Why Healthcare?

Interacting even briefly with the healthcare system reveals the issues that plague the sector in India: a severe shortage of high-quality doctors, nurses, or medical supplies (and a lack of information on where the best are); misdiagnoses or late diagnoses; overcrowding and long waits in public hospitals; overpriced and over-prescribed procedures and in private hospitals; a complicated insurance claim system; and significant gaps in health insurance coverage. Those who have worked on trying to improve the healthcare system know the systemic challenges: misaligned incentives in care delivery, a lack of health data to coordinate care, low state capacity, and the political battles between states and the Centre. Yet not one of us is spared bouts of illness or other health incidents over our lifetime. We have no choice but to work with this system. And when it doesn’t function effectively, the largest effects are felt by the poorest: productivity losses and income shocks caused by health issues have a way of spiralling individuals on the cusp of economic well being back into poverty.

Designing for high quality, affordable, and accessible healthcare in India is a challenging societal problem worth solving, with huge potential spillover benefits.

iSPIRT in Healthcare

At iSPIRT, we have started to develop an approach to dealing with complex societal problems at national scale. Our work on India Stack and financial inclusion taught us that public digital infrastructure can create a radical transformation in social outcomes when designed with a regulated and shared back-end that enables a number of (sometimes new!) private players to innovate on the front end to deliver better services. After all, innovative companies like Uber or Amazon are built on digital infrastructure: the TCP/IP Internet protocol and GPS systems that were both funded by public research. iSPIRT targets societal challenges by setting an ambitious target that forces us to think from first principles and innovate on the right digital public goods – which then catalyses a private ecosystem to help reach the last mile and solve the challenge at scale.

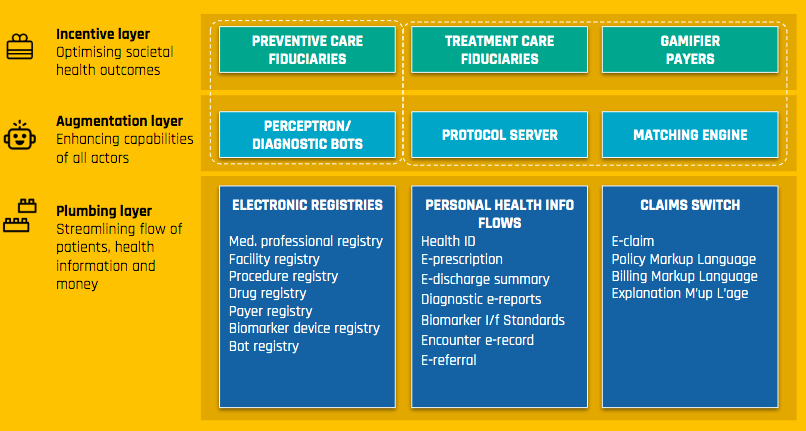

Over the last three years, members of our Health Stack team have been thinking deeply about how to design for a radical transformation in healthcare outcomes. We have developed a trusted working relationship with the National Health Authority and the Ministry of Health to better understand their operations and the issues at play. Our approach to addressing the challenge is evolving every day, but we’ve now developed a hypothesis around a set of building blocks that we believe will catalyse the health system. These blocks of digital infrastructure will, we hope, improve capacity at the edges of the system and realign institutional incentives to solve for long term holistic healthcare for all.

Some further teasers to our approach are included in the attached writeup which provides an overview of some of the more mature building blocks we hope to implement in the coming year.

We’re striving for an end state of healthcare that looks something like this (cut by population type on the left):

These ideas were presented by the team recently to Bill Gates in a closed-door meet last month (who said he was excited to see what we could accomplish!)

We need your help!

To help shape our ideas and make them a reality, we need more volunteers — particularly those with the following expertise:

- Technical Experts (e.g. microeconomists or engineers): We have a few building blocks with broad design principles that need fleshing out – for instance, a Matching Engine to between individuals and doctors/hospitals. If you are a microeconomist (especially if you have thought about bidding/auction design for a matching engine, and more generally want to solve for misaligned incentives in market structure) or you’re a techie interested in contributing to solve a problem at a national scale, please reach out! Prior expertise in healthcare is not a prerequisite. Also, if you’ve looked through the document and find a block where you think your technical expertise could help us build, certainly let us know.

- Current and Future HealthTech Entrepreneurs: Often, a successful health tech startup requires some public infrastructure to be successful. For instance, a powerful rating and recommendation app need a trusted electronic registry of doctors and hospitals providing core master data. Many of our Health Stack modules are designed to catalyse private sector participation and market potential for better products and services, which in turn produce better outcomes for individuals. If you are interested in helping design public infrastructure that your company could use or are a potential health tech entrepreneur interested in learning more about the ecosystem by building for it, please let us know!

- Healthcare Policy/Program Implementation Expertise: Field experience in healthcare delivery is invaluable – it gives us a true sense of the real challenges on the ground. If you’ve worked in delivering healthcare programs before with government, a non-profit, the private sector, an international organisation, or philanthropy and have ideas on what’s needed for an improvement in the sector at national scale, we’d love to hear from you.

- Market making/ Health Stack Evangelisation: Any technology is only as good as its adoption! As some building blocks of the health stack get implemented, we are looking for volunteers who can help evangelise and drive its adoption.

India’s potential in the health sector is tremendous – partly because we have an opportunity to redesign not just the technology foundation (which is a near-greenfield) but also the market structure. With the right team, we hope to orchestrate an orbit shift in the quality and affordability of healthcare across the country.

To volunteer, please reach out to [email protected] and [email protected]