iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

The volumes and traction on Open Credit Enablement Network (OCEN) continues to grow month on month. The growing trajectory highlights OCEN’s ability to streamline and democratise credit access for MSMEs by leveraging digital public infrastructure and fostering collaboration among lenders, agents, and technology providers.

Here is a snapshot of the OCEN ecosystem’s key updates for March:

Metric

Jan-25

Feb-25

Mar-25

No. of Lenders Live on OCEN

7

7

7

No. of Borrower Agents Live

6

6

6

No. of Technology Service Providers (TSPs) with active deployment

2

3

3

No. of Loan Products

11

11

11

No. of Loans Disbursed

895

1567

3179

Disbursement Amount

₹25.17 Crore

₹33.67 Crore

₹139.11 Crore

Average Loan Ticket Size

₹2.81 Lakh

₹2.14 Lakh

₹4.37 Lakh

As OCEN continues to evolve, it is poised to further bridge the credit gap for MSMEs, enabling faster, more transparent, and more inclusive financial support for this vital sector of the Indian economy.

India has made rapid progress in digitisation of the economy in the last decade becoming a world leader in identity systems, digital payments and tax, and a new data sharing and empowerment framework. However, many deep-rooted issues still exist, such as extending true financial inclusion; formalisation and creating a higher trust economy, that is essential for growth of mostly small businesses.

In this blog post, we look at innovations in blockchain, distributed ledger and other technologies such as zero-knowledge proofs as potential solutions to build a stronger fabric for the economy for decades ahead. The unique opportunity India has is to boost commerce by enhancing trust, thereby culminating the transformation already underway through existing building blocks of digital identity, payments and data sharing to boost commerce. Unlike many other countries, faster and interoperable payments or reducing the dominance of private money are solved problems for India; the missing piece is to digitise commercial contract enforcement, which on the other hand is a solved problem for developed countries. Lack of adequate contract enforcement caused by contracting parties having different versions of the truth; due to data systems that don’t interoperate reduces trust and creates friction for economic growth. Solution requires connecting the goods and services ledger to the money ledger, so that contracts of any kind become binding promises that can be executed programmatically. Using technology to solve this trust problem is a unique opportunity for India.

BADAL (also happens to be a word for Cloud in local language), a techno-legal solution in the form of “Distributed Ledger for Privacy-preserving Trustful Commerce; is proposed as an interoperable fabric underlying a future programmable economy across large and small businesses to create high trust economy.

We also look at the emergence of Central Bank Digital Currency (CBDC) which is one of the core money applications of this framework and global backdrop in Annexure. There are many other use cases being proposed from land records to decentralised clinical trials for blockchain and allied technologies in different areas of government and business1https://www.meity.gov.in/content/national-strategy-on-blockchain likewise, that can be implemented in BADAL.

First of all, why is trust important?

Trust is the basic glue that connects strangers and promotes economic activity. Money is the basic economic institution in a society building that trust2https://press.princeton.edu/books/paperback/9780691146461/the-company-of-strangers. However, trust builds slowly due to a combination of various factors such as the nature of institutions (political and legal) and the level of formalisation. While formalisation of even small businesses is increasingly addressed by the successful rollout of GST for India, formalisation of trust still remains elusive. At a core fundamental level, trust is a public good that creates friction-free commerce and is a recipe for rapid economic growth.

There is a high correlation between the level of trust in society and GDP per capita3https://ourworldindata.org/trust-and-gdp. A study conducted by World Value Survey attempted to measure the level of trust in a country by recording the positive responses received to the question ‘most people can be trusted’. It found that countries with high GDP per capita such as Sweden, Norway and Netherlands recorded high levels of trust exceeding 60% determined in this manner as the graphic below shows.

Douglass C. North, Nobel laureate in economics4https://www.nobelprize.org/prizes/economic-sciences/1993/north/lecture/, found that ‘the inability of societies to develop effective, low-cost enforcement of contracts is the most important source of both historical stagnation and contemporary underdevelopment.’ The Union Minister of Finance and Corporate Affairs has rightly acknowledged the role of the “Hand of Trust”5https://pib.gov.in/PressReleasePage.aspx?PRID=1601273when presenting the Economic Survey of 2019-20.

In societies like India, with limited ability to efficiently enforce routine civil or property contracts, businesses tend to restrict working with those similar to them based on caste, religion etc. (called associational activity) where there is an implicit social and moral enforcement mechanism or with members who have clearly demonstrated reputation in the past (usually the large or the older players). In both these situations, the economic benefit that a new firm can bring with new ideas or new techniques will be muted as its absorption is slower. Similarly, a new player will find it very difficult to compete with incumbents even if such players are economically more efficient. Economist Olson6Olson, M. (1974). The logic of collective action. Harvard University Press showed that associational activity is often more detrimental than favourable for an emerging economy. So we need better ways to break this trust logjam. Trust in the money system in India is comparatively high, as promises tend to be kept with sufficient legal backing and can be digitised with e-mandates or automated payments/ collections; but the same is not the case for goods (or services) ledger, leaving room for delays cascading into a logjam resulting in low trust. This is often felt in day to day life by citizens not getting routine services despite advance payment or small businesses not getting paid despite having supplied goods. Delays, defaults and disputes can become the norm if parties have different versions of the truth.

Every economic activity is thus like a mini-contract with one side on the money ledger (payment from party A to B) and the other side, on the goods/services ledger (from B to A) between counterparties, and can be converted into an electronic contract that automatically executes on both ledgers subject to interoperability. To assure the performance of contracts, the money ledger and the goods/ services ledger need to be connected in a way that is scalable, privacy-enhancing, non-repudiable and programmable. This enables a contract agreed between parties becomes a commitment, and fulfilment is guaranteed by code through the electronic contract. Assuring performance of contracts is critical for a country that is seeking to grow through startup activity, not just in tech but other sectors too.

Currently, litigants lose nearly ₹ 50,000 crores annually in wages or business lost which comes to 0.5% of the country’s GDP, because of litigation, an indication of how expensive litigation can be. The majority of civil disputes in courts are related to recovery of money (30.2 per cent) and land-or property-related matters (29.3 per cent) As reported in the 2016 survey carried out by DAKSH. Common reasons for dispute are different versions of the truth of contracting parties, prior to contract (past) or during the performance of contract (future). Having the same truth and programmability inherent in electronic contracts is a boon in this regard.

In an earlier blog, we have explored the benefits of adapted blockchain technologies to solve the problem of SME financing in India with a related post by global experts7https://balajis.com/add-crypto-to-indiastack/. We build further on that and believe that India can harness recent advances associated with blockchain technology to enable trust between unrelated parties by combining the best of the scalable and centralized legacy world with a secure and private decentralized world. This can benefit the real economy vastly along with the financial world.

Innovations in distributed ledger technologies and BADAL

Distributed Ledger technology can help in two ways – first by being able to verify past performance before one party strikes a deal with another, and second, by being able to enforce a contract in most situations as performance unfolds in future. Thus, building trust about the past as well as the future.

We thus imagine a fabric based on the following basic principles to help create and grow a large number of applications to record economic activity even while reconciling with other activities and past data and help inject a level of trust by creating a reliable, immutable record of trusted data records and programmable contracts

Single platform to allow standards bodies and organisations to publish their schemas, and reuse other schema elements in composing workflows

Fully privacy-preserving capabilities to allow participants to publish relevant zero-knowledge proofs which do not require private data to be shared beyond the participating entities

A programmatic contracts capability that can help automatically carry out the relevant tasks as agreed on without any further manual intervention

By connecting a new digital money ledger (such as Central Bank Digital Currency, or stablecoins) with the new goods & services ledger, we envisage a boost to trust across economy and commerce. As such, BADAL is the first such framework we are aware of globally, uniquely suited to India’s needs, opportunities and strengths.

We have discussed the early version of this in detail in an earlier open-source document8https://github.com/iSPIRT/ppl, called Public Private Ledger. BADAL is thus a privacy supporting, trust enhancing mechanism of coordinating economic activity, and information recording and sharing. Originally this group started out of a process to explore the domain around and figure out the appropriate model to support CBDC, support data sharing between participants, and coordination and automation of event-based standing instructions across events in the goods and services ecosystem and/or money flow.

We then reviewed exciting developments in related areas first to understand their relevance given India’s unique needs. Blockchain technologies generally are seen to enable unrelated parties to trust each other and transact without depending on a central institution or intermediary. These technology innovations are around three key areas:

Maintaining immutability and integrity of data across the distributed ledgers of parties.

Governance mechanisms, especially for decentralised networks

The programmability of such transactions to allow automatic execution.

Public blockchain technologies like Bitcoin and Ethereum, on the other hand, are based on a philosophy of distrust of centralised institutions like Central Banks and are designed for unrestricted access and decentralised decision-making. But they have had to develop new approaches to contend with a few challenges, especially given the huge growth off late that see further wor:

The enormous consumption of resources to establish ‘proof of work’ that limits efficiency and scalability, leading to newer approaches

Exposing all transactions on these networks that generally do not allow sensitive data to be private on the key layer, is as critical for confidential business data as it is for personal data

Rise of many networks that are not interoperable with each other or with the mainstream economy, though some bridges do exist

May have ability to operate outside banking conduits and regulatory frameworks that challenges government’s sovereignty and financial stability through greater oversight has been coming recently

Research on amending throughput, reducing costs and enhancing privacy/auditability/KYC compliance has been ongoing at a rapid pace, especially over the last couple of years.

Despite these unresolved issues, Public blockchain-based tokens, so-called cryptocurrencies, NFTs etc have become an unregulated asset class, especially amongst the young rapidly given the ease of use, creating concerns on possible misuse as well as potential opportunities. We were also part of the recent consultation of the Parliamentary Committee on Finance on ‘Cryptoassets: Opportunities and Challenges’ and had shared with them some of our ideas above in our submission here9https://docs.google.com/document/d/e/2PACX-1vShkuTno_bSILFZPf-Cb_KNwwgM6A_6OgyRiASNS0tXB3ViriHztovrkL7sebiAC7O54y0uwQheTdin/pub.

Various solutions have been employed to address some of these challenges:

Permissioned blockchains, such as Hyperledger Fabric and Corda, allow only trusted parties to participate. Corda uses Notaries for verifying transactions. Such solutions have been successfully used in finance, supply chain, property rights, healthcare, education and e-governance

Zero-knowledge Proofs (ZKPs) allow proving/verification of specific aspects of data without actually making the data public

BADAL builds on the above primitives and is offered as an open and interoperable platform to enable money ledgers such as CBDC/stablecoin along with applications relevant for finance and commerce. This can be designed as a permissioned network relying upon a few regulated entities, and interoperable to ensure that its benefits are widespread and at much lower costs than permissionless systems. It consists of a private ledger that holds sensitive user data withaccess restricted to participating entities only, and a public ledger that contains notarised zero-knowledge proofs about transactions between users. It supports different schemas (configurations) that enable usage across different use-cases.

This programmability coupled with immutability akin to electronic contracts, allows applications in BADAL to be used to leapfrog the trust logjam, without diluting sovereign privileges of control of money given India’s stage of development. BADAL will thus establish provenance that helps establish credibility and reputation of transacting parties, proof of title/ownership of goods and assets, proof of the history of transactions including promises made and ambiguously defined and fulfilled; automatic execution of terms of contracts along with privacy as a fundamental right.

Historically, monetary accounting has solved for only one side of this metaphorical coin- the monetary value. All monetary systems denote a money value to any transfer of goods or services. BADAL, being a ledger that can record value in any domain, solves for the non-monetary aspect of the transaction. Integrated with electronic contracts for a variety of applications, BADAL will enable digital claims on non-monetary assets, including new age asset classes such as crypto assets, NFTs, where claims can be financialized and liquidated. An inherent promissory layer can be enabled into the current transaction mechanism. This extends to all data types, from land records to hospital quality service quality etc, rather than just transactions involving money and goods/ services.

The ability to connect any of the data types across domains can give rise to massive amount of efficiency gains with automated execution thanks to new data from machines like cars, consumer durables like refrigerators or health wearables coming from advances in IoT (Internet of Things), 5G, Imagine a use case of automated crop insurance with sensors that monitor weather from a satellite in space to moisture in soil etc. and deliver claim benefit to the farmer with zero friction in real-time.

One of the biggest problems BADAL could solve at bottom of the pyramid is financial inclusion in India. This is not only in the form of increased monetary transactions through it, but also the ability for MSME’s to gain cheaper credit. This is a possibility as MSME’s will find it easier to prove their liquidity and income to banks and other lenders due to the monetary traceability the system will provide. An increased ability to prove financial stability will lead to greater leverage for borrowers and more systemic trust for lenders. This increase in the systemic trust will not only lead to an increase in credit creation but catalyse an increase in money velocity in India as a whole.

In a subsequent blog post, we will detail the potential use cases; as well as preliminary design of a prototype of one sample use case that is being built currently.

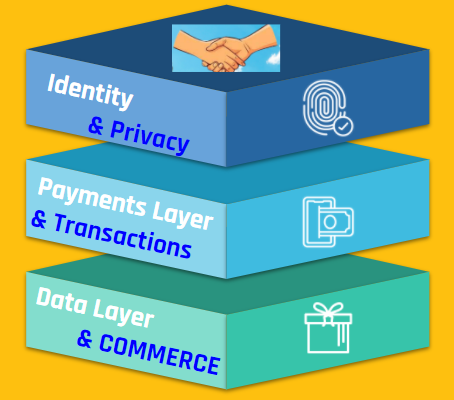

BADAL fabric supporting India Stack could boost digital India

India has pioneered transformations in Identity, Payments, and Data empowerment (these building blocks are popularly called the India Stack) through a techno-legal approach. These address friction of doing business, information asymmetry, and distributed systems. Breakthroughs along the way were public platform (identity), public protocols and standards, and techno-legal approaches to solving big societal problems.

The recent launch of the Account Aggregator (AA) model (based on Data Empowerment and Protection Architecture, DEPA) allows the controlled sharing of private financial data by citizens with various financial institutions to get the best deals. This is a global first and in some sense, an export of a truly global standard12https://twitter.com/Product_nation/status/1435997280692158464?s=20 from India.

Open Credit Enablement Network (OCEN) is creating a way to democratise access to credit, to the level of making it accessible to a street vendor for small sums. These public goods prevent any large player from monopolising the data ecosystem and at the same time reduce the cost of providing service. For instance, microloans as small as Rs.300 can be availed on GeM-SAHAY leading to true inclusion at the bottom of the pyramid.

These techno-regulatory concepts are now being considered for adoption by several countries across the world. Overall, India is arguably ahead of most countries in adopting technology for promoting financial inclusion as well13https://www.bis.org/publ/bppdf/bispap106.pdf.

Image Courtesy: Ananya Phadke

The next building block now is the trust layer through BADAL, ensuring every commitment is met and every contract is enforceable, boosting transparency and growth over the next decade. Trust permeates through all three ends of this triangle as identity is the ‘who’; and data and payment relate to ‘what’ of commerce. In BADAL, identity and data sharing can be achieved without diluting privacy to enable trusted payments (& commerce).

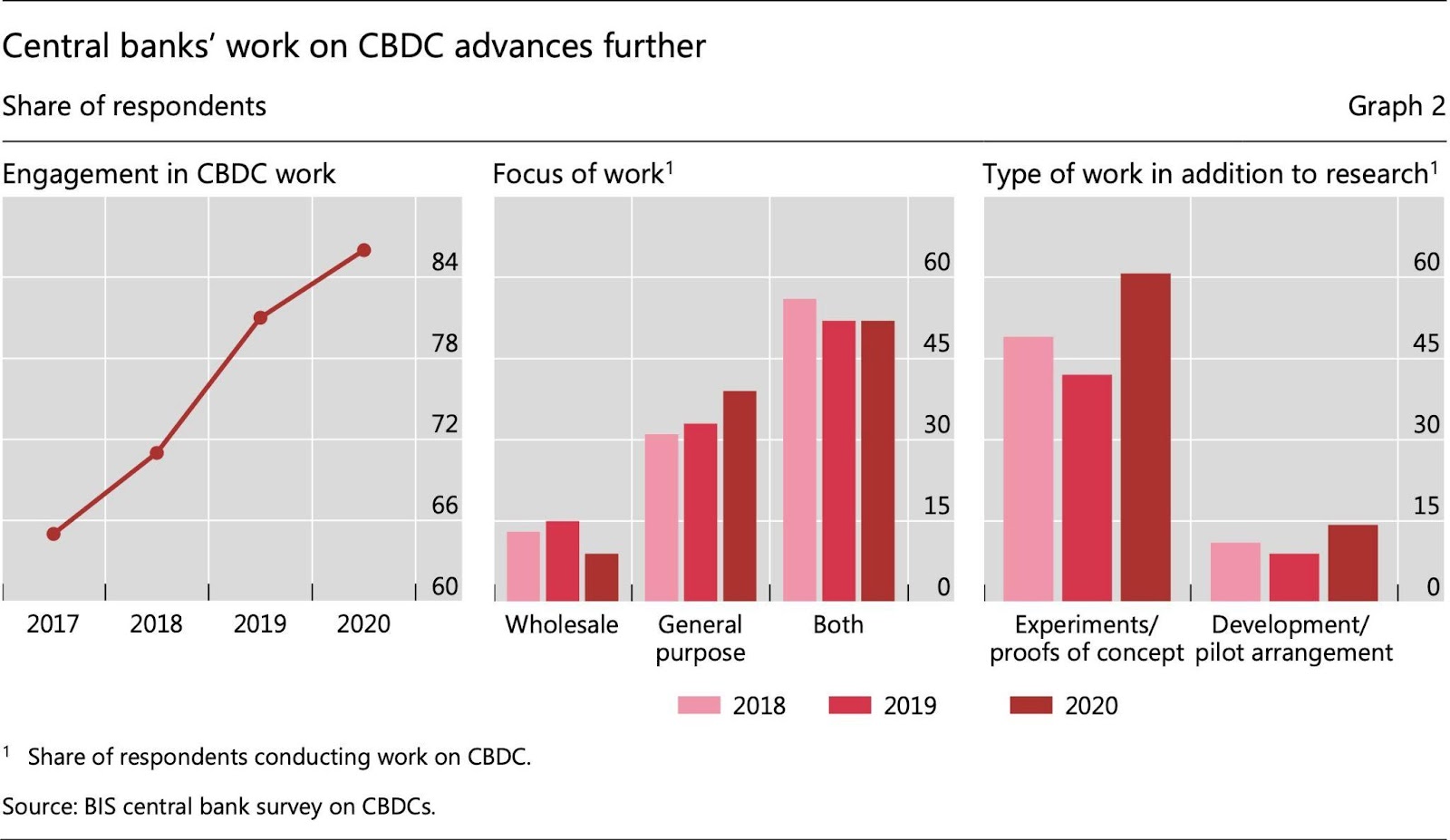

Annexure: CBDC Developments

While BADAL provides fabric to money or goods ledgers, we describe CBDC in detail here, given its importance. Money was traditionally issued by the sovereign (through a Central Banker) and circulated in the economy through layers of banking intermediaries. With the advent of permissionless public blockchains, some of which also seek to portray themselves as alternate currencies, the sovereigns have taken note and introduced their own variant as a public good to protect the financial stability of the nation-states. This sovereign/state-issued digital currency is popularly known as Central Bank Digital Currency (CBDC).

While there are different types of CBDCs such as wholesale/ retail and account-based/ token-based, ultimately a payment using CBDC can be immediately settled. This is akin to using paper money and unlike a cheque or money transfer between bank accounts that require a process of clearing and settlement adding to inefficiency and costs. CBDC can potentially thus leapfrog depending upon the development of existing banking systems in different countries.

Advanced Economies (AEs) and Emerging Markets and Developing Economies (EMDEs) have different motivations for issuing CBDC to end-users (via Retail CBDC) and financial institutions (via Wholesale CBDC), illustrated in the diagram below.

In the USA, payments are expensive due to its legacy system of banking. This has led to a burst of digital payment options, the latest being ‘stablecoin assets’ (digital currencies backed by real assets like US dollar, treasuries, etc) that also compete with their money-market funds. Stablecoin assets have crossed $100 billion25https://www.statista.com/statistics/1255835/stablecoin-market-capitalization/ in market value and are a popular choice to transact in Decentralised Finance (DeFI). DeFi is a parallel financial system evolving around crypto-assets. DeFI is not subject to transparency and compliance required in the conventional financial world at this point in time. As DeFi becomes big and interacts with the conventional financial world, there is a growing systemic risk arising from failure or fraud in DeFi. The US Government, therefore, wants to regulate some aspects of DeFI26https://www.federalreserve.gov/monetarypolicy/fomcminutes20210728.htm and may thereby bless some stablecoins and crypto-assets as explicitly permitted financial products. Earlier in 2015, Bitcoin was determined to be a commodity27https://www.cftc.gov/sites/default/files/2019-12/oceo_bitcoinbasics0218.pdf by some authorities there. The US Fed has also begun a consultation process towards design choices and feasibility of CBDC implementation.

Indian perspective

In India, the focus of policy has rightly been on promoting financial inclusion to formalise the economy and drive economic growth. One important factor which drives the usage of unregulated informal value transfer systems is the lack of banking facilities and corresponding amenities for managing money, which leaves rural communities without alternatives other than a person-to-person method of transferring monetary value. Even though India has seen a significant increase in the number of bank accounts created, Reserve bank data still highlights little improvement in account usage and institutional borrowings, which feeds into the broader issue of financial inclusivity.

Initiatives like Pradhan Mantri Jan-Dhan Yojana (PMJDY) opened doors to big change. UPI has been very successful as a payment mode but still needs underlying bank accounts to transact and thus depends on the banking system & its motivation to provide access to the poor. The PMJDY scheme announced in 2014 has increased the number of adults with bank accounts to 43.47cr 28Progress Report as on 22-Sep-21, PMJDY, MOF, GOI, https://pmjdy.gov.in/account (~46% of 93.55cr adults with an Aadhaar29https://uidai.gov.in/images/Saturation_Report_State-UT_Agewise_31-08-2021.pdf). Despite this headway, there is still a lot to be achieved. The Financial Inclusion Index (FI) recently launched by RBI shows that India is at 53.9 on March 21 (vs 43.4 in March 2017) – a little more than halfway towards complete financial inclusion (FI of 100)30https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52068. Presently, the banking system acts as the main gateway to financial inclusion as the banking system is the main distributor of cash. Hence, various government programmes (like PMJDY) rely upon banks for financial inclusion, despite those being not remunerative for banks. The accounts also have various restrictions on the number of debits/withdrawals to ensure low cost.

Even with the existence of such low-cost bank accounts, the poor do not have an incentive to use a bank account regularly as they do not save enough to use the bank account as a store of value. They use these accounts mainly to collect remittances and withdraw cash at ATMs as bulk of their transactions is in cash, not leaving a visible money trail that in turn makes financial inclusion difficult. Cash in circulation in India even now is Rs 29.38 trillion31https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52274 (~14.9% of estimated GDP for 2020-2132http://mospi.nic.in/sites/default/files/press_releases_statements/Statement_12_1st+September+2021.xls) despite the availability of these cheaper accounts, demonetisation in 2017 and the subsequent formalisation of the economy with GST, RERA, etc.

In addition, the cost of handling cash by the central bank and commercial banks (currency printing, operating currency chests, logistics of moving currency, ATM operations, etc.) has been estimated to be ~Rs 21,000 cr (Rama Bijapurkar) and ~1.7% of GDP ( (Visa Inc., 2016). High adoption of CBDC can help in reducing this cost while creating enormous amounts of data and enabling policymakers to diagnose and regulate better. At a later stage, CBDC can also be used for targeted monetary policy actions when its impact on the financial system is well understood. Experts are concerned that CBDC may result in the disintermediation of the financial system. This risk can be mitigated by following design principles set out by the Bank for International Settlements (BIS)33https://www.bis.org/press/p201009.htm (i) “do no harm” to monetary and financial stability; (ii) coexist with cash and other types of money in a flexible and innovative payment ecosystem; and (iii) promote broader innovation and efficiency.

CBDC inherently provides an alternative to cash to directly reach a customer and can complement the banking network to make adoption quicker. By providing a digital alternative to cash will enable building verifiable money trails that can lead to greater financial inclusion by private players providing customised health, insurance, investment & education products in compliance with privacy laws. In the financially excluded segments, CBDC, being a form of central bank currency, is likely to be well trusted and be adopted easily.

The blog post is co-authored by Sanjay Phadke, Dhananjay Nene, Sharad Sharma, Navin Kabra, R Barve, K Babel, V Agarwal, K Gokarn, Kalyan Narguru, Shashank B, Arun Maharajan, Karan Sirdesai, P Sahu, P Rao, A Kulkarni, Krishna Iyer, V Nene and A Lath.

If you have any queries or comments, please contact us at [email protected].

The internet connected the average Indian to millions of sources of information. Could crypto protocols connect Indians to millions of sources of capital?

To achieve its goal of a five trillion dollar economy by 2025, India needs to close an enormous financing gap for its small and medium-size enterprises (SMEs). It already has important assets with which to attract global capital: the youth of its population, the energy of its tech sector, the growth of its internet connectivity, and the rising acceptance of so-called informational collateral in lieu of traditional physical collateral. But what hasn’t yet been done is to integrate these assets into the new multi-trillion dollar cryptoeconomy, which may have the most risk-tolerant, internationally oriented, growth-seeking pool of investors in the world.

In this piece we begin by reviewing India’s need for SME and startup capital. We then tick through India’s existing assets, with particular focus on informational collateral, which combines the previously separate concepts of due diligence and physical collateral into an internet-friendly financing package. Finally, we discuss why global crypto investors could help meet India’s capital needs.

India’s need for SME and startup financing

India is home to more than 60 million businesses, 10 million of which have unique GST registration numbers, most of them SMEs. However, of the one trillion USD worth of total commercial lending exposure of the banking system, only ~25% of it is provided to SMEs, which are considered less creditworthy than larger corporates or multinationals. This has resulted in a financing gap estimated to be between 250-500 billion USD, where meritorious businesses without national profiles aren’t able to access the capital they need to finance their growth. India’s next trillion in GDP growth depends upon solving this problem, but the incumbent financial system may not have the resources to fix it alone. Despite ever-increasing bank branches, India’s legacy financial system is still slow, costly, and unwieldy for borrowers— in sharp contrast to the databases, online KYC systems and intelligent lending apps of new-age fintech companies. And in addition to this high cost of capital for MSMEs, India also has a low baseline level of financial inclusion.

The baseline issue is being partially addressed with low-frill Jan Dhan accounts, which are providing partial banking support for millions of previously excluded individuals. Many of these Jan Dhan accounts are held by small businesses, entrepreneurs, students and self-employed people in rural India, the same folks who are running India’s SMEs. But these accounts have only inflow data, with outflows typically in cash. Even though cash still plays a big role in the self-organized and informal sectors, it’s not easy to provide business-related financing in cash. The so-called JAM trinity (Jan Dhan accounts, Aadhaar digital identities, and Mobile phones) offers a partial solution for this under-banked population, but it only supports what we might think of as consumer-grade applications like basic peer-to-peer payments and individual savings accounts. Access to capital sufficient to finance a business — a true measure of financial inclusion — is still not yet present for these low-income, mostly feature-phone possessing groups.

On the other end of the spectrum from rural SMEs are India’s tech startups. Over the last decade, India has broken into the ranks of global technology and is now the #3 generator of unicorns in the world. Supportive governmental policies, combined with a young, creative, and aspirational workforce has helped reimagine large swathes of the economy including diverse industries such as e-commerce, logistics, SAAS, education, food, healthcare etc. This rise has attracted global equity and loan-funds that could in turn help many start-ups become world beating players in their respective domains. But the startup sector is just as hungry for capital as the rural SMEs, and India’s startup economy is still somewhat disconnected from global venture capitalists and financial markets.

India’s assets: youth, growth, connectivity, and informational collateral

India does have assets with which to close the capital gap. It has a youthful population. It has a fast-growing economy, even given the setbacks of COVID-19. It has an enormous population of hundreds of millions of new internet users. And it has something new, which is the possibility of informational collateral as a sort of combination of traditional concepts of due diligence and physical collateral.

Specifically, the SME funding gap is most pressing for the Indian cash-flow businesses that don’t have the physical assets to take out loans, which are the mainstay of the current, hard-collateral-backed credit system.

One alternative is to use trustworthy digital records to ascertain whether a business is worthy of credit or equity investment. India’s Goods and Services Tax (GST) helps to address this by generating invoice and payment data in a format suitable for credit underwriting and risk analysis. The GST data also enables a small enterprise in a large value system to provide data and visibility across the supply chain; for example, one can track the progress of parts from a small parts supplier to an auto component manufacturer to a large passenger car maker all the way through to distributors, sub-dealers, and retail sales.

The digital version of an SME’s sales and purchase invoices ledger thus amounts to informational collateral on both the company and the larger ecosystem within which it sits, that could become the basis for extending credit, as an alternative to the hard asset or collateral-based financial system. This is similar to how Square Capital and Stripe Capital already function in the West.

In addition to credit-based financing, the trustworthy records furnished by GST’s informational collateral can also support equity or quasi-equity financing, to support growth without increasing debt. These might take the form of direct equity investments in small businesses, or even personal micro-equity investments in individual consultants or students.

India’s innovation: use new pools of crypto capital to address long-standing financing needs

So, we understand that (a) Indian SMEs need capital, and that (b) IndiaStack’s UPI and Aadhaar can help GST generate informational collateral for potential investors and lenders.

Now the question arises: what class of investors is most willing to use this newfangled type of informational collateral to invest in potentially high-risk businesses outside of the proven venues of America, Europe, East Asia and the large Indian enterprises? Who are the most risk-tolerant, international, forward-looking, class of investors in the world — willing to risk millions of dollars purely on the basis of internet diligence alone?

It may turn out to be the new class of wealthy, globally-minded crypto investors. After all, the 10-year old cryptoeconomy is now worth trillions of dollars, there are more than a hundred million crypto holders around the world, and there are at least fifty crypto protocols valued over one billion dollars, a “unicoin” analog to the traditional tech unicorn. While still small in comparison to global capital markets, a sector worth $2T that is growing at more than 100% per annum could become a much larger piece of the global financial puzzle in short order. This is a new source of risk-tolerant digital capital that could flow into India to help close the SME financing gap, if we can make it an attractive proposition for the global investor.

Specifically, India could offer a viable path to deploy this new crypto wealth in a controlled manner, while solving for SME financial inclusion. Inflows of cryptocurrencies from KYC-ed investors through approved Indian and global exchanges can potentially be allowed into India for the purposes of enhancing SME access to low-cost global capital. GST-registered companies could, for instance, receive capital against their issued e-invoices and other information collateral in special accounts opened via a controlled conduit such as GIFT city, which is one of India’s favored bridges to international markets. The companies benefiting will need to explicitly consent to sharing their information and receiving funds into a new account at system-level while capturing cash flows against invoices for repayment. Inflows of global crypto-capital into Indian SMEs could also enable the rest of the credit system to migrate to informational collateral-based lending. And the special account could eventually be ported to a wallet backed by a national digital currency, such as the proposed digital rupee.

For more detail on this possibility, we invite your attention to Balaji S. Srinivasan’s companion piece on the subject, where he proposes to Add Crypto To IndiaStack. Balaji makes the case for crypto-powered extension of IndiaStack, which broadens IndiaStack from its current mostly domestic remit into an international platform for attracting capital from around the world. He describes several case studies by which the emerging world of decentralized finance or “defi” could help enrich the Indian economy, without competing with the digital rupee. For example, Indian startups could benefit from crypto crowdfunding, Indian SMEs as discussed could access global defi lending pools, and Indian students might even be funded with the emerging concept of personal tokens, like an equity-based version of microfinance. As the former CTO of Coinbase, the $100B crypto goliath, and a former General Partner at Andreessen Horowitz, the $16B venture capital firm, Balaji’s proposals have technical and social support from the very class of investors we’d seek to attract. At least insofar as they relate to the issue of plugging the SME financing gap, we believe they deserve serious consideration by policymakers in India.

In short, India has a unique opportunity to close the SME financing gap by attracting the new class of global crypto investors, by using everything the IndiaStack team has helped build over the last decade — particularly UPI, Aadhaar, GST, and the informational collateral they generate — to help connect the trillion-dollar cryptoeconomy to capital-hungry Indian entrepreneurs.

In 1973, the British economist Ernst Schumacher wrote his manifesto “Small is Beautiful”, and changed the world. Schumacher’s prescription — to use technologies that were less resource-intensive, capable of generating employment, and “appropriate” to local circumstances — appealed to a Western audience that worried about feverish consumption by the ‘boomer’ generation. Silicon Valley soon seized the moment, presenting modern-day, personal computing as an alternative to the tyranny of IBM’s Big Machine. Meanwhile, in India too, the government asked citizens to embrace technologies suited to the country’s socio-economic life. Both had ulterior motives: the miniaturisation of computing was inevitable given revolutions in semiconductor technology during the sixties and seventies, and entrepreneurs in Silicon Valley expertly harvested the anti-IBM mood to offer themselves as messiahs. The government in New Delhi too was struggling to mass-produce machines, and starved of funds, so asking Indians to “make do” with appropriate technology was as much a political message as it was a nod to environmentalism.

And thus, India turned its attention to mechanising bullock carts, producing fuel from bio-waste, trapping solar energy for micro-applications, and encouraging the use of hand pumps. These were, in many respects, India’s first “civic”, or socially relevant technologies.

The “appropriate technology” movement in India had two unfortunate consequences. The first has been a celebration of jugaad, or frugal innovation. Over decades, Indian universities, businesses and inventors have pursued low-cost technologies that are clearly not scaleable but valued culturally by peers and social networks. (Sample the press coverage every year of IIT students who build ‘sustainable’ but limited-use technologies, that generate fuel from plastic or trap solar energy for irrigation pumps.) Second, the “small is beautiful” philosophy also coloured our view of “civic technologies” as those that only mobilise the citizenry, out into farms or factory floors. Whether they took the form of a hand pump, solar stove or bullock cart, these technologies did little to augment the productivity of an individual. However, they preserved the larger status quo and did not disrupt social or industrial relations as technological revolutions have historically done.

Nevertheless, there has always been a latent demand in India for technologies that don’t just mobilise individuals but also act as “playgrounds”, creating and connecting livelihoods. When management guru Peter Drucker visited post-Emergency India in 1979, Prime Minister Morarji Desai sold him hard on “appropriate technology”. India, Drucker wrote, had switched overnight from championing big steel plants to small bullock carts. Steel created no new jobs outside the factory, and small technologies did not improve livelihoods. Instead, he argued, India ought to look at the automotive industry as an “efficient multiplier” of livelihoods: beyond the manufacturing plant, automobiles would create new sectors altogether in road building and maintenance, traffic control, dealerships, service stations and repair. Drucker also pointed to the transistor as another such technology. Above all, transistors and automobiles connected Indians to one another through information and travel. Drucker noted during his visit that the motor scooter and radio transistor were in great demand in even far-flung corners, a claim that is borne by statistics. These, then were the civic technologies that mattered, ones that created playgrounds in which many could forge their livelihoods.

The lionisation of jugaad is an attitudinal problem, and may not change immediately. But the task of creating a new generation of civic technologies that act as playgrounds can be addressed more readily. In fact, it is precisely during crises such as the ongoing COVID-19 pandemic that India acutely requires such platforms.

Consider the post-lockdown task of economic reconstruction in India, which requires targeted policy interventions. Currently, the Indian government is blinkered to address only two categories of actors who need economic assistance: large corporations with their bottom lines at risk, and at the micro-level, individuals whose stand to lose livelihoods. India’s banks will bail out Big Business, while government agencies will train their digital public goods — Aadhaar, UPI, eKYC etc — to offer financial assistance to individuals. This formulaic approach misses out the vast category of SMEs who employ millions, account for nearly 40% of India’s exports, pull in informal businesses into the supply chain and provide critical products to the big industries.

To be sure, the data to identify SMEs (Income Tax Returns/ GSTN/ PAN) exists, as do the digital infrastructure to effect payments and micro-loans. The funds would come not only from government coffers but also through philanthropic efforts that have gained steam in the wake of the pandemic. However, the “playground” needs to be created — a single digital platform that can provide loans, grants or subsidies to SMEs based on specific needs, whether for salaries, utilities or other loan payments. A front-end application would provide any government official information about schemes applied for, and funds disbursed to a given SME.

Civic technologies in India have long been understood to mean small-scale technologies. This is a legacy of history and politics, which policymakers have to reckon with. The civic value of technology does not lie in the extent to which it is localised, but its ability to reach the most vulnerable sections of a stratified society like India’s. The Indian government, no matter how expansive its administrative machinery is, cannot do this on its own. It has to create “playgrounds” — involving banks, cooperative societies, regulators, software developers, startups, data fiduciaries and underwriting modellers — if it intends to make digital technologies meaningful and socially relevant.

About the author: Arun Mohan Sukumar is a PhD candidate at the Fletcher School, Tufts University, and a volunteer with the non-profit think-tank, iSPIRT. He is currently based in San Francisco. His book, Midnight’s Machines: A Political History of Technology in India, was published by Penguin Random House in 2019

Amidst the usual flurry of sensational headlines, you may have missed a quiet announcement a few weeks ago that marked a monumental shift: RBI became the first central bank globally to publish acommon technology framework – including detailed APIs – for consent driven data sharing across the entire financial sector (banking, insurance, securities, and investment).

This is a gamechanger for the industry.

Out of context, yet another circular with a good deal of jargon is an easy thing to gloss over. But it turns out this effort is actually a global first: although the UK, EU, Bank of International Settlements (BIS), Canada, and others have begun thoughtful public conversations around Open Banking (e.g. through that famous BIS report making the case, initiatives like PSD2, conferences, and various committees), India is one of the first nations in the world to actually make it a market reality by publishing detailed technical API standards — standards that are quickly being adopted by major banks and others across the financial sector in the country without a mandatory requirement from RBI. It’s not just the supposedly cutting edge banks of Switzerland, the UK, or the US driving fintech innovation: the top leadership of our very own SBI, ICICI, IDFC First, Bajaj Finserv, Kotak, Axis, and other household names have recognised that this is the way forward for the industry, and are breaking through new global frontiers by actually operationalising the powerful interoperable technology framework. Not only are they adopting the APIs, some are also starting to think through the new lending and advisory use cases and products made possible by the infrastructure. We think many new fintech startups should also be considering doing the same.

Why do the APIs Matter?

The world is focusing heavily on data protection and privacy – and rightly so. Securing data with appropriate access controls and preventing unauthorised third-party sharing is critical to protecting individual privacy. But to a typical MSME, portability and control oftheirdata is just as critical as data security to empower them with access to a stream of new and tailored financial products and services. For instance, if an MSME owner could share trusted proof of their business’ regular historic GST payments or receivables invoices digitally with ease, a bank could now offer regular small ticket working capital loans based on demonstrated ability to repay (known as Flow-based lending) rather than just loans backed on collateral. Data sharing can become a tool for individual empowerment and prosperity by enabling many such innovative new solutions.

Operationalising a seamless and secure means to share data across different types of financial institutions – banks, NBFCs, mutual funds, insurance companies, or brokers – requires a common technology framework for data sharing. The published APIs create interoperable public infrastructure (a standard ‘rails’) to be used for consented data sharing across all types of financial institutions. This means that once a bank plugs into the network as an information provider, entities with new use cases can plug in as users of that data without individually integrating with each bank. Naturally, the system is designed such that data sharing occurs only with the data owner’s consent — to ensure that data is used primarily to empower the individual or small business. The MeiTY Consent Framework provides a machine-readable standard for obtaining consent to share data. This consent standard is based on an open standard, revocable, granular (referring to a specific set of data), auditable, and secure. Programmable consent of this form is the natural next innovation of the long terms and conditions legalese that apps typically rely on. RBI has also announced a new type of NBFC – the Account Aggregator – to serve as a consent dashboard for users, and seven new AAs already have in principle licenses.

The Data Empowerment and Protection Architecture (DEPA) – in one image

In many other nations, market players have either not been able to come together to agree on a common technical standard for APIs, or have not been able to kick off its adoption across multiple competing banks at scale and speed. In countries like the US, data sharing was enabled only through proprietary rails – private companies took the initiative to design their own infrastructure for data sharing which end up restricting players like yourselves from innovating to design new products and services which could benefit people on top of the infra.

What other kinds of innovative products and services could you build?

Think of the impact that access to the Google Maps APIs allowed: without them, we would never have seen startups like Uber or Airbnb come to life. Building these consented data sharing APIs as a public good allows an explosion of fintech innovation, in areas such as:

New types of tailored flow-based lending products that provide regular, sachet sized loans to different target groups based on GST or other invoices (as described above).

New personal financial management apps which could help consumers make decisions on different financial institutions and products (savings, credit, insurance, etc.) based on historic data and future projections. This could also branch out into improved wealth management or Robo advisory.

Applications that allow individuals to share evidence of financial status (for instance, for a credit card or visa application) without sharing a complete detailed bank statement history of every transaction

…and many others, such as that germ of an idea that’s possibly started taking shape in your mind as you were reading.

In summary

This ecosystem is where UPI was in mid-2016: with firm, interdepartmental, and long term regulatory backing, and at the cusp of operationally taking off. UPI taught us that those who make a bet on the future, build and test early (PhonePe and Google were both at the first ever UPI hackathon!), and are agile enough to thrive in an evolving landscape end up reaping significant rewards. And just as with UPI, our financial sector regulators are to be lauded for thinking proactively and years ahead by building the right public infrastructure for data sharing. RBI’s planning for this began back in 2015! They have now passed the innovation baton onto you — and we, for one, have ambitious expectations.

With warmest regards,

iSPIRT Foundation

I’m Pinging A Few Whatsapp Groups Now, What Else Should I Send Them To Read?

Join us for a conversation with Vinod Khosla and Nandan Nilekani. Together with Sharad Sharma, our fireside chat host, they will talk about what it means to be an entrepreneur in India today and how these entrepreneurs can solve the hardest problems of India.

Vinod Khosla and Nandan Nilekani are arguably two of the most influential thinkers and innovators of our time when it comes to transformation, entrepreneurship, and large scale impact. Born within 6 months of each other, both graduated for IITs, created iconic companies, become billionaires in the in aprocess and continue to innovate and transform the world.

What better opportunity than to hear these icons of industry at a fireside chat discussing the most intriguing aspects of startups, entrepreneurship, digital transformation and India’s growth towards a multi trillion dollar economy.

About Mr. Vinod Khosla

Vinod Khosla is the founder of Khosla Ventures, a premier Silicon Valley venture capital firm, and a member of the 2018 Midas List. His firm, Khosla Ventures, invests in a wide variety of startups ranging from Healthcare, Sustainable Energy, Food/Agriculture to Space, AI and Robotics. He co-founded Sun Microsystems in 1982 after which he spent 18 years at venture capital firm Kleiner Perkins Caufield & Byers before launching his own fund.

About Mr. Nandan Nilekani

Nandan Nilekani is the co-founder of tech giant Infosys and currently back as a non-executive chairman affecting a remarkable turnaround. In 2009, he was made a Cabinet Minister and Chairman of UIDAI – India’s mammoth National ID project – Aadhaar. After Aadhaar, Nandan has actively supported India’s digital transformation through the IndiaStack initiatives in payments, digital locker, eSignature and other services. Nandan has also backed startups in the India ecosystem.

About Mr. Sharad Sharma

Sharad Sharma is the co-founder of iSPIRT and has worn many hats as CEO of Yahoo India R&D, Chair of NASSCOM Product Forum and as intrapreneur at AT&T. He is a passionate evangelist and an active investor in the software product ecosystem in India.

When?

2nd of August, 2019 from 18:00 – 19:30 hrs. Venue to be disclosed.

How to participate?

You can be a part of this Fireside Chat by registering here. Confirmed participants will be intimated by the 28th of July via email.

Please note, due to limited seating at the venue we will not be able to accommodate everyone who applies.

More commonly known as the ‘Consent Layer of the India Stack’, Data Empowerment and Protection Architecture (DEPA) is a new approach, a paradigm shift in personal data management and processing that transforms the currently prevalent organization-centric system to a human-centric system. By giving people the power to decide how their data can be used, DEPA enables the collection and use of personal data in ways that empower people to access better financial, healthcare, and other socio-economically important services in a safe, secure, and privacy-preserving manner.

It gives every Indian control over their data, democratizes access and enables the portability of trusted data between service providers. This architecture will help Indians in accessing better financial services, healthcare services, and other socio-economically important services.The rollout of DEPA for financial data and telecom data is already taking place through Account Aggregators that are licensed by RBI. It covers all asset data, liabilities data, and telecom data.

We, at iSPIRT, organised a learning session on the 18th of May, to give relevant and interested stakeholders a detailed primer on DEPA. We had 60-odd very animated and engaging people in the audience. The purpose of the session was to understand the technological, institutional, market and regulatory architecture of DEPA, it impacts on existing data consuming businesses and how people could contribute to this new data sharing infrastructure that’s being built in India.

The session was anchored by Siddarth Shetty, Data Empowerment And Protection Architecture Lead & Fellow, iSPIRT Foundation (Email – sid@ispirt.in). Please feel free to reach out to him for any queries regarding DEPA.

Last week we wrote about India’s Health Leapfrog and the role of Health Stack in enabling that (you can read it here). Today, we talk about one component of the National Health Stack – Federated Personal Health Records: its design, the role of policy and potential use cases.

Overview

A federated personal health record refers to an individual’s ability to access and share her longitudinal health history without centralised storage of data. This means that if she has visited different healthcare providers in the past (which is often the case in a real life scenario), she should be able to fetch her records from all these sources, view them and present them when and where needed. Today, this objective is achieved by a paper-based ‘patient file’ which is used when seeking healthcare. However, with increasing adoption of digital infrastructure in the healthcare ecosystem, it should now be possible to do the same electronically. This has many benefits – patients need not remember to carry their files, hospitals can better manage patient data using IT systems, patients can seek remote consultations with complete information, insurance claims can be settled faster, and so on. This post is an attempt to look at the factors that would help make this a reality.

What does it take?

There are fundamentally three steps involved in making a PHR happen:

Capture of information – Even though a large part of health data remains in paper format, records such as diagnostic reports are often generated digitally. Moreover, hospitals have started adopting EMR systems to generate and store clinical records such as discharge summaries electronically. These can act as starting points to build a PHR.

Flow of information- In order to make information flow between different entities, it is important to have the right technical and regulatory framework. On the regulatory front, the Personal Data Protection Bill which was published by MeitY in August last year clearly classifies health records as sensitive personal data, allows individuals to have control over their data, and establishes the right to data portability. On the technical front, the Data Empowerment and Protection Architecture allows individuals to access and share their data using electronic consent and data access fiduciaries. (We are working closely with the National Cancer Grid to pilot this effort in the healthcare domain. A detailed approach along with the technical standards can be found here.)

Use of information – With the technical and regulatory frameworks in place, we are now looking to understand use cases of a PHR. Indeed, a technology becomes meaningless without a true application of it! Especially in the case of PHR, the “build it and they will come” approach has not worked in the past. The world is replete with technology pilots that don’t translate into good health outcomes. We, in iSPIRT, don’t want to go down this path. Our view is that only pilots that emerge from a clear focus on human-centred design thinking have a chance of success.

Use cases of Personal Health Records

Clinical Decision Making

Description: Patient health records are primarily used by doctors to improve quality of care. Information about past history, prior conditions, diagnoses and medications can significantly alter the treatment prescribed by a medical professional. Today, this information is captured from any paper records that a patient might carry (which are often not complete), with an over-reliance on oral histories – electronic health records can ensure decisions about a patient’s health are made based on complete information. This can prove to be especially beneficial in emergency cases and systemic illnesses.

Problem: The current fee-for-service model of healthcare delivery does not tie patient outcomes to care delivery. Therefore, in the absence of healthcare professionals being penalised for incorrect treatment, it is unclear who would pay for such a service; since patients often do not possess the know-how to realise the importance of health history.

Chronic Disease Management

Description: Chronic conditions such as diabetes, hypertension, cardiovascular diseases, etc. require regular monitoring, strict treatment adherence, lifestyle management and routine follow-ups. Some complex conditions even require second opinions and joint decision-making by a team of doctors. By having access to a patient’s entire health history, services that facilitate remote consultations, follow-ups and improve adherence can be enabled in a more precise manner.

Problem: Services such as treatment adherence or lifestyle management require self-input data by the patient, which might not work with the majority. Other services such as remote consultations can still be achieved through emails or scanned copies of reports. The true value of a PHR is in providing complete information (which might be missed in cases of manual emails/ uploads, especially in chronic cases where the volume and variety of reports are huge) – this too requires the patient to understand its importance.

Insurance

Description: One problem that can be resolved through patient records is incorrect declaration of pre-existing conditions, which causes post-purchase dissonance. Another area of benefit is claims settlement, where instant access to patient records can enable faster and seamless settlement of claims. Both of these can be use cases of a patient’s health records.

Problem: Claim settlement in most cases is based on pre-authorisation and does not depend solely on health records. Information about pre-existing conditions can be obtained from diagnostic tests conducted at the time of purchase. Since alternatives for both exist, it is unclear if these use cases are strong enough to push for a PHR.

Research

Description: Clinical trials often require identifying the right pool of participants for a study and tracking their progress over time. Today, this process is conducted in a closed-door setting, with select healthcare providers taking on the onus of identifying the right set of patients. With electronic health records, identification, as well as monitoring, become frictionless.

Problem: Participants in clinical trials represent a very niche segment of the population. It is unclear how this would expand into a mainstream use of PHR.

Next steps

We are looking for partners to brainstorm for more use cases, build prototypes, test and implement them. If you work or wish to volunteer in the Healthtech domain and are passionate about improving healthcare delivery in India, please reach out to me at [email protected].

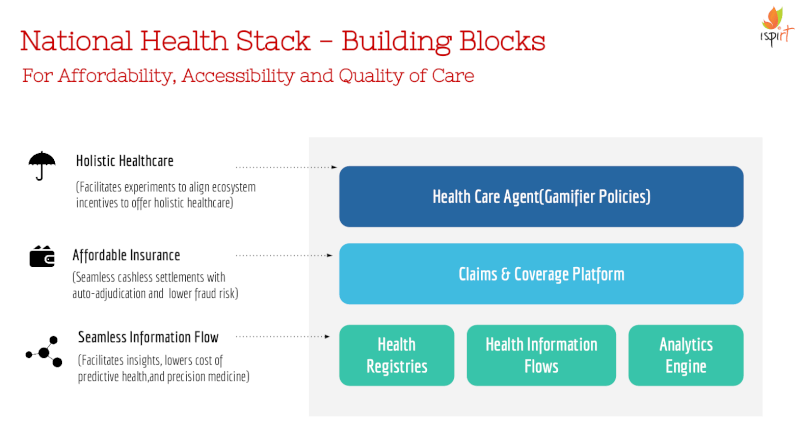

In July 2018, NITI Aayog published a Strategy and Approach document on the National Health Stack. The document underscored the need for Universal Health Coverage (UHC) and laid down the technology framework for implementing the Ayushman Bharat programme which is meant to provide UHC to the bottom 500 million of the country. While the Health Stack provides a technological backbone for delivering affordable healthcare to all Indians, we, at iSPIRT, believe that it has the potential to go beyond that and to completely transform the healthcare ecosystem in the country. We are indeed headed for a health leapfrog in India! Over the last few months, we have worked extensively to understand the current challenges in the industry as well as the role and design of individual components of the Health Stack. In this post, we elaborate on the leapfrog that will be enabled by blending this technology with care delivery.

What is the health leapfrog?

Healthcare delivery in India faces multiple challenges today. The doctor-patient ratio in the country is extremely poor, a problem that is further exacerbated by their skewed distribution. Insurance penetration remains low leading to out-of-pocket expenses of over 80% (something that is being addressed by the Ayushman Bharat program). Additionally, the current view on healthcare amongst citizens as well as policymakers is largely around curative care. Preventive care, which is equally important for the health of individuals, is generally overlooked.

The leapfrog we envision is that of public, precision healthcare. This means that not only would every citizen have access to affordable healthcare, but the care delivered would be holistic (as opposed to symptomatic) and preventive (and not just curative) in nature. This will require a complete redesign of operations, regulations and incentives – a transformation that, we believe, can be enabled by the Health Stack.

How will this leapfrog be enabled by the Health Stack?

At the first level, the Health Stack will enable a seamless flow of information across all stakeholders in the ecosystem, which will help in enhancing trust and decision-making. For example, access to an individual’s claims history helps in better claims management, a patient’s longitudinal health record aids clinical decision-making while information about disease incidence enables better policymaking. This is the role of some of the fundamental Health Stack components, namely, the health registries, personal health records (PHR) and the analytics framework. Of course, it is essential to maintain strict data security and privacy boundaries, which is already considered in the design of the stack, through features like non-repudiable audit logs and electronic consent.

At the second level, the Health Stack will improve cost efficiency of healthcare. For out-of-pocket expenditures to come down, we have to enable healthcare financing (via insurance or assurance schemes) to become more efficient and in particular, the costs of health claims management to reduce. The main costs around claims management relate to eligibility determination, claims processing and fraud detection. An open source coverage and claims platform, a key component of the Health Stack, is meant to deal with these inefficiencies. This component will not only bring down the cost of processing a claim but along with increased access to information about an individual’s health and claims history (level 1), will also enable the creation of personalised, sachet-sized insurance policies.

At the final level, the Health Stack will leverage information and cost efficiencies to make care delivery more holistic in nature. For this, we need a policy engine that creates care policies that are not only personalized in nature but that also incentivize good healthcare practices amongst consumers and providers. We have coined a new term for such policies – “gamifier” policies – since they will be used to gamify health decision-making amongst different stakeholders.

Gamifier policies, if implemented well, can have a transformative impact on the healthcare landscape of the country. We present our first proposal on the design of gamifier policies, We suggest the use of techniques from microeconomics to manage incentives for care providers, and those from behavioural economics to incentivise consumers. We also give examples of policies created by combining different techniques.

The success of the policy engine rests on real-world experiments around policies and in the document we lay down the contours of an experimentation framework for driving these experiments. The role of the regulator will be key in implementing this experimentation framework: in standardizing the policy language, in auditing policies and in ensuring the privacy-preserving exchange of data derived from different policy experiments. Creating the framework is an extensive exercise and requires engagement with economists as well as computer scientists. We invite people with expertise in either of these areas to join us on this journey and help us sharpen our thinking around it.

Do you wish to volunteer?

Please read our volunteer handbook and fill out this Google form if you’re interested in joining us in our effort to develop the design of Health Stack further and to take us closer to the goal of achieving universal and holistic healthcare in India!

Dalberg and iSPIRT invite applications from early-stage ventures that are tech-

based solutions leveraging the India Stack platform at the core of their business

model to bring financial or transactional services to the underserved in India.

Pitch to some of the leading investors and thinkers in the Indian start-up ecosystem,

including the Bharat Innovations Fund, Omidyar Network and Unitus Seed Fund.

Winners will spend an hour of 'Think Time' – a mentorship session with

technology evangelist Nandan Nilekani.

Who are we looking for?

We are open to all innovations that use the India Stack to unlock new business

models or reach previously underserved new customer segments across sectors

such as financial services, education, healthcare and others. Some core focus areas

for the competition may include digital lending and supporting activities, such as

alternative credit scoring; sector specific affordable digital finance services such as

health insurance or education loans; sector specific digital services such as skilling

and certification, property registration agreements, patient-centric healthcare

management; and SaaS platforms “as a service” that support the development of

other India Stack based innovations such as Digi-locker or e-sign providers.

Who is eligible?

All applicants should:

1. Meet the 3-point criteria: tech enabled, leveraging India Stack Platform and

serving the underservedBe

2. Be a part of two (minimum) to four (maximum) members team including the

founder of the companyBe early stage start-ups that have received only seed (or limited angel)

3. Be early stage start-ups that have received only seed (or limited angel)

funding, if at all

What is in it for you?

The investor group, comprising of Bharat Innovations Fund, Omidyar Network and

Unitus Seed Fund, is a network of investors and operators, entrepreneurs and

technologists, designers and engineers, academicians and policy makers, with the

singular mission to solve some of India’s toughest problems.

Through this event you have an opportunity to receive:

-Exclusive focus on tech innovations that leverage the India Stack platform

and have the potential to address the underservedFlexible

-Flexible, insight driven, funding of up to Rs. 8 lakhs for early stage, innovative

modelsStrategic

-Strategic business support, through their specialists to support investees in

their strategy and growthA chance to be a part of the India Stack ecosystem through partnerships,

-A chance to be a part of the India Stack ecosystem through partnerships,

pilots, workshops, conferences and network building exercises

Visit www.buildonindiastack.in and send your pitch now.

Chit Funds are indigenous financial institutions in India. It is a mechanism that combines credit and savings in a single scheme. In a chit fund scheme, a group of individuals come together for a predetermined time period and contribute to a common pool at regular intervals. Every month, up until the end of the tenure of the scheme, the collected pool of money is loaned out internally through a bidding mechanism to the most deserving member. This way, people who are in need of funds and those who want to save are able to meet their requirements. Similar schemes have been known to be popular across the developing world, generally referred to as Rotating Saving and Credit Associations (ROSCA)

An interesting aspect of Chit Funds in India is that the industry is highly regulated and institutionalized. A Chit Fund can be either “registered” or “unregistered”. Registered Chit funds are organized by Chit Fund firms/companies and regulated by the Chit Fund Act. They are in essence impersonal contracts that depend on market forces. Unregistered Chit Funds which exceed Rs. 100 ($2) in chit value are illegal in India, although it is widely known that the unregistered Chit Funds industry is still very popular.

While no official or government estimates of the industry exist, The All India Chit Fund Association estimates that “the size of industry is Rs 35,000 crore, with the unregistered part estimated to be at least 100 times the registered one”

Value to the consumer

Prof Mary Kay Gugerty, in her paper, “You Can’t Save Alone: Commitment in Rotating Savings and Credit Associations in Kenya” argues that, “saving requires self-discipline, and ROSCAS provide a collective mechanism for individual self-control in the presence of time-inconsistent preferences and in the absence of alternative commitment technologies”

This conclusion, although based in data from Kenya, is also supported by the data collected in India, which suggests that 72.1% of consumers participate in chit funds(Estimate of Chit Fund Industry size) to save. While 95% of these consumers have bank accounts(Reason for Chit participation : Table 3-7), they still prefer chit funds as a saving mechanism due to higher perceived returns, paperless documentation(Banking Details : Table 3-4), familiarity and doorstep service.

Housewives and Small business owners are the two most prominent cohorts within the chit fund users(Figure 3-1 Frequency of Occupation based on Gender). Daily chits are popular with small business owners, presumably because it allows them to manage their daily cash flow and allows control over their interest rate when the need for a loan arises(Section 9, Chit funds and Small Business, Para 3).

The chit funds are also perceived to be liquid, Most consumers bid to get the pot when they had an emergency need or when an lucrative business investment came about(Reason for participating in Chit Funds : Table 3-11).

Finally 96% of chit members overall think that the Chit Funds they participate in are safe and about 85% of these chit members are loyal to fund company they are participating in.

Legal framework for Chit Funds

The Government of India passed the Chit Fund Act in 1982, with implementation of the Act left to the Registrar of Chit Funds in each state. This Act, it is relevant to note, contains many restrictions like a minimum Capital requirement (Section 8), prohibition of transacting business other than Chit Business (Section 12), a ceiling on the aggregate chit amount which is 10 times of the net-owned funds (Section 13), Utilization of funds (Section 14), security to be given for full value of chit (Section 20), a self-contained machinery for settlement of disputes etc and a number of penal provision for various defaults(All India Chit Funds Association submission to parliamentary committee), etc.. Notably there are stringent requirements on written formalities like notice to the customer, minutes of the meeting, record keeping and audit by certified chartered accountant(6(1), 15, 35, 40-Chit Agreement, 22(2)- Intimation to Registrar of deposits, 26(1), 34(1) Withdrawal of foreman 28(1) Removal of defaulting subscribers 33(1) Demand note 38(1) Minutes of the meeting).

The regulatory hurdles that the chit companies face due to the stringent rules proposed by the Government progressively, have been a setback to the growth of the industry. The effect of the increased costs of operations for the registered chit companies has been to push these companies ’underground’. Many companies have, in the recent past, either folded up or shifted their operations entirely to the informal arena becoming an ’unregistered’ chit fund(Chit Funds Boon to Small Enterprise).

The key source of revenue for a Chit fund manager is commission which is capped at 5%. Alternatively the chit fund managers take the first installment in full. The chit manager can also generate revenue from float interest charges i.e. by disbursing the loan a month after the money is collected, he can earn the interest on the full amount(Section 7 : Sources of Income to the Chit Manager)

Role of the India Stack

With the size and scope of the chit fund industry, as outlined above, it is clear that there is a large addressable market for innovators. What makes this opportunity more lucrative is the presence of India Stack. India Stack is set of technologies (primarily Aadhaar authentication, e-KYC, e-Sign, Digital locker and UPI) that together dramatically reduce the cost of transactions. For example, an analysis on the Mutual funds business indicated that by use of India stack, the average transaction cost would drop from Rs 50 to Rs 2, making it viable for Mutual funds to go after the small ticket business.

Opportunities for Start Ups

Given the background above, following is the most promising opportunity for startups:

Organize the unregistered chit fund companies

Hypothesis: With the recent crackdown on black money and tax evasion, it will become more difficult to run unregistered chit funds circumventing the law. This will give the unregistered chit funds incentive to become registered and follow the law

Product: An easy platform that allows management of chit funds through mobile phone app/apps and make it compliant with the law

Key Customers : Unregistered chit funds

Key Stakeholders : State Government, Unregistered Chit Funds, Users of chit funds

Key activities:

Build technology based on India Stack to meet KYC requirements, sign chit agreements using e-sign, transfer money between people using UPI and keep an account.

Strong sales network to bring the chit funds onboard

Product and legal expertise to liaison with the state governments and registered chit funds to build products that meets all requirements

Need for funding:

Initial product could be built with a relatively small investment

Scaling with scale will likely need venture investments (but no access to large capital should be needed)

Revenue generating activity:

Pay per instance or per user from the funds

Lead generation for Chartered Accountants

Aggregate data reports could be sold

Could also build a government facing interface for monitoring

Competitive Advantage:

No real competition at this point

Network effects could become significant advantage

Implicit or explicit endorsement from Government agencies

Key Risks:

Product adoption risk: The success of the idea is hinged on pressure from government creating the need, which drives adoption. In the absence which it will be significantly harder to move people from the familiar. The risk is somewhat contained because of a supreme court order directing government to act on this.

Regulation risk: A parliamentary committee has recommended that the government revise the regulation. This means that government could do away with a number of provisions, making compliance much easier of chit funds thus eliminating the need for such a company. Again this is low likelihood event given the scrutiny on this sector

Reputation risk: The company will have to be careful not to associate with chit funds with malicious intents. Being associated could result in penalties and damage to reputation.

Guest Post by Kunal Kashyap, IIT KGP graduate, Spent 8 years at Capital One, a US based Fortune 100 Fintech company. Volunteer for iSPIRT.

A phenomenon that has been pretty popular recently in the news goes by the name of UPI(Unified Payments Interface). However, most people have not been able to experience the revolution and the magic moment that comes along when paying via it.Part of that stems from the myths that keep floating around, regarding how it might not be that secure and worthwhile. Well, allow me to put all of these doubts at ease through this post.

Let us take all the salient features of UPI one by one –

Bye-bye long account numbers and IFSC codes

Convenience factor

Now, there is no need to ask anyone for their account numbers or IFSC codes when sending or receiving money. Apart from the fact that remembering long account numbers and IFSC codes is cumbersome, entering those on a small screen / app is painful (especially considering that the user experience of banking websites and apps is mostly terrible).

Of course, the question is now what replaces these 2 if they are not in the picture any more. Say hello to virtual address (which looks like sunnyrohit@ybl where the first part is a unique ID set by you and the second part is determined by the bank/app which processes your payments). This virtual address is automatically mapped to your bank account by NPCI when you register for the first time.

Security factor