iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

iSPIRT has been actively engaged in pursuing the favourable policy for the Cloud Telephony sector in Telecom Industry, an amalgamation of the various IT and Communications technologies.

National Digital Communication Policy has been announced recently and it is encouraging to see the announcements in the policy on some common issues to do with Startup ecosystem and digital communication aspects of the Cloud Telephony Players.

We are expecting the Department of Telecom (DOT) to further work on implementation and framing of rules and regulation in light of policy in near future. Despite many positive directional changes, there is a need to develop a regulatory framework for the Cloud Telephony players. Cloud Telephony players are adding value to communication and hence to the economy in several innovative ways. In addition, they also add a good revenue stream to licenses Telecom Service Providers (TSPs).

This PolicyHacks session is devoted to the critical analysis of the NDCP for this sub-sectoral player. Some of the entrepreneurs involved in the discussion are Gurumurthy Konduri of Ozonetel, Ujwal Makhija of PhoneOn, Gaurav Agrawal of Exotel and Gaurav Sawhney of Knowlarity.

A recording of this discussion is given below. Please feel free to click and watch. (About 20 seconds lost in the opening frame, apologises for the error)

The main point covered in the discussion is summed up below as are the some of our recommendations and good work is done (while the Policy was in the draft stage and during various consultation processes), which have been reflected in the policy under respective sections as under:

Page 7

1.1.(f) – Encourage and facilitate sharing of active infrastructure by enhancing the scope of Infrastructure Providers (IP) and promoting and incentivising the deployment of common sharable, passive as well as active, infrastructure

1.1.(g).iv. – Allowing benefits of convergence in areas such as IP-PSTN switching.

Both of these are encouraging moves however it is to be seen how further rules and framework make easy for Small and Startup companies to use them without licensed TSPs creating a barrier for them.

Page 8

1.1.(j) – By encouraging innovative approaches to infrastructure creation and access including through resale and Virtual Network Operators (VNO)

This is a very encouraging announcement for the Cloud Telephony startups.

Page 14

2.1. (c ) iv. – Improving the Terms and Conditions for ‘Other Service Providers’, including definitions, compliance requirements and restrictions on inter-connectivity

2.1.(c ).viii. – Creating a regime for fixed number portability to facilitate one nation – one number including portability of toll-free number, Universal Access numbers and DID numbers

Again very encouraging but needs some boost up. Audiotex regime must go most speakers feel and all the players in Cloud telephony are treated as ASP. These provisions will help cloud telephony to deliver better value propositions in their offerings.

Page 15

2.2.(a) iv: – Encourage use of Open APIs for emerging technologies

2.2. (b) – Promoting innovation in the creation of Communication services and network infrastructure by Developing a policy framework for ‘Over The Top’ (OTT) services.

2.2.(f) ii. – Enabling a light touch regulation for the proliferation of cloud-based systems

2.2.(f).iii. – Facilitating Cloud Service Providers to establish captive fibre networks.

A welcome move to encourage Open APIs. However, licenses TSP should be given one standard that is governed by DOT to implement any APIs that let them monitor cloud telephony or ASPs on their network, instead of allowing them to create a regime of their own.

Generally, an OTT policy is recommended in reforming the sector. However, OTT framework should not be mixed with ASP or Cloud Telephony providers. It is better to keep a distinction between the two.

Page 17:

2.4.(a).ii: – Promoting participation of Start-ups and SMEs in government procurement

2.4.(b). – Reducing the entry barriers for start-ups by reducing the initial cost and compliance burden, especially for new and innovative segments and services.

Acceptance of these issues is very encouraging. The Government can be a very big user of the Cloud Telephony industry also. And we hope this will turn out to be a winning proposition for the Cloud Telephony industry in near future.

Conclusion

Whereas this policy announcement reflects a positive change, it is yet to be seen how DOT look at Cloud Telephony and provides it with a recognition as a sub-sector with easy and proper regulatory framework for same.

Note: The above article is co-authored by Gurumurthy Konduri of Ozonetel with Sudhir Singh of iSPIRT

Data protection and privacy have been a topic of hot debates and discussion in recent times in India. It had become extremely important as India is progressing to a be a “Digital economy” to address this issues relating to the use of personal data.

iSPIRT has been in forefront of developing Consent Framework and called as Data Protection & Empowerment Architecture (DEPA). The Account Aggregator Policy of RBI revolves around this consent architecture.

Whereas the bill is of interest to almost all the sectors of the economy, it is extremely important for businesses in Information Technology sector and especially in Software product Industry to understand the law as it is seeded and further as it evolves.

The bill has many aspects to it in the legal framework. It is not possible to cover the entire understanding of the bill in one blog. We have attempted to cover some salient features that may be important for the Software Product Industry as well as how it contacts with the techno-legal aspects of DEPA as it stands in financial sector, perhaps to be replicated in other important sectors of the economy.

This blog is again posted in a Question and answer format both as a video and as a transcript of the video. You can use the one you like.

Questions have been asked by iSPIRT volunteer and Policy expert Mr Sudhir Singh and answered by Supratim Chakraborty (Data Privacy and Protection expert from Khaitan & Co.) and Siddharth Shetty (leading the DEPA initiative at iSPIRT).

What are the most important aspects of the bill?

Supratim answered, “What we have seen is through this draft bill, there is an attempt to establish the relationship of trust between the data subject and data controller. The nomenclature has been changed in this bill and It is data fiduciary and data principles. It puts a lot of onus on the data fiduciary to take care of data care protection.”

“There are several important aspects of the bill that needs attention such as localisation of data, cross-border transfer and also some other aspects such as privacy by design, transparency requirement, security safeguard, breach notification, grievance redressal mechanism, the requirement of Data protection officer, record keeping requirements”, as elaborated Supratim.

Is there some restriction on data fiduciary? Is the state exempted?

Supratim said, “this bill is equally applicable to private parties and the Government unlike earlier provisions of section 43A and 72A of IT ACT. 43A will be scrapped after this bill comes into existence. There has been a lot of debate on this aspect of bringing Govt. under the purview of the law.”

Is right to be forgotten covered in a similar way as GDPR?

Supratim explained, “Our Govt. has looked at this in a more business-friendly way by covering the right to be forgotten by provisioning that any further dissemination of data should be stopped, once the data principal chooses to withdraw the consent or ask for the right to be forgotten.”

He described four governing aspect that explains how to determine the aspect of keeping Data local, as described below.

You could have certain pockets of personal data that can be transferred outside.

There could be certain pockets of data that could be transferred outside but a serving copy of the data has to be within the country

The third category is sensitive personal data ambit of sensitive personal data which has been widened considerably compared to what we saw under the 43A of IT ACT. For this, if sent out of

The fourth category is data that cannot be sent outside country at all.

“On Cross border transfer of data in addition to ‘consent’ there has to be standard contractual clauses (approved/prescribed by authority) or the transfer to a jurisdictions is approved by the central government”, he further explained.

What is the Data Protection Authority?

Supratim answered, “In the draft bill this seems to be all encompassing all powerful authority from rulemaking to advisory to enforcement. Therefore it is important to see how this really shapes up. In “IT Act”, section 43 A and 72A were largely there to cover the aspects of data privacy but enforcement and implementation.”

What are other important aspects to consider?

“There are many aspects but let us touch upon two given below”, said Supratim.

One is the requirement of having notices in multiple languages, which is not a very hard obligation the way it has been put. But in a country like India for say an e-commerce platform imaging the cost that one has to incur for putting multiple language notices. Also, we need to see are we able to really address the point of informed consent through this, because you also have a section of people who may be illiterates. Justice Srikrishna report suggest that we should have short videos or graphical representation which make it very easy for someone to understand the critical aspects of privacy.

Another important aspect is applicability of the law. This law is applicable to all processing that is happening in India and also to foreign bodies. Section 2(2) talks about applicability to foreign bodies, the first part says that “in connection with any business carried out in India”. This means a global platform that is accessible from India has to have the entire requirement of this law.

Are we going in direction of GDPR?

Supratim answered, “Whereas we are trying to follow the Gold standard and many countries are trying to follow the path set by GDPR, India is quite different country and we are not following everything the way it is in GDPR, we have to be mindful of our requirements. But the idea is slowly and surely reach a zone where we can have our laws quite akin to laws of matured jurisdictions.”

How does Bill address iSPIRT DEPA initiative?

Siddharth, sees this draft bill as a unique India first approach. He feels that apart from addressing privacy and data protection aspects it empowers Indians on having control on the use of their data for better financial services, better health services, education etc.

Siddharth goes on to explain that at iSPIRT for past 3-4 years we have been working at Consent layer of IndiaStack or Consent framework and it is great to see that bedrock of draft bill is actually based on consent and in that way it is somewhat similar to GDPR. But, one of the biggest problem they are facing in EU today is it is very difficult to operationalise consent. It is for the first time India has a unique infrastructure to operationalise consent.

“DEPA is nothing but a set of two tools that helps to operationalise consent, explains Siddharth.

One is known as Digital Locker system which allows to the federated exchange of data and second is known as electronic data consent, which is nothing but an electronic representation of user Consent.

“This means, if you want to share or allow your data from some provider to say another consumer, then you must be able to express what date you want to share with whom for what time period in some codified manner. This codified information or consent is known as consent artefact”, says Siddharth further.

As explained by Siddharth, the ‘consent artefact’ became a national standard in 2016 adopted by four financial sector regulator RBI, PFRDA, IRDA and SEBI and they adopted it for their entire eco-system.

Based on consent artefact every individual has an access to financial data and has a mechanism to share that data to gain access to a loan or any other services provider. This has been through an institutional mechanism called Account aggregator.

Siddharth further elaborated that, “the ‘Account aggregator’ (AA) is a class of entities known as data access fiduciaries. The AA unlike other parts of world decouples the institution that collecting consent from an institution that either consuming data or providing data. In EU e.g. as per of PSP2 directive the account information service provider which consumes data is also responsible for collecting the data.”

In India, 3 AA have been approved. Technical standard drafts are also out for ecosystem. And through AA you actually have an entity that’s working toward creating an informed consent experience. Going forward just like UPI you receive your consent for a payment, through AA you will have an entity that helps you provide and control consent. Based on Financial sector we have proposed a similar concept to TRAI for the telecom sector and health sector to NITI Ayog.

Has the AA concept been addressed in the bill?

Siddharth explains further, “The bill makes bedrock of most processing of data based on consent. AA model is nothing but your consent collector or Consent manager. Every data principle they have outlined right to confirmation and access, right to correction, most importantly the right to data portability. As a data principle from data fiduciary, you have the right to request and port machine structured non-reputable transaction history or any other user-generated data to other service providers. AA is nothing but a framework to operationalise this right.”

He further explained that in the report preceding the bill, they talk about a concept consent dashboard. AA is nothing but a consent dashboard. They had 2 tech innovation consent dashboard and data dashboard. You can log consent flows and data flows.

Will, there be consent dashboards concept like AA in other sectors also or will there be one single point authority under DPA?

Siddharth, “it would be a combination of both. If you see the draft bill, it allows sectoral regulators to write rules. For data the falls under private data sets category such as data pertaining to social media etc, DPA would prescribe an standard.”

The report talks about that dashboard can be maintained by each data fiduciary or it can be a common dashboard that everyone else agrees and follows. If you look at the account aggregator dashboard it is a common dashboard for the entire financial sector. But for social media companies can follow their won dashboards.

For any Software product companies that does not lie in any of the regulated sector can create their own consent dashboards, where the user can come see their dashboard correct their data, port the data, manage their consent.

Unlike the IT act, this regulation will have a direct bearing on any businesses processing data irrespective of being in a Software product or other domain. And hence there is a need to be attentive. How right is this aspect?

“Yes, the ambit increases quite a bit. Wherever there is sensitive personal data interface involved, the level of compliance requirement has gone up several times. In the IT Act, there was a mention of personal data in section 72A. The present draft bill does not talk about the deletion of 72A. The draft bill have a parallel mechanism set out in the IT Act”, mentioned Supratim.

Siddharth, “it is just not limited to compliance, this law unlocks the whole host of business models around data sharing around consented data sharing that you haven’t yet seen in any other country and it will be really interesting to space to see what companies get a build out there.”

Question from Participants.

What is the definition of data processing? Or what is the differentiation between Data Storage and Data Processing. E.g. if you are an email service provider, is it Data Storage or Data Processing? (asked by Chintan)

Supratim answered, “definition of data processing is extremely wide enough to make businesses fall in to ‘data processing category’ without being a processor.”

What is the timeline? (Asked by Chintan)

MeitY has asked for public comments by 10th of September on the draft bill, thereafter it will be presented to parliament and after promulgation, there will be more work in framing Authority, the rules by DPA etc. The law is not expected to be in implementable form only after 18 Months or so, minimum.

What happens to the Existing customer? Do we go back to them and get their consent? (Karthik)

Supratim answered, “whilst the it is not a retrospective legislation, if you continue processing without taking consent, you will fall foul of the requirement of law.”

Are there any fines defined here? (Karthik)

Yes, it has been taken care. Just like other aspects the draft bill he highly inspired by GDPR on this aspect also. We have 4% and 2% of annual turnover. There are 2 buckets 4% and 15 Cr and other is 2% and 5 Crore.

Do we need to appoint an DPO?

“There is a segregation which has been made of has significant Data Fiduciary under certain conditions will have to have DPO. Also, this law has an immense amount of significant rulemaking power, answered Supratim.

Hence, it will be seen in future how rules are framed by Authority. So, it has to be seen how business friendly the authority remains in rulemaking e.g. section 43A in IT ACT gave rule making power to define what is sensitive data and information and set out what is reasonable practices and procedure. In the rule made in future, we saw a plethora of requirements set out, over legislated and sometimes badly drafted.

The rules will go through an evolutionary cycle. Hence, the legislation has to be tested over a period of time as it unfolds, after crystallisation of this draft promulgation by parliament in to an ACT and rules being made after that on different aspects.

Disclaimer

PolicyHacks, and publications thereunder, are intended to provide a very basic understanding of legal/policy issues that impact Software Product Industry and the startups in the eco-system.

PolicyHacks, therefore, do not necessarily set out views of subject matter experts, and should under no circumstances be substituted for legal advice, which, of course, requires a detailed analysis of the relevant fact situation and applicable laws by experts in the subject matter on the case to case basis.

If you are facing an issue, we recommend you take expert professional advice on the case to case basis.

We intend to provide the best transcripts in the text part of the blog. However, it may not be an exact replica and maybe approximation, more standardised, normalised or moderated version of the expert view presented in the video.

The government of India had announced a Preferred Market Access (PMA) policy for Cyber Security products through an order notifying the Public Procurement (Preference to Make in India).

MeitY shall be the nodal Ministry to monitor and administer this PMA policy.

iSPIRT has been pursuing with MietY, application of PMA for all Indian Software Products to promote the Indian Software product industry and it is heartening to note that at least one important sub-sector of Cybersecurity has caught the Government’s attention.

iSPIRT organised a PolicyHacks session to understand this policy announcement with Ashish Tandon Founder & CEO of Indusface and Mohan Gandhi of Entersoftsecurity.

You can watch the discussion with Ashish and Mohan at below given YouTube video, in a question and answer format with Sudhir Singh.

What are the essential features of this Policy?

Ashish described the main features stating that this is a policy that is going to help boost Cybersecurity products in India. Govt. of India identified areas that require boosting ‘make in India’ products for the sensitive areas of cybersecurity.

Is there a way product companies can register or Government is going to keep a registry of ‘made in India’ products?

Ashish explains the policy has provided for the formation of a committee that will further provide for a process for empanelment of Indian Cybersecurity products and Indian Cybersecurity product companies with some defined key aspects that would qualify for empanelment.

Ashish further explained that as the empanelment aspects are decided there may also come up with a process for testing and meeting standards and quality norms etc.

Are there are enough product companies in ‘Cyber Security’ space for empanelment?

Mohan Gandhi answered that there are several product companies, but this policy should further strengthen the ‘make in India’ aspect and companies based out of India with deep tech product can look at getting this advantage of this policy.

Whether the Policy will be applicable to “productized services”?

Ashish answered, that this policy is applicable to the only product and at best give preference to made in India products in turnkey projects wherein a large project cybersecurity product is involved.

How will this policy help Start-up companies in Indian Market?

Mohan mentioned, that one interesting thing about this policy is that, it clearly talks about intellectual property. There is a need to register and prove that the IP belongs to India. It will encourage small companies to register the IP and leverage the Indian IP even when they are selling abroad.

Is there enough clarity exist on process and enplanement etc.?

Ashish feels the policy has already prescribed setting up of an empowered committee who will look at these aspects and it is MeitY that will be responsible for doing this.

Ashish further also elaborated that this Policy will get further push once some companies start getting empanelled and processes and rules are framed under MeitY by the empowered committee.

In concluding remarks, both Ashish and Mohan felt that Cybersecurity ecosystem will get a boost by this policy as the policy is furthering the cause by advising Government departments for preferring Indian products. With Digital economy on anvil, there should be a huge demand in Government and Public sector enterprises for cybersecurity. Cybersecurity product market is today dominated by players from the US, Europe and Israel.

The policy has to be pushed hard to further encourage and coupled with StartupIndia policy, there should be all-out effort to promote the Indian Cybersecurity product companies.

Here are concerns and curiosity about European Union General Data Protection Regime (GDPR) and there is a related issue in India being covered under Data Empowerment and Protection Architecture (DEPA) layer of India Stack being vigorously followed at iSPIRT.

iSPIRT organised a Policy Hacks session on these issues with Supratim Chakraborty (Data Privacy and Protection expert from Khaitan & Co.), Sanjay Khan Nagra (Core Volunteer at iSPIRT and M&A / corporate expert from Khaitan & Co) and Siddharth Shetty (Leading the DEPA initiative at iSPIRT).

Sanjay Khan interacted with both Siddharth and Supratim posing questions on behalf of Industry.

A video of the discussion is posted here below. Also, the main text of discussion is given below. We recommend to watch and listen to the video.

GDPR essentially is a regulation in EU law on data protection and privacy for all individuals within the European Union. It also addresses the export of personal data outside the EU.

Since it affects all companies having any business to consumer/people/individual interface in European Union, it will be important to understand this legal framework that sets guidelines for the collection and processing of personal information of individuals within the European Union (EU).

Supratim mentioned in the talk that GDPR is mentioned on following main principles.

Harmonize law across EU

Keep pace with technological changes happening

Free flow of information across EU territory

To give back control to Individual about their personal data

Siddharth explained DEPA initiative of iSPIRT. He mentioned that Data Protection is as important as Data empowerment. What this means is that individual has the ability to share personal data based on one’s choice to have access to services, such as financial services, healthcare etc. DEPA deal with consent layer of India Stack.

This will help service providers like account aggregators in building a digital economy with sufficient control of privacy concerns of the data. DEPA essentially is about building systems so that individual or consumer level individual is able to share data in a protected manner with service provider for specified use, specified time etc. In a sense, it addresses the concern of privacy with the use of a technology architecture.

DEPA is being pursued India and has nothing to do with EU or other countries at present.

Sanjay Khan poses a relevant question if GDPR is applicable even on merely having a website that is accessible of usable from EU?

Supratim explains, GDPR applicable, if there is involvement of personal data of the Data subjects in EU. Primarily GDPR gets triggered in three cases

You have an entity in EU,

You are providing Goods and services to EU data subjects whether paid for or not and

If you are tracking EU data subjects.

Many people come in the third category. The third category will especially apply to those websites where it is proved that EU is a target territory e.g. websites in one of the European languages, payment gateway integration to enable payments in EU currency etc.

What should one do?

Supratim, further explains that the important and toughest task is data management with respect to personal data. How it came? where all it is lying? where is it going? who can access? Once you understand this map, then it is easier to handle. For example, a mailing list may be built up based on business cards that one may have been collected in business conferences, but no one keeps a track of these sources of collections. By not being able to segregate data, one misses the opportunity of sending even legitimate mailers.

Is a data subject receives and gets annoyed with an obnoxious email in a ‘subject’ that has nothing do with the data subject, the sender of email may enter into the real problem.

Siddharth mentioned that some companies are providing product and services in EU through a local entity are shutting shops.

Supratim, mentions that taking a proper explicit and informed consent in case of email as mentioned GDPR is a much better way to handle. He emphasised the earlier point of Data mapping mentioned above, on a question by Sanjay khan. Data mapping, one has to define GDPR compliant policies.

EU data subjects have several rights, edit date, port data, erase data, restrict data etc. GDRP has to be practised with actually having these rights enabled and policies and processed rolled out around them. There is no one template of the GDPR compliant policies.

Data governance will become extremely important in GDPR context, added Siddharth. Supratim added that having a Data Protection officer or an EU representative may be required as we go along in future based upon the complexity of data and business needs.

Can it be enforced on companies sitting in India? In absence of treaties, it may not be directly enforceable on Indian companies. However, for companies having EU linkages, it may be a top-down effect if the controller of a company is sitting there.

Sanjay asked, how about companies having US presence and doing business in EU. Supratim’s answer was yes these are the companies sitting on the fence.

How about B2B interactions? Will official emails also be treated as personal? Supratim answers yes it may. Again it has to be backed by avenues where data was collected and legitimate use. Supratim further mentions that several aspects of the law are still evolving and idea at present is to take a conservative view.

Right now it is important to start the journey of complying with GDPR, and follow the earlier raised points of data mapping, start defining policy and processes and evolve. In due course, there will be more clarity. And if you are starting a journey to comply with GDPR, you will further be ready to comply with Indian privacy law and other global legal frameworks.

“There is no denying the fact that one should start working on GDPR”, said Sanjay. “Sooner the better”, added Supratim.

We will be covering more issues on Data Protection and Privacy law in near future.

Author note and Disclaimer: PolicyHacks, and publications thereunder, are intended to provide a very basic understanding of legal/policy issues that impact Software Product Industry and the startups in the eco-system. PolicyHacks, therefore, do not necessarily set out views of subject matter experts, and should under no circumstances be substituted for legal advice, which, of course, requires a detailed analysis of the relevant fact situation and applicable laws by experts in the subject matter on the case to case basis.

GST regime has brought a new dimension to treatment of Indirect taxation in Exports.

Prior to GST era, the export invoice had no Indirect tax mentions. So also, the indirect tax returns had nothing to do with Exports.

After GST implementation, to make the GST truly value added and consumption-based tax a concept of Zero-Rate supply was introduced. This made it necessary for exporters to account for indirect tax (GST) at time of exports.

An exporter has to adopt either of the two below given methods.

Export with IGST Paid – include and pay IGST at time of export to Govt. on invoice value and later get refund or

Export under LUT without payment of IGST – File a letter of Undertaking (LUT) with GST department and raise zero IGST export invoices and get refund of GST paid on inputs at later date.

Note: Before October 2017 there was also a requirement to sign a Bond (backed by bank Guarantee) if the value of exports for an enterprise in previous years were less than Rs. 1 Crore and sign a LUT if previous year exports were more than Rs. 1 crore. The requirement to sign a BOND has been done away with and all the BONDS signed until October 2017 will be treated as LUT, format and paper work being almost similar.

As working capital gets blocked if the IGST route is adopted (exporter pays IGST and then file for refund again and again on each billing cycle), not many may have adopted this route. Hence, A good number of Software exporters filed Bonds or LUTs with GST department early at start of GST regime.

The tax refunds can be claimed every month. However, for most small exporters it may be useful to file tax refund claims once at end of financial year. This will keep administrative burden low and also the cost of tax management low, while seeing a handsome refund amount in one go.

This write-up is meant to simplify issues of GST refund in exports for entrepreneurs i startups including SaaS and Software products.

Why is refund applicable on Exports?

First thing to understand is that under GST regime (unlike previous VAT and service tax) exports and imports are subject to IGST (in lieu of CGST+SGST), which is a tax applicable on Inter-state supplies. GST law treats exports and imports at par with inter-state trade to make exporters account for IGST.

Second thing to understand is whereas exports are covered under IGST (inter-state supplies), the exports are treated as “Zero Rates” supplies i.e. such supplies will have zero indirect tax incidence finally. The tax incidence of Indirect tax is normally on the final consumer of goods and services. Since, in exports the final consumer of goods or services is located outside India, the consumption happens outside the country. To maintain competitiveness of exports from country and to align with tariff structures in place before GST implementation, the indirect tax has to be zero (excepting a list of goods that are subject to tax). The exports and supplies to SEZ (deemed exports) have been treated as Zero-rate supplies.

Third thing to understand is the GST is a value added tax. This can be understood from old VAT regime, also. A supply of goods or service when passes from original manufacturer to end consumer through various trading channels, it’s value increases at every point. If A sales a good for Rs. 100 and charges GST of Rs. 18 the cost becomes Rs.118 to B, now B may sale same at Rs. 125 to C the final consumer. The GST will now be Rs. 22.5 and final cost to C will be Rs. 147.50. B however gets an input credit of Rs. 18 and pays Rs. 4.5 tax (Rs. 22.5- Rs. 18).

Now, if B is an exporter and C is a client abroad, B has an option to adopt one of the two routes described above.

Route 1 – B can raise an export invoice with IGST paid of Rs. 22.5. Client C is charged Rs. 125 (in equivalent foreign currency) but IGST of 22.5 is paid to GST department in India. B then files for a claim of entire GST amount of Rs. 22.5.

Route 2 – B can file a LUT with GST department and raise an invoice with IGST zero and Rs. 125 (in equivalent foreign currency). Now either at month end or within a period of 2 years B can ask for refund of IGST that B has paid when procuring supplies from A of Rs. 18. This Rs. 18 is called unutilised input credit.

Refund of unutilised input is available as the final goods are consumer by client C in foreign territory and C is not subject to payment of indirect tax. Hence the tax accumulated by exporter B from his previous suppliers (can’t be born by the exporter) and should be refunded.

Had the consumer C been in domestic tariff area i.e. within the territory of India, the final value added tax on supplies would have been born by the consumer.

An exporter can claim unutilized input credit on all the inputs required in production of final product or service exported.

How can exporters claim utilised tax credit (GST) refund?

As per Section 54(3) of the CGST Act, 2017, refund can be claim of unutilised input tax credit can be done at the end of any tax period (tax return period) i.e. a taxpayer can claim refund on monthly basis.

As per the provisions of GST Law, Refunds to be granted to the dealer electronically on the basis of application in RFD-01. However, due to the non-availability online process, as per notification No.39/2017-Central Tax, dt. 13-10-2017 exporters can file manual refund claims to the jurisdictional officers.

A New form RFD-01A introduced to be filed manually by the exporters to facilitate early Refunds vide Circular no.17/2017 dated 15-11-2017.

For those adopting IGST paid route, the processes is more simpler and 90% of tax is supposed refunded within 7 days of filing. This writeup assume most exports barring petty exporters have adopted LUT route.

This write-up is not meant to describe a detailed process, but highlight the need to file for refunds by exporters if not filed yet, instead of letting the input tax credit to be passed on to next year. This will help channelize funds recouped in to business cycle for next year.

In order to file for refund an exporter needs to have filed all required returns on GST portal and should have records of all purchase invoices, export invoices raised, and the bank certificates of remittances received against export invoices.

For those who are suppling to Special economic Zones (SEZs) the process is similar to exports, except there will be documents and certification to be sought from SEZ units and local jurisdictional officer.

As the financial year end closes, all such exporters who have filed a LUT or BOND should be gearing up to seek GST refunds, if not done already.

GST regime started with lot of confusion for small exporter. Many issues have been resolved and many are yet to be resolved. GST is a much better regime in terms of taxation. However, a fully featured matured and fully digital GST regime will be much more beneficial for exporters. We hope in next financial year we can see roll out of a fully digital GST with near zero interference from officials and manual applications.

Every year we have two events in financial year end which attracts every one right from Industry, Agriculture to common man of this country. These are annual budget of Govt. of India and preceding the budget the Economic survey. The Chief economic adviser who keeps an eye on the Economy of the country round the year and advises the Govt. on right policy formulation, presents the Economic Survey year, which is both the stock of performance of the Economy as well as a guide to investigate future, especially setting the thought process for the budget.

This year’s Economic survey was very important from the perspective of having come after two consecutive events in short term, the Demonetization effect + GST. This year’s economic survey also moved ahead from “digital economy” theme. The word digital finds only a lip service in certain places in volume II.

The information technology sector has been an important sector of Indian economy for last 2 decades. This write up is a synopsis view of how Economic survey has projected the performance of this sector vis-à-vis the rest of economy.

On overall terms, Chief Economic Advisor(CEA) is very optimistic and has projected a 7+% growth in GDP in next one-year time frame. He has rightly quoted the positive indicators from International rating agencies of Moody’s upgrade of India’s ranking and a jump in world banks ranking on Ease of doing business.

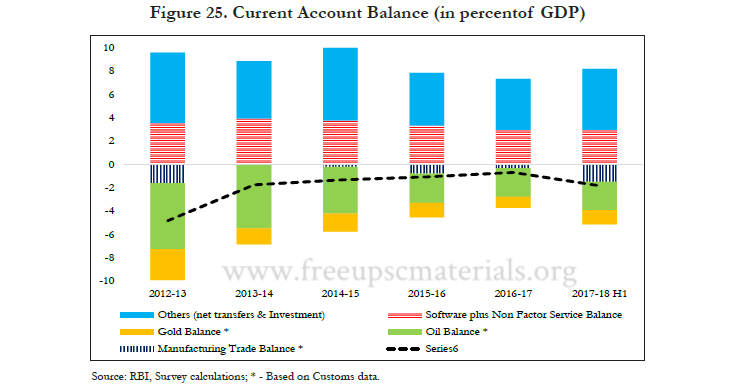

The “Software” and IT is covered under “services” as the balance of payment accounting accounts “Software” under services and non-factor services balance. This accounting entry in current account balance has consistently performed for years for India. The following chart is self-explanatory on this.

Almost every Government record uses the terminology IT-BPM to aggregate both IT services and ITeS exports. Software forms part of IT exports and it is difficult to estimate the Software product exports in this category as it includes mix of various reporting.

In India there are two sources of data for Software exports. One from a RBI data based on remittances reported under specified codes and secondly from data and analysis reported by NASSCOM, STPI and Jurisdictional SEZ commissioners.

The interesting difference in this year’s Economic survey is the data reported by RBI and NASSCOM is in two different directions. Usually both do not match. This year RBI reported a negative (-)0.7% in 2016-17 growth in exports, whereas NASSCOM registered a 7.6% growth in exports.

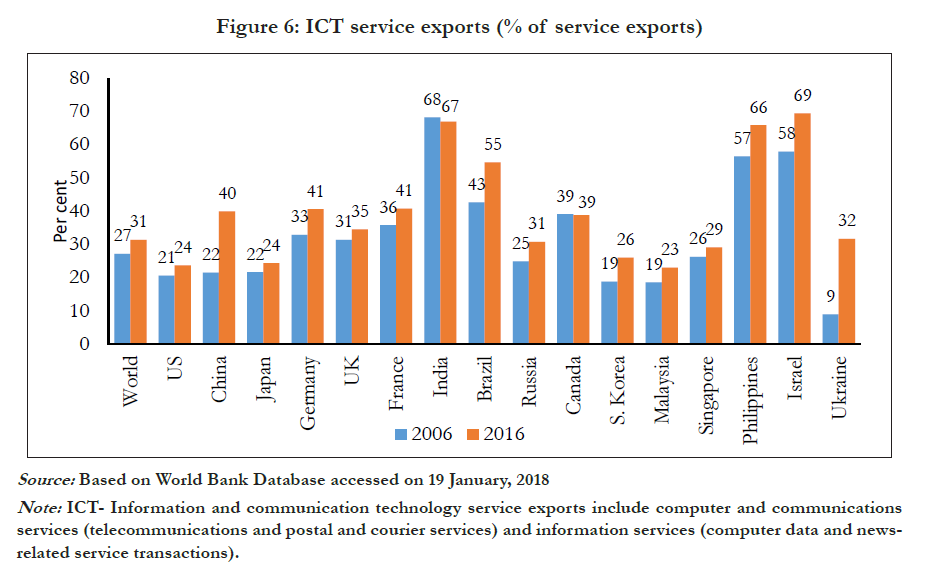

Another interesting chart from economic survey reporting from this sector is a report from world bank data base. The chart given below depicts that India, Israel and Philippines as top players in ICT exports to the world. It is common knowledge that Israel’s exports are based on their competitive advantage in Software products, India in IT Services and Philippines in BPO. Israel a small country export levels using product as a base are higher than India’s in IT services. It goes without saying that India needs to shift its strategy in the sector and give emphasis to products in its ICT portfolio.

FDI inception in the sector can not be estimated separately from given data. However, FDI in overall services sector (of top 10 service sector) had a share of 65.8%. in April-October 2017-18.

The survey also reported a robust growth of services sector to 16.2% in April-September 2017 owning to major sectors like travel and Software.

Software services share was 45.2% of overall services exports in 2016-17. (The software however in report means complete IT sector).

GST in Economic Survey

On fiscal policy side, GST is a new entrant in the system. GST also treats every thing that is intangible in IT as service be it is a IT Service or a Software product. As per CEA there is a 50% increase in registration of tax payers after GST introduction. This is a healthy sign for the economy and for digital transformation of economy.

With indirect tax on Software having risen from 15% to 18% there will be a larger gross value addition in Domestic market by the Software sector. Plus, increased digital adoption is expected to boost the overall domestic trade in this sector.

GST system also effects how exports are done. On export front discounting the initial difficulties exporters had, GST is expected to ease the compliance on export front as well as complexities that affected many on Place of supply/provision of services rule.

Other general announcements on Exports

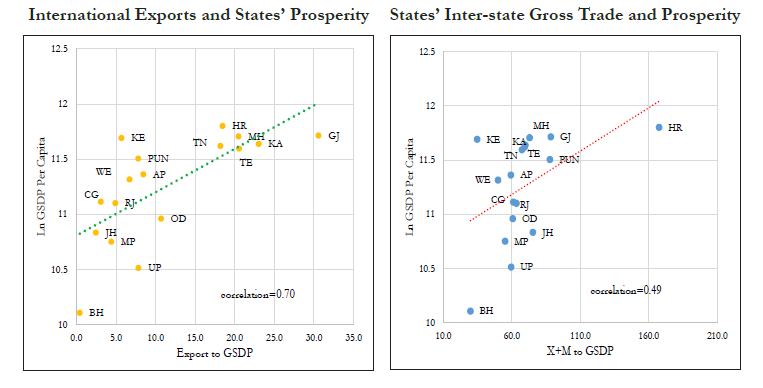

Many of the India’s states are much larger than some developed countries. However, it is for first time that a comparison or detailed data on the international exports of states has been included. Also this data shows a strong correlation between export performance of states and their standard of living and affluence.

A figure from Economic survey is reproduced below.

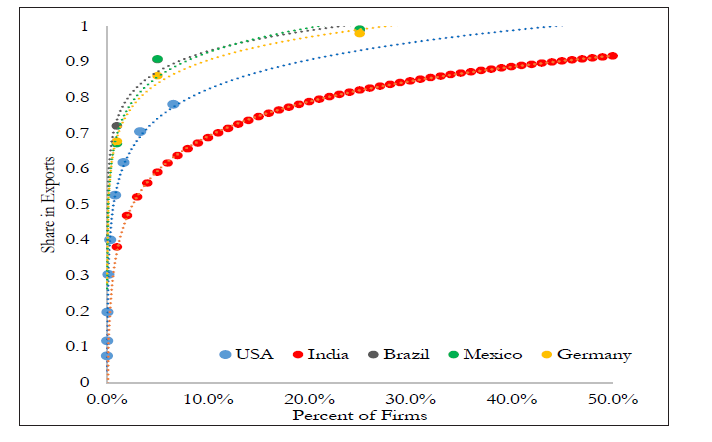

IT is said that there is no super star exporters in India. According to survey, top 1 percent of Indian firms account for 38 percent of exports; in all other countries, they account for a substantially greater share (72, 68, 67, and 55 percent of exports in Brazil, Germany, Mexico, and USA respectively). And this is true for the top 5 percent, 10 percent, and so on.

This analogy also helps us undertand that in IT sector also there is no superstar that is ruling the globe in international trade from India. Rather in IT the spread is much wider and open. India needs to build a Google is the dream that remains to be realised for this sector, to be a true Software power.

A chat below explains this in the survey.

Conclusion

There is a clear cut challenge on economic front for IT sectors. The share of IT exports in total Services export has also been going down for last few years. Survey says Govt. is taking several steps to boost this. However, the reality is that government has yet to take right steps in changing world scenario both to boost the exports as well as growth of domestic IT industry.

Government has failed to recognize formation of a sub-sector of SaaS products and bring up new programs and schemes for promotion of Software product as a sector with in IT. iSPIRT has been continuously working to influence the policy makers to come up with a Software Product policy which can lead to announcement of a Scheme for SaaS companies and boost morals of Indian Startup entrepreneurs to stay in India and run global business from India.

With this background now we look forward for a Budget 2018.

iSPIRT has taken up a checklist of issues to be resolved for helping Startups stop relocating themselves abroad and stay in India, popularly called as Stay-In-India Checklist. These were taken up with Department of Industrial Policy and Promotion (DIPP) under Ministry of Commerce, Government of India. DIPP is also the administrative department for Startup India Policy.

There are a number of issues that have been resolved, till today.

A list of eight issues that have been resolved until now that directly effects the Startups on company law or their promotion and ease of doing business are given below.

1. IPR Registration

A scheme for promoting IPR awareness has been brought out by DIPP with an objective of promoting IP awareness, conduct workshops and training to enable an innovation-driven environment. The details of the scheme are given on DIPP site like here.

2. Conversion process of LLP into company

Conversion of an LLP into a company was allowed with an amendment to Section 366 of the Companies Act, 2013, as notified on 1 April 2014. This has further been simplified by bringing down threshold of member from 7 members to 2 members. Please refer to the amendment in section 266 of THE COMPANIES (AMENDMENT) ACT, 2017, published on 3rd January 2018. Refer the link http://www.mca.gov.in/Ministry/pdf/CAAct2017_05012018.pdf

3. Incorporation process to be simplified

Rule 38 of Companies (Incorporation) Rules, 2014 provides for SPICe (Simplified Proforma for Incorporating Company electronically) form for incorporating a company. This is considered to be a welcome step as this simplified procedure would save the time of incorporation of a company.

The Fourth amendment rules notified on 1st October 2016 and Fifth amendment notified on 29 Dec 2016 came in to force from 1st January 2017 provides for much simpler SPICe form, now known as E-Form SPICe (Form INC-32).

SPICe now integrates into single application – reservation of name, allotment of Directors Identification Number (DIN). It can be filled without having DIN already, by maximum three directors.

The company is allotted Permanent Account Number (PAN) and Tax Deduction Account Number (TAN) and Certificate of Incorporation (CIN) on completion of form and processing by ROC. The PAN number is printed on CIN.

MCA has notified Section 234 of the Companies Act 2013 (2013 Act) which permits cross-border mergers with effect from 13 April 2017. MCA has also notified relating amendments to the Companies (Compromises, Arrangements and Amalgamations) Rules 2016 (Merger Rules) by inserting a new Rule 25A to be effective on and from 13 April 2017.

The provisions now permit cross-border mergers both ways.

Inbound – Foreign company merging into Indian company

Outbound – Indian company merge into a foreign company.

This will help the intra-group situations and also open opportunities to raise capital, diversify ownership base and achieve other strategic objectives

5. Regulation on Insider trading on private companies

Section 195 of the Companies Act, 2013 has been omitted by way of Companies (Amendment) Act, 2017 as it was deemed that the SEBI regulations on the same are wide enough to cover such instances. Currently, there is no provision under the Companies Act, 2013 which deals with insider trading in private companies

6. Regulations governing TDS to be rationalized

Thresholds limits for TDS deductions under various sections has been increased and also the rate of tax rationalized in some cases in the Budget 2016. We may see some more changes coming in future.

7. Single window agency for closure of failed startups

The Insolvency and Bankruptcy Code 2016, is a single legislation clubbing together the processes for resolution or liquidation of corporate persons.

Sec 12 of the Insolvency and Bankruptcy Code, 2016 provides for closure of failed startups within 180 days, which can be extended by another 90 days.

This provision removes the hindrance of long drawn procedures and timelines when it comes to the closure of such failed startups by capping the process at 180 days.

8. External commercial borrowing guidelines to be relaxed

A startup can borrow up to US$ 3 million or equivalent per financial year under ECB framework, either in Indian rupee or any convertible foreign currency or a combination of both. In case of borrowing in INR, the non-resident lender should mobilize INR through swaps/outright sale undertaken through an AD Category-I bank in India.

iSPIRT will be further pursuing with DIPP and other Departments and Ministries of Govt. of India on the additional items in Ease of Doing Business for starts ups and furthering its agenda of Stay in India.

The GST was welcomed by all as a revolutionary measure. We had covered one earlier topic, “How GST will work for software exporters”. There have been many changes in last few weeks before GST was launched in the IGST law.

Please note that “GST law” treats Software as “Service”. Hence, there may be a mention on “Software” and “Services” in mixed manner in the write-up. This write-up is just focusing on problems and issues created for exporters by the GST process. On details of process there are many blogs on internet.

After launch of GST since 1st July 2017, we came across many questions and concerns on how GST on Exports. I have been trying to write a piece on how the process works for Software exports under GST. However, the policy and process for export of “Services” was not at all clear. I have myself struggled through, and it has taken more than 6 weeks to understand the process, raise exports invoices and multiple documentations required.

GST has turned out to be nightmare, especially for Small and medium Software exporters and will continue to do so, unless corrective measures are taken up.

Let us look into how process required to be complied, caused problems.

Exporting Software under IGST law

IGST law on one hand treats exports as “Zero-rated” supplies and on the other hand treats exports as “inter-state” trade instead of “International trade”. These two corollaries of GST law are inherently paradoxical.

Being Zero-rated there is no tax or duty on export. However, being Inter-state trade (rather than being international trade) it requires payment of IGST under IGST law.

If one delves deep in to this application of IGST on exports, it clearly comes from concern of tax policy makers on “Goods”, moving in a container and a compliance assuring good reach port of export and gets exported finally. That this does not apply to services has not been thought over by the GST law makers. (the assumption may be services will adjust in due course of time)

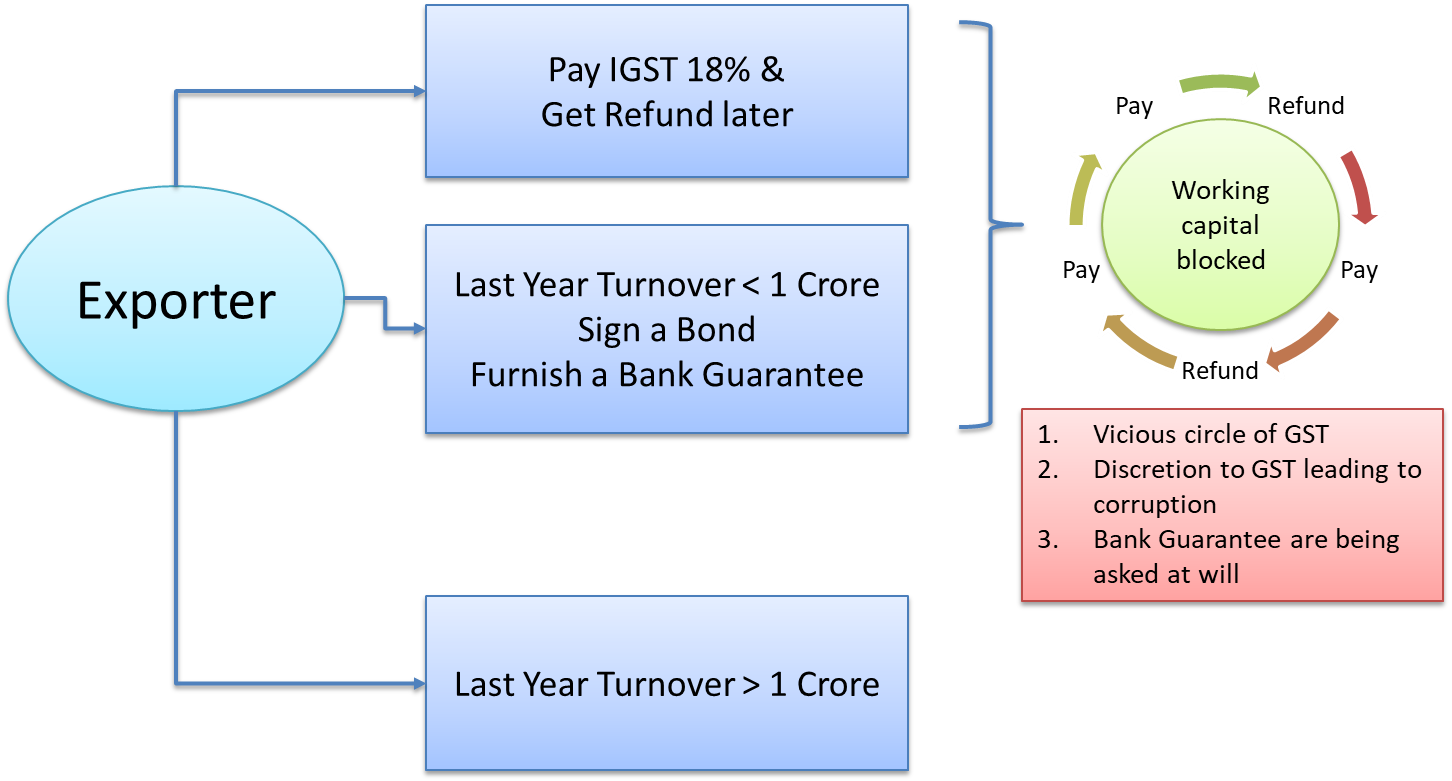

Hence, as per IGST law an exporter is required to either

Pay IGST 18% on Software export and get it refunded

Or Export without IGST by

Filing a Bond if the exports in previous year were less than rupees one crore.

Filing a LUT if the exports in previous year were more than rupees one crore.

Filing a Bond requires submitting a Bank Guarantee to GST department up to 15% of the amount of duty applicable on estimated exports value in a given (say a year). The jurisdictional office of GST has a discretion to decide bank guarantee amount anywhere from Zero to 15%.

If the office approves zero % (or nil) bank Guarantee, the department asks a set of declarations and data of past year.

Anything that is based on discretion in regulation, also brings in corruption with it. Whereas there is news from many places that jurisdictional GST office are waving bank guarantee clause for Software/IT exports. There is also news that GST department is randomly asking for bank guarantees.

Problems created by IGST law

Locking of working capital

A small software exporter or a startup not having more than 1 crore of “export turnover” in past year will have to opt for either option a) Or b) from above choices i.e. either the exporter has to pay duty and get a refund or has to sign a bond with bank guarantee.

If the bank guarantee is not waved by the jurisdictional officer, the exporter will have to keep the bank guarantee replenished continuously to support regular exports.

In either of the cases the IGST law locks the working Capital of the start-up or small exporter.

The GST law therefore goes against policy of Government of India to promote startups. It also is going to be regressive measure for large number of small IT companies, IT consultants and freelancers.

Discretion causes corruption on ground

Anything that is based on discretion in regulation, also brings in corruption with it. For those who want to file bond, the jurisdictional office of GST has a discretion to decide bank guarantee amount anywhere from Zero to 15%.

Whereas there is news from many places that jurisdictional GST office are waving bank guarantee clause for Software/IT exports. There is also news that GST department is randomly asking for bank guarantees.

GST department’s manual intervention in Exports

Exports before GST were never allowed to report or get clearance from Indirect tax departments. Now, GST department has become a gateway for every exporter of Goods and Services, thus extending mandate from domestic tariff area to international trade also.

What is cause of concern is this intervention of GST department is manual as against the principle of making entire GST system end-to-end digital. This give power in hands of indirect tax officers to monitor exports.

This perhaps is a fundamental error that Government of India have made, against it’s public stance on “Ease of doing business.”

This is a problem for all exporters including those with “export turnover” more than 1 crore and eligible to sign a LUT with GST.

It is more of less like traffic policing the exports on regular basis and heavily increased compliance.

GST has no focus on Software exports

The entire GST law has been written with physical Goods in mind but applied equally to both Goods and Services. Once again Government of India has made a classical mistake. It is an irony that a nation that is known to be power house of Software has not focus of tax authorities on “Software exports”.

The concept of Bank-Guarantee is detrimental to Startup eco-system and SMEs

Startups and SMEs require removal of regulatory barriers for them to grow. GST law has done just the opposite. It requires small exporters and Startups to furnish Bank Guarantees.

GST for supplying to SEZ

SEZs are deemed to be considered outside the customs territory of India. Hence, supplies to SEZ units by exporters in India i.e. DTA will be treated in same manner as exports to clients located outside the country.

Therefore, if a Startup or a Software product company is selling to an SEZ unit, the process will be same as that of exporting.

Conclusions and Recommendations

Government of India has seriously lost focus on “Ease of doing business” agenda, startup policy, SMEs and supporting self-employed professionals while framing GST/IGST laws.

It is recommended that

Government of India should notify a clearly stated policy for Services and Software exports and not mix or generalize with remaining Goods exports.

The GST department should have no or minimum (limited to Digital medium) only in regulating exports of Services and Software

IGST duty and refund mechanism and also Bank-Guarantee or LUT should be done away for Services and Software export. A quarterly and annual reports is enough on digital platform, regulated digitally. In order to bring or include Services exporter under DGFT regulation, IEC can be made mandatory and used to regulate Services trade. IEC is same as PAN now, hence, IEC can be used by all size of exporters.

‘SaaS’ can drive the future of Indian IT Industry both in International trade as well as domestic front. With changing dynamics in Software sector globally, ‘SaaS’ can help India remain a Software power house. iSPIRT has been following ‘SaaS’ industry growth from this perspective. The realization that there are several policy hurdles for ‘SaaS’ industry was very early conceived at iSPIRT.

Accordingly, iSPIRT made several attempts to ease the problems of ‘SaaS’ industry. One of the belief at iSPIRT is that ‘SaaS’ is basically about ‘product’ first and then a ‘service’. With this belief iSPIRT has been continuously taking up the case of clear distinction of Software product within the larger framework of Digital economy consisting of “Digital goods” and “Digital services”.

In order to stop the exodus of Startups, which constitutes a large number of ‘SaaS’ based startups, a Stay-in-India checklist was taken up with Department of Industrial Policy and Promotion (DIPP). There have been a number of items cleared by DIPP such as Angle Tax, Fair market Value, ESOPs provisions made better, Company incorporation rules simplified, Domestic venture debt made easy, Convertible notes, FVCI norms relaxed and External Commercial borrowing (ECB) eased by RBI etc. Some of these announcements under the shadow of StartupIndia policy. However, iSPIRT has been continuously pushing policy makers to relax all these norms for all start-ups. iSPIRT covered most of these announcements in PolicyHacks blogs given here.

A major problem area for ‘SaaS’ startups is also the payment gateway systems. ‘SaaS’ industry has to resort to either relocate to a foreign geography, or open a subsidiary abroad or seek expensive international payment gateway services. On domestic front the ‘SaaS’ industry suffers from recurring billing problems. Both these issues were taken up in PolicyHacks sessions given here. iSPIRT believes Indian ‘SaaS’ companies should be able to carry of out international trade of digital goods without moving out of India seamlessly and using Indian payment Gateway systems.

The belief at iSPIRT that a futuristic industrial policy at Ministry of Electronics and IT (MeitY) is required to meet the challenge of Indian IT industry was followed up with a National Policy on Software Product (NPSP) at MeitY. Being the administrative ministry for this Industry MeitY has in past played highly catalytic role in making of IT industry that India is proud today. A similar renewed thrust is required to push the Indian Software Product Industry.

One of the main emphasis in NPSP draft being followed up at MeitY is the ‘‘SaaS’’ segment. iSPIRT team is continuously engaging with the MeitY officials to educate them and influence on the importance and the need to focus on ‘SaaS’ segment.

There is recognition in Government system for need of this strategic shift. Honourable Prime Minister’s speech at Germany (Link here see 12th Minutes segment) is the evident of this realization of need for change that can lead to companies like Google to be born out of India.

iSPIRT is striving hard in this direction to see the ‘SaaS’ as the next big leap by India.

GST council has yesterday cleared all the bills required to implement the GST. Finance minister wants to kick-start from July 1 2017. This can be easily achieved is the model laws can be enacted in the current session of parliament. The GST is therefore set become a reality from the second quarter of the current financial year.

GST is going to catalyze greater IT adoption. We can see the business going digital in future and a Digital India emerging.

Apart from receiving GST as a catalyst for Software product industry growth, we also need to get prepared for adopting GST our selves. Not everyone has prepared for GST though. At iSPIRT we are starting discussion group on GST so that community can take advantage from shared learning. This blog is the first in series of this effort.

Few fundamental changes in the Goods and Service tax (GST) as it is called are

It is supply based and not sales based tax system

Being an indirect tax, it applies where the consumption happens

There are three statues and taxes that are part of GST i.e. SGST (state GST), CGST (Center GST) and IGST (integrated GST = SGST+CGST)

Both state and center will get tax on Goods and services supplied unlike earlier only Center received the service tax

The GST subsumes many of the indirect taxes prevalent at present

GST will significantly change the way of doing business. Also, it is bound to greatly impact the international trade regime e.g. excise duty will merge in GST and deemed exports benefits under excise laws may come to an end. The exports aspect will impact Software exporters, irrespective of whether they are operating under SEZ, STP, EOU, EPCG or outside as these export schemes. GST on Import is going to impact every one, as in globalized world with cloud penetration, everyone is bound to use goods and services imported.

In this blog we cover in brief the application of GST on the import and export of goods and services.

How it impacts Import?

Basic custom duty (BCD) is not covered under GST and it will remain same. There will be two components on each import to be paid i.e. Basic Duty + IGST.

IGST will subsume currently applicable countervailing duty (CVD) and additional duty of customs (SAD).

Integrated Goods and Services Tax (IGST) means tax levied under this Act on the supply of any goods/services in the course of inter State trade or commerce. IGST has two components SGST and CGST. A supply of goods/services in the course of Import into the territory of India shall also be deemed to be a supply of goods/services in the course of inter-state trade or commerce.

The levy of IGST will be payable for each transaction, as against the monthly payment in case of IGST payable on domestic interstate transactions.

The other difference in GST is aboput IGST computation. The IGST will be computed on transaction value of imported goods plus duties and taxes etc. charged under any statute other than the GST Law. Hence, ISGT will be applied on total landed value, basic customs duty and any other charges.

On import of services GST will be based on reverse charge method just as the Service tax is today i.e. IGST will apply on reverse charge mechanism. Hence, all Software or a SaaS bought online will be subject to reverse charge basis IGST.

But there is a input credit allowed in ISGT on imports. The service provider, trader or manufacturer of imported goods/services shall be eligible to offset IGST paid on import of goods/services against his output liability. The same does not apply to BCD as BCD is not part of GST.

Although it does not apply to Software sector, the anti-dumping duties and safeguard duties will continue to be applied as they were and have not been subsumed in the IGST.

Impact on exports

Exports under GST will be Zero rated i.e. there will not be any exports duty except on items that enjoy an export duty levy currently. Software exports will be zero rated.

The biggest impact will be on units presently enjoying exemptions on inputs like service tax in SEZ. Under GST all duties and taxes will be payable at the time of a transaction when procuring input goods/service and the exporter can get refund for these after exporting. Exemptions will be replaced by refunds after exports.

This will put lot of burden on arranging working capital for the inputs. This burden will be higher for manufacturing firms than services firms.

On pursuance of commerce ministry, in a recent announcement, the finance ministry has agreed to relax the refund pains. The finance ministry has agreed to refund 90% of the duties paid by exporters within a period of seven days under the Goods and Services Tax (GST) regime. If duty refunds could not be made within seven days, then government will pay interest to exporters. However, it is yet to be decided how much interest will be paid to exporters in such a scenario, as per announcement. (Source: livemint news item)

The remaining 10% refund will be made after verification by tax authorities.

This is a bit of relief to exporters. Compliance process will change from presently exemption based compliance to a refund claim filing in time. The crux here is to use digital technology to automate many of these issues in GSTN.

Whereas these announcements have been made, the details will depend upon how rules are notified.

GST will undoubtedly make the efficient in long run. However, the next one year will be full of challenges and adjustments by Ministry of finance to oversee a smooth rollout.

Should you have further questions on GST, please write to[email protected]

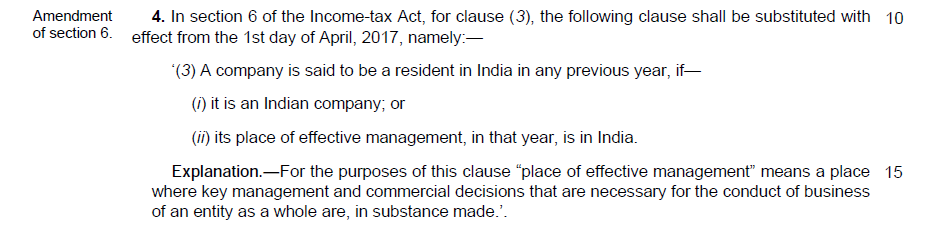

Finance minister had announced during budget 2016 that place of effective management (POEM) will determine if a company is resident in India or not. Accordingly, this was notified in Finance ACT 2016 as under.

The details of what will determine the place of business rules was not decided in the Finance Act 2016. The POEM provisions was supposed to become effective from April 2017. The detailed guidelines of what rules and conditions will determine the POEM has been issued by CBDT on 24 January 2017.

Ever since the announcement in 2016 there were many apprehensions on POEM, especially in SaaS companies.

In order to clear this apprehension a PolicyHacks session of iSPIRT was conducted.

The video discussion on POEM attended by Girish Rowjee, Founder CEO of Greytrip; Mrigank, Mrigank Tripathi, Founder CEO of Qustn Technologies; Sanjay Khan Nagra, of Khaitan and Co.; Avinash Raghava and Sudhir Singh, iSPIRT is given below.

What does the above POEM ruling incorporate in finance bill imply?

In simple terms the place of effective management in above act means a place where key management or commercial decisions that are necessary for the conduct of the business of an entity are made, in substance. This implies Indian resident status on a company will apply even when the entity is incorporated outside India, if the place of effective management is proven to be in India.

The guidelines issued on 24th January 2017 by CBDT will be used to determine if a business of non-Indian entity or a subsidiary of Indian entity will fall under the place of business rules or not. The Guide lines can be accessed here.

POEM is an internationally recognised test for determination of residence of a company incorporated in a foreign jurisdiction.

Why this regulation has been brought in?

POEM require Indian firms with overseas subsidiaries or foreign companies in India to pay local taxes based on where the business is effectively controlled.

The main intention of this regulation is to capture the income in shell companies incorporated outside India that are held by resident Indians with a basic intention of retaining the income outside India.

The regulation is not intended to discourage valid Indian businesses to setup an entity outside India or operate in global markets.

Does it impact Software sector?

It is very common for the India Software companies to open an office in foreign geography, many times as a subsidiary of Indian company and sometimes a new entity with mixed local and Indian management. Hence, the POEM has been worrying entrepreneurs in this sector. For SaaS segment, it is very normal to have a foreign entity, either for reasons of funding or market penetration.

As mentioned above, for a valid global business the POEM will not be a hurdle. Businesses, having global operation but not retaining income in foreign companies (i.e repatriating profits to Indian company) through authorised route and after complying with other regulations, POEM will not be a a worrying factor.

There may be a very few Software Companies, who may need to be concerned, to pass the test of POEM. Any determination of the POEM will depend upon the facts and circumstances of a given case. The POEM concept is one of substance over form. If POEM is established to be in India for businesses operating outside India, they will be taxed in India.

It is not possible to generalize the impact of POEM on Software sector or illustrate few used cases. Whether a business operating outside India will get classified as POEM can only be ascertained after detailed examination.

Exemption for turnover less than 50 Crore

There is good news for startups as per the Press release accessible here, it has been decided that the POEM guidelines shall not apply to companies having turnover or gross receipts of Rs. 50 crore or less in a financial year.

This was not clear before video discussion and doubts were expressed during discussion, as this rule has not been described in the guideline circular of CBDT but has been mentioned in the press release of same date from CBDT.

Hence, we can expect that the rule of less than 50 crore income shall be embedded in income tax rules to be notified later.

Other salient features

The provision would be effective from 1st April 2017 and will apply to Assessment Year 2017-18 and subsequent assessment years.

The Assessing Officer (AO) shall, before initiating any proceedings for holding a company incorporated outside India, on the basis of its POEM, as being resident in India, seek prior approval of the Principal Commissioner or the Commissioner, as the case may be.

Further, in case the AO proposes to hold a company incorporated outside India, on the basis of its POEM, as being resident in India then any such finding shall be given by the AO after seeking prior approval of the collegium of three members consisting of the Principal Commissioners or the Commissioners, as the case may be, to be constituted by the Principal Chief Commissioner of the region concerned, in this regard. The collegium so constituted shall provide an opportunity of being heard to the company before issuing any directions in the matter.

The point 2 and 3 mentioned above will ascertain that there is no arbitrary discretion exercised by Assessing officers on ground.

The Guidelines issued can be accessed here, also provides examples that explains when an active business outside India will be treated as Indian business based on POEM. These examples do not explain each and every case.

Also the exemption of 50 Crore is neither given in Finance Act or in the Guidelines but mentioned in press release.

CBDT may therefore issue further circulars to clarify these positions.

[An immediate official iSPIRT response to the budget was issued as a Press release on 1st FEB 2017. It is placed in media section. You can access it here.]

Budget can’t be construed as main stream policy making exercise. Yet, the policy analysts and experts, track it with utmost seriousness, to understand Government’s thought process in economic policy. Similarly, industry looks in to budget for the sectoral emphasis, allocations that will influence the demand/ supply, reforms and special provisions in the sector. A reminiscent of this in recent period of history is 2012-13 budget speech of then finance minister Pranab Mukherjee, when analysts were counting how many times he used “inclusive growth” as a phrase.

This budget speech was unique in many sense and very tactical. The proposed GST regime, the rigours of demonization and skepticism of coming state elections have all effected this budget. The usual rigmarole by media of comparing prices of commodities and consumer goods from cigarettes, electronics to automobiles is missing. GST being in pipeline, the indirect tax section, which was usually the largest section of finance bill is almost missing. Hence, allocation of resources and the direct taxes had all the share of FM’s mind in budget. The new item on the block is “Digital economy”.

We have been seeking attention of Government on:

increasing domestic demand,

promote innovation (Startups)

ease of doing business and

level playing field for Indian companies.

These four parameters impact our “product nation” focus. Let us briefly analyse how these have been taken care in the budget.

Influencing Domestic Demand function

The usual model of a demand stimulating economic policy has been based on consumption led demand relying mainly on sops and taxes for several years with doses of investment driven demand and growth from time to time.

Increased efficiency, transparency, formalization of economy and investment driven growth are four major thoughts embedded in this budget. The former three are additional determinants of demand function of emerging new economies and a means to achieving developmental agenda. Relying mainly on investment driven demand and growth is very need of the time of low sentiments.

A big measure towards increased efficiency is the change from plan and non-plan classification of expenditure. “This will give us a holistic view of allocations for sectors and ministries. This would facilitate optimal allocation of resources”, said the FM in speech.

The agriculture and rural sector of India cannot be ignored by any Govt. Hence, increased focus in budget on these two important sectors is about inclusive growth, and also in “Digital economy” perspective an attempt to avoid a digital divide.

Both continual emphasis on infrastructure investment and targeting doubling farmer income will provide an investment driven demand push and a consumption driven demand function at higher level.

What is most heartening on domestic demand side for ICT sector is the huge recognition of the “Digital Economy” in the budget. For past some years iSPIRT has been pursuing the “Digital economy” agenda at various forums. There was cautious optimism, but not full acceptability. Thanks to demonetization, “Digital” is now a mainstream concept.

Devoting a full section in his speech on “Digital economy” and dealing with it in ‘direct tax’ provisions speaks a volumes of the mind share this has taken at top in the present Govt. The finance minister stated in his speech, “Promotion of a digital economy is an integral part of Government’s strategy.”

Further, the finance minister said, “Government will consider and work with various stakeholders for early implementation of the interim recommendations of the Committee of Chief Ministers on digital transactions.” This is especially important for iSPIRT as Nandan Nilekani and Sharad Sharma of iSPIRT are special invitees on this committee.

The demand conditions for ICT sector can best be boosted by increased adoption of the ICT by masses and the businesses, especially the SME businesses. This throws open a number of opportunities for many new startups to emerge and contribute to the development of an ecosystem, friendly to “Software product”.

Following are the notable announcements in the budget on “Digital economy” Steps:

Stepped up the allocation for BharatNet Project to Rs. 10,000 crores in 2017-18.

Targeting high speed broadband connectivity on optical fibre in more than 1,50,000 gram panchayats, with wi-fi hot spots and access to digital services

A “DigiGaon” initiative will be launched to provide tele-medicine, education and skills through digital technology

No transaction above 3 lakh should be permitted in cash.

Limit the cash expenditure allowable as deduction, both for revenue as well as capital expenditure, to Rs. 10,000. Similarly, the limit of cash donation which can be received by a charitable trust is being reduced from Rs. 10,000 to Rs. 2000.

All indirect tax/ duty exempted on miniaturised POS card reader for m-POS, micro ATM standards version 1.5.1, Finger Print Readers/Scanners and Iris Scanners. Also components for manufacture of such devices exempted.

Increased digital transactions will enable small and micro enterprises to access formal credit. Government will encourage SIDBI to refinance credit institutions which provide unsecured loans, at reasonable interest rates, to borrowers based on their transaction history.

To make MSME corporate tax with annual turnover up to 50 crores will be 25%

Presumptive income tax for SME tax payers whose turnover is up to 2 crores reduced from 8% to 6%.

BHIM app with cashback and referral schemes

exemption of service charge on railway bookings,

Aadhaar based smartcards for Senior citizens

Create a Payments Regulatory Board in the Reserve Bank of India by replacing the existing Board for Regulation and Supervision of Payment and Settlement Systems.

Also Government has on mid the ‘indigenous’ in ICT sector. This is reflected by the proposal on metro rail policy for upcoming metro infrastructure across the country. The budget statement reads, “A new Metro Rail Policy will be announced with focus on innovative models of implementation and financing, as well as standardisation and indigenisation of hardware and software.”

Further in related electronic sector, the budget has exponentially increased the allocation for incentive schemes like M-SIPS and Electronic Development Fund (EDF) to 745 crores in 2017-18. The draft National Policy on Software Product already intends to have a synergy with the EDF in PPP model.

This is not enough on “Digital economy” if the Government itself does not implement the “Digital” in its own functions in pervasive manner. The thought process of the Government seems to be aligned in this direction also.

The Finance Minister has said in his speech, ”we are trying to bring in maximum use of Information Technology to remove human contact with assesses as well as to plug tax avoidance.”

Innovation and Startups

Both innovation and Startups still occupy the thought process at top leadership level. There are signals and clear provisions indicating this.

The income tax exemption window slider for Startups, approved under DIPP, has been increased for 3 years in five years to 3 years in 7 years.

Another new measure is promoting innovation right at secondary education level and in backward areas. “An Innovation Fund for Secondary Education will be created to encourage local innovation for ensuring universal access, gender parity and quality improvement. This will include ICT enabled learning transformation. The focus will be on 3479 educationally backward blocks”, mentions the Finance minister, in budget speech.

Ease of doing business

Ease of doing business is an important topic in PART-B of the content list of budget document. Hence, its importance in thinking process of Government.

iSPIRT has pursued a Stay-in-India-checklist with the Department of Policy and Promotion (DIPP) with an intent to remove various frictions faced by industry in funding, company formation, corporate regulation and taxation issues. A number of steps have been taken up by Government in past one year to sort out these issues.

Announcements like abolition of FIPB, rationalization of taxation (on FPIs, convertible instruments, long term capital gains, etc), lower rate of taxation of 25% for companies with revenue of less than 50 crores, rationalization of labour laws, carry forward of MAT for 15 years, etc. are all in line with the philosophy of iSPIRT’s Stay-in-India checklist.

Among key issues from the Stay-in-India checklist which were expected to be addressed in the budget but have been missed out are angel tax and tax parity between listed and unlisted securities etc.

Level Playing Field