysis of the relevant fact situation and applicable laws by experts in the subject matter on case to case basis.

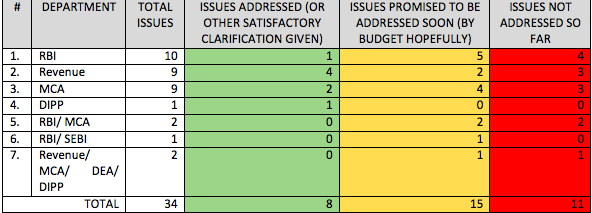

The policy changes announced by RBI are as follows:

The policy changes announced by RBI are as follows: Lastly, while the RBI has positively stated that it will notify certain changes soon, all of MCA issues and a majority of RBI issues are still at a ‘discussion/recommendation stage’ (and have been merely acknowledged by the authorities as issues that need to be resolved). Hopefully, the authorities will not stop here, and will implement all these changes soon. Needless to add, iSPIRT will keep interacting with, and assisting, the authorities in achieving a quick closure to these items, as well as the remaining issues which have not yet been touched by the authorities.

Lastly, while the RBI has positively stated that it will notify certain changes soon, all of MCA issues and a majority of RBI issues are still at a ‘discussion/recommendation stage’ (and have been merely acknowledged by the authorities as issues that need to be resolved). Hopefully, the authorities will not stop here, and will implement all these changes soon. Needless to add, iSPIRT will keep interacting with, and assisting, the authorities in achieving a quick closure to these items, as well as the remaining issues which have not yet been touched by the authorities.

What are some of the learning’s from this effort?

What are some of the learning’s from this effort?