iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

This workshop was organized by the Indian think tank iSPIRT Foundation, French Embassy in India, Consulate General of France in Bangalore, and La French Tech in India, based on the following principles:

Gathering high level contributors from India and France: industrials, transdisciplinary academics, diplomats, officials, business founders, think tank members, technology makers;

Pushing a Workshop format (not an event, not a round table, not a scientific conference), organizing 3 different days with 3 different viewpoints:

Philosophical/epistemological/ human sciences,

Economical/techno-legal/social sciences/adoption,

Application domains and use cases (Health, Culture, Creative Cities, Agriculture);

Targeting recommendations toward the AI Action Summit (Paris, February 2025).

Results:

More than 80 speakers, 100 participants in person (in Bangalore or in Paris), 200 participants online;

14 different countries represented all over the world (India, France, Canada, USA, Mexico, Guatemala, Brazil, Germany, Netherland, Italia, Spain, Portugal, Belgium, Thailand);

An opening session figuring the Ambassador of India to France H.E. Mr. Jawed Ashraf, the French Digital Affairs Ambassador H.E. Mr. Henri Verdier, the Consul general of France in Bangalore Mr. Marc Lamy;

📢Calling all loan agents keen to understand the OCEN 4.0 business opportunity. 🔑📈

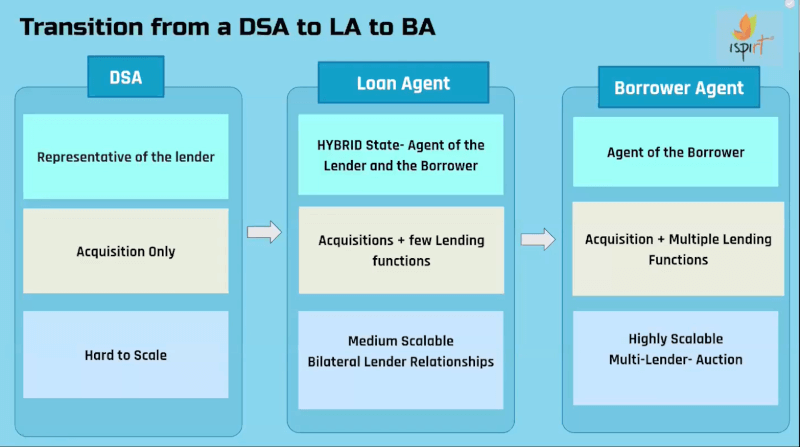

OCEN 4.0 introduces a new and powerful role – the Borrowers Agent(BA). If you are looking to play a pivotal role in the MSME lending ecosystem without lending from your own balance sheet, this new role of a BA may be what you want to understand really well. 💡

The BA role is critical to the OCEN story. In this session, we deep-dive on what this role entails, why it is the linchpin of the OCEN 4.0 model, how BAs enable lenders to go remote, and how this role wields a lot of power. We also talk through how to get started, possible business models for BAs and what to focus on to be a successful Borrowers Agent. 🌟🚀🚀

📢👷🧑💻Calling all TSPs and participants eager to dive into OCEN 4.0 APIs.

If you are wanting to understand the tech, the APIs and get started on building for OCEN 4.0, our second open house on OCEN 4.0 is here for you !! 💡

In this session, we do a deep-dive on the architecture, the loan journey on OCEN 4.0 components, the APIs in the OCEN spec and share how you can build for a participant by mocking the APIs of the other. 📝🔑🧑💻

We’re thrilled to unveil OCEN 4.0, the latest advancement in our Open Credit Enablement Network protocol, revolutionizing cash flow-based MSME lending. 🌟

OCEN 4.0 represents a significant leap forward from our ongoing GeM SAHAY and GST SAHAY pilots. In this iteration, along with updated API specifications, we have also added the OCEN Registry, Product Network and rules, specialized participant roles and much more. All these features help us unlock cash-flow-based lending to match the scale, complexity and needs of Bharat. 🔑📈

Check out our introductory open house session on OCEN 4.0

🔍 More details? The API and documentation of OCEN 4.0 are publicly available at http://ocen.dev and will be updated with FAQs from the open house sessions.

🔮 What’s next? Yes, a lot is happening. We have more open house sessions coming out in the following weeks. We are also actively onboarding Wave 1 partners for OCEN 4.0.

❓Questions? Submit your questions here. 📩Contact? Reach the OCEN 4.0 team at [email protected]

Please note: The blog post is authored by our volunteers, Aravind R andSagar Parikh.

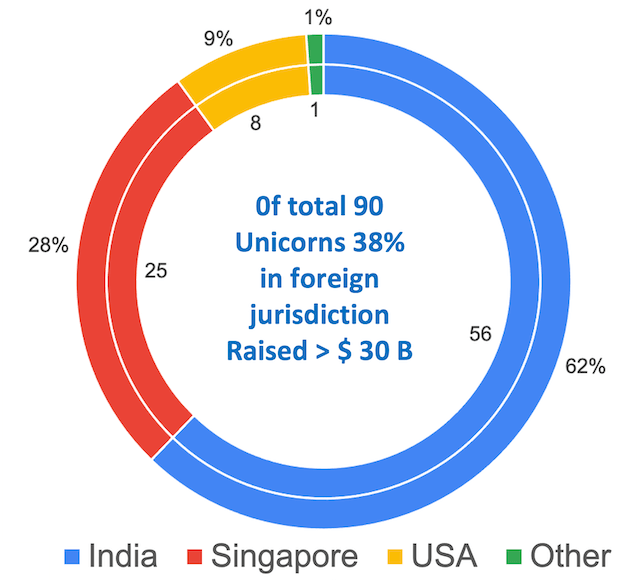

India currently has90 unicorns – startup companies that are valued at over $1b – and will likely soon have 100 unicorns, becoming the third such country after the USA and China. Since January 2016 when the “Startup India” program was launched, the startup ecosystem of India including infrastructure for startups, be it incubators, mentorship, funding, corporate initiatives, media coverage, or even patent filing, has improved substantially making life easier for entrepreneurs.

However, it is still not as smooth a ride for the Indian start-ups as it is for startups in the advanced economies of say, the USA, Singapore, and China. Our “ease of doing business” is yet to be on par with the developed world, especially given the high taxation, onerous compliance requirements, inadequate and cumbersome legal protection of IP, as well as time-consuming and expensive processes to access capital and secure exits. It isn’t a surprise therefore that many companies are shifting their primary legal location to foreign jurisdictions like the USA, and Singapore.

How do the numbers stand?

As per a study by Venture Intelligence, of the presently known 90 “Indian” unicorns), 56 are based in India, 25 in the USA, 8 in Singapore, and 1 in the Netherlands spanning sectors from e-Commerce to fintech to gaming and more. In other words, 38% of “Indian” unicorns are not quite Indian as they are domiciled outside of India. Moreover, these 34 unicorns have raised approximately $30B ie, this large money could have been but hasn’t been invested into an India domiciled entity.

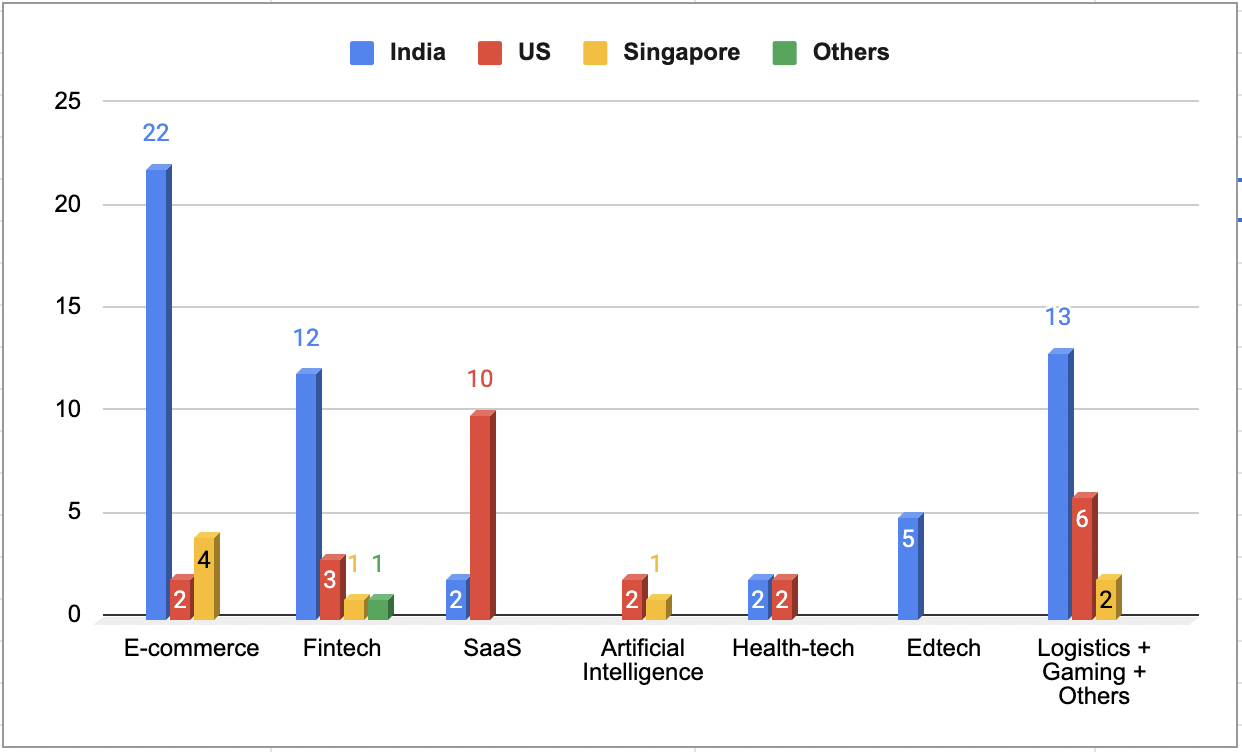

Sector Wise break-up of the Unicorns

Source: Venture Intelligence

Chart: Sector-wise domicile of unicorns as on 31st March 2022.

The reasons for incorporating in the USA are different from incorporating in say, Singapore. SaaS founders find it easier to reach out to the large market for SaaS “Software as a Service” based offerings in the USA by incorporating there. Companies incorporated in Singapore for high “ease of doing business”, low taxation, quality infrastructure, and quality of life while remaining close to India.

Out of 12 Indian unicorns in the SaaS category, all except Zoho and Darwinbox are based in the USA. SaaS offerings are expected to be a $1 trillionopportunityand India will lose wealth creation, tax revenues, listing, and related income, by not having these companies domiciled in India.

Of the three unicorns in a frontier technology area like Artificial Intelligence, namely – Glance, Fractal, and Mindtickle, one is registered in Singapore while the other two are in the USA. Of the 3 unicorns in Gaming, Mobile Premier League and Dream 11 are based in Singapore and New Jersey respectively while Games 24×7 is registered in India.

Flipkart, India’s greatest startup success story and the poster boy for Indian e-commerce, which was acquired by Walmart at a valuation of over $20B, was domiciled in Singapore. That set the trend of e-commerce companies having their HQs in the island country. There are many Singapore shell companies set up by VC funds to become holding companies for Indian subsidiaries. Singapore is today the hottest destination for the registration of Indian e-commerce players.

Even more worrying than this trend of registering the parent company outside India is the migration of startup founders to UAE and Singapore. Lower taxes, easier access to capital, government support, simple compliance, and better quality of life while being just a short flight away from India make the UAE and Singapore rather attractive to founders.

Whichever country our startups chose to register or our founders chose to migrate to, the ultimate loser is India with intellectual property ownership and funds being vested in non-Indian jurisdictions.

Stay in India Mission

In order to retain the economic value added by the start-up ecosystem, it is important that India urgently puts in place policies that ensure that founders and startups ‘Stay-in-India”. This will require the coming together of various ministries, particularly DPIIT/Min of Commerce, Ministry of Finance, Ministry of Electronics and Information Technology, and regulators like the Reserve Bank of India and Securities and Exchange Board of India to address the Stay-in-India Checklist.

Stay-in-India is an evolving checklist of issues that need to be solved to contain the exodus of startups from India. These issues fall under four categories: a) Ease of doing business and making it easy to raise funds; b) harmonization of coding of digital economy c) Reducing overall tax anomalies and d) Increased DTA and foreign markets access.

The issues are comprehensively listed in the Stay-in-India checklist.

As an example, let’s consider the anomalies in the taxation of dividends. Dividend received from overseas subsidiaries, that has been already taxed, is taxed once again in India as income in the hands of the company. Also, while the rate of tax on such dividends for certain companies is 15% (as against 30%), the same exemption is not provided to limited-liability partnerships and individuals. It amounts to double taxation of income and discourages a model where overseas subsidiaries of Indian startups can pay dividends at lower tax rates to Indian shareholders. Removal of this dividend tax will directly encourage start-ups to remain domiciled in India and receive dividend income from subsidiaries abroad.

Similarly, there are regulatory frictions e.g. TDS on the sale of software products which reduces the working capital in hands of Software product companies, or the need for filling the Softex form (which was relevant in the early days of IT services exports), and which is now redundant as GSTN Invoices already have the required and sufficient data. All that is required is for different departments of the Govt and regulators to connect digitally and share information. The unfavourable tax regime for IPR protection, such as subjection to minimum alternate tax, IPRs being subject to income tax, and not capital gains even when they are held for more than a year is another big irritant. Technology-heavy startups, therefore, tend to relocate to jurisdictions like Singapore and the USA that have a smoother and lower-cost approach. Founders relocating to overseas jurisdictions are typically seen around the time of M&A. One of the reasons relates to taxation: typically, a portion of the financial proceeds arising from an M&A transaction is held in escrow and released to the founders after some time and/or completion of certain contractual obligations. The escrow payments are treated as income by the Indian tax authorities rather than capital gains as other jurisdictions do – this needs resolution.

India is emerging as a global startup hub, with the support of the Govt, with our startups attracting capital and talent while being at the forefront of innovation, jobs, wealth, and intellectual property creation. Brand India is enhanced globally by the success of Indian startups. With more support from the Government by way of removal of regulatory friction and by providing incentives – fiscal and regulatory – the ecosystem required to create, enable and grow Indian startups will dramatically accelerate.

The Ease of Doing Business must be tackled in mission mode with the Stay-in-India Mission (SIIM) being an integral part of India is to secure its rightful place around the global innovation table.

Disclaimer: The article depends upon various pubic data sources apart from credible data sources that are relevant at the current date and time. Readers may like to read this accordingly.

India has made rapid progress in digitisation of the economy in the last decade becoming a world leader in identity systems, digital payments and tax, and a new data sharing and empowerment framework. However, many deep-rooted issues still exist, such as extending true financial inclusion; formalisation and creating a higher trust economy, that is essential for growth of mostly small businesses.

In this blog post, we look at innovations in blockchain, distributed ledger and other technologies such as zero-knowledge proofs as potential solutions to build a stronger fabric for the economy for decades ahead. The unique opportunity India has is to boost commerce by enhancing trust, thereby culminating the transformation already underway through existing building blocks of digital identity, payments and data sharing to boost commerce. Unlike many other countries, faster and interoperable payments or reducing the dominance of private money are solved problems for India; the missing piece is to digitise commercial contract enforcement, which on the other hand is a solved problem for developed countries. Lack of adequate contract enforcement caused by contracting parties having different versions of the truth; due to data systems that don’t interoperate reduces trust and creates friction for economic growth. Solution requires connecting the goods and services ledger to the money ledger, so that contracts of any kind become binding promises that can be executed programmatically. Using technology to solve this trust problem is a unique opportunity for India.

BADAL (also happens to be a word for Cloud in local language), a techno-legal solution in the form of “Distributed Ledger for Privacy-preserving Trustful Commerce; is proposed as an interoperable fabric underlying a future programmable economy across large and small businesses to create high trust economy.

We also look at the emergence of Central Bank Digital Currency (CBDC) which is one of the core money applications of this framework and global backdrop in Annexure. There are many other use cases being proposed from land records to decentralised clinical trials for blockchain and allied technologies in different areas of government and business1https://www.meity.gov.in/content/national-strategy-on-blockchain likewise, that can be implemented in BADAL.

First of all, why is trust important?

Trust is the basic glue that connects strangers and promotes economic activity. Money is the basic economic institution in a society building that trust2https://press.princeton.edu/books/paperback/9780691146461/the-company-of-strangers. However, trust builds slowly due to a combination of various factors such as the nature of institutions (political and legal) and the level of formalisation. While formalisation of even small businesses is increasingly addressed by the successful rollout of GST for India, formalisation of trust still remains elusive. At a core fundamental level, trust is a public good that creates friction-free commerce and is a recipe for rapid economic growth.

There is a high correlation between the level of trust in society and GDP per capita3https://ourworldindata.org/trust-and-gdp. A study conducted by World Value Survey attempted to measure the level of trust in a country by recording the positive responses received to the question ‘most people can be trusted’. It found that countries with high GDP per capita such as Sweden, Norway and Netherlands recorded high levels of trust exceeding 60% determined in this manner as the graphic below shows.

Douglass C. North, Nobel laureate in economics4https://www.nobelprize.org/prizes/economic-sciences/1993/north/lecture/, found that ‘the inability of societies to develop effective, low-cost enforcement of contracts is the most important source of both historical stagnation and contemporary underdevelopment.’ The Union Minister of Finance and Corporate Affairs has rightly acknowledged the role of the “Hand of Trust”5https://pib.gov.in/PressReleasePage.aspx?PRID=1601273when presenting the Economic Survey of 2019-20.

In societies like India, with limited ability to efficiently enforce routine civil or property contracts, businesses tend to restrict working with those similar to them based on caste, religion etc. (called associational activity) where there is an implicit social and moral enforcement mechanism or with members who have clearly demonstrated reputation in the past (usually the large or the older players). In both these situations, the economic benefit that a new firm can bring with new ideas or new techniques will be muted as its absorption is slower. Similarly, a new player will find it very difficult to compete with incumbents even if such players are economically more efficient. Economist Olson6Olson, M. (1974). The logic of collective action. Harvard University Press showed that associational activity is often more detrimental than favourable for an emerging economy. So we need better ways to break this trust logjam. Trust in the money system in India is comparatively high, as promises tend to be kept with sufficient legal backing and can be digitised with e-mandates or automated payments/ collections; but the same is not the case for goods (or services) ledger, leaving room for delays cascading into a logjam resulting in low trust. This is often felt in day to day life by citizens not getting routine services despite advance payment or small businesses not getting paid despite having supplied goods. Delays, defaults and disputes can become the norm if parties have different versions of the truth.

Every economic activity is thus like a mini-contract with one side on the money ledger (payment from party A to B) and the other side, on the goods/services ledger (from B to A) between counterparties, and can be converted into an electronic contract that automatically executes on both ledgers subject to interoperability. To assure the performance of contracts, the money ledger and the goods/ services ledger need to be connected in a way that is scalable, privacy-enhancing, non-repudiable and programmable. This enables a contract agreed between parties becomes a commitment, and fulfilment is guaranteed by code through the electronic contract. Assuring performance of contracts is critical for a country that is seeking to grow through startup activity, not just in tech but other sectors too.

Currently, litigants lose nearly ₹ 50,000 crores annually in wages or business lost which comes to 0.5% of the country’s GDP, because of litigation, an indication of how expensive litigation can be. The majority of civil disputes in courts are related to recovery of money (30.2 per cent) and land-or property-related matters (29.3 per cent) As reported in the 2016 survey carried out by DAKSH. Common reasons for dispute are different versions of the truth of contracting parties, prior to contract (past) or during the performance of contract (future). Having the same truth and programmability inherent in electronic contracts is a boon in this regard.

In an earlier blog, we have explored the benefits of adapted blockchain technologies to solve the problem of SME financing in India with a related post by global experts7https://balajis.com/add-crypto-to-indiastack/. We build further on that and believe that India can harness recent advances associated with blockchain technology to enable trust between unrelated parties by combining the best of the scalable and centralized legacy world with a secure and private decentralized world. This can benefit the real economy vastly along with the financial world.

Innovations in distributed ledger technologies and BADAL

Distributed Ledger technology can help in two ways – first by being able to verify past performance before one party strikes a deal with another, and second, by being able to enforce a contract in most situations as performance unfolds in future. Thus, building trust about the past as well as the future.

We thus imagine a fabric based on the following basic principles to help create and grow a large number of applications to record economic activity even while reconciling with other activities and past data and help inject a level of trust by creating a reliable, immutable record of trusted data records and programmable contracts

Single platform to allow standards bodies and organisations to publish their schemas, and reuse other schema elements in composing workflows

Fully privacy-preserving capabilities to allow participants to publish relevant zero-knowledge proofs which do not require private data to be shared beyond the participating entities

A programmatic contracts capability that can help automatically carry out the relevant tasks as agreed on without any further manual intervention

By connecting a new digital money ledger (such as Central Bank Digital Currency, or stablecoins) with the new goods & services ledger, we envisage a boost to trust across economy and commerce. As such, BADAL is the first such framework we are aware of globally, uniquely suited to India’s needs, opportunities and strengths.

We have discussed the early version of this in detail in an earlier open-source document8https://github.com/iSPIRT/ppl, called Public Private Ledger. BADAL is thus a privacy supporting, trust enhancing mechanism of coordinating economic activity, and information recording and sharing. Originally this group started out of a process to explore the domain around and figure out the appropriate model to support CBDC, support data sharing between participants, and coordination and automation of event-based standing instructions across events in the goods and services ecosystem and/or money flow.

We then reviewed exciting developments in related areas first to understand their relevance given India’s unique needs. Blockchain technologies generally are seen to enable unrelated parties to trust each other and transact without depending on a central institution or intermediary. These technology innovations are around three key areas:

Maintaining immutability and integrity of data across the distributed ledgers of parties.

Governance mechanisms, especially for decentralised networks

The programmability of such transactions to allow automatic execution.

Public blockchain technologies like Bitcoin and Ethereum, on the other hand, are based on a philosophy of distrust of centralised institutions like Central Banks and are designed for unrestricted access and decentralised decision-making. But they have had to develop new approaches to contend with a few challenges, especially given the huge growth off late that see further wor:

The enormous consumption of resources to establish ‘proof of work’ that limits efficiency and scalability, leading to newer approaches

Exposing all transactions on these networks that generally do not allow sensitive data to be private on the key layer, is as critical for confidential business data as it is for personal data

Rise of many networks that are not interoperable with each other or with the mainstream economy, though some bridges do exist

May have ability to operate outside banking conduits and regulatory frameworks that challenges government’s sovereignty and financial stability through greater oversight has been coming recently

Research on amending throughput, reducing costs and enhancing privacy/auditability/KYC compliance has been ongoing at a rapid pace, especially over the last couple of years.

Despite these unresolved issues, Public blockchain-based tokens, so-called cryptocurrencies, NFTs etc have become an unregulated asset class, especially amongst the young rapidly given the ease of use, creating concerns on possible misuse as well as potential opportunities. We were also part of the recent consultation of the Parliamentary Committee on Finance on ‘Cryptoassets: Opportunities and Challenges’ and had shared with them some of our ideas above in our submission here9https://docs.google.com/document/d/e/2PACX-1vShkuTno_bSILFZPf-Cb_KNwwgM6A_6OgyRiASNS0tXB3ViriHztovrkL7sebiAC7O54y0uwQheTdin/pub.

Various solutions have been employed to address some of these challenges:

Permissioned blockchains, such as Hyperledger Fabric and Corda, allow only trusted parties to participate. Corda uses Notaries for verifying transactions. Such solutions have been successfully used in finance, supply chain, property rights, healthcare, education and e-governance

Zero-knowledge Proofs (ZKPs) allow proving/verification of specific aspects of data without actually making the data public

BADAL builds on the above primitives and is offered as an open and interoperable platform to enable money ledgers such as CBDC/stablecoin along with applications relevant for finance and commerce. This can be designed as a permissioned network relying upon a few regulated entities, and interoperable to ensure that its benefits are widespread and at much lower costs than permissionless systems. It consists of a private ledger that holds sensitive user data withaccess restricted to participating entities only, and a public ledger that contains notarised zero-knowledge proofs about transactions between users. It supports different schemas (configurations) that enable usage across different use-cases.

This programmability coupled with immutability akin to electronic contracts, allows applications in BADAL to be used to leapfrog the trust logjam, without diluting sovereign privileges of control of money given India’s stage of development. BADAL will thus establish provenance that helps establish credibility and reputation of transacting parties, proof of title/ownership of goods and assets, proof of the history of transactions including promises made and ambiguously defined and fulfilled; automatic execution of terms of contracts along with privacy as a fundamental right.

Historically, monetary accounting has solved for only one side of this metaphorical coin- the monetary value. All monetary systems denote a money value to any transfer of goods or services. BADAL, being a ledger that can record value in any domain, solves for the non-monetary aspect of the transaction. Integrated with electronic contracts for a variety of applications, BADAL will enable digital claims on non-monetary assets, including new age asset classes such as crypto assets, NFTs, where claims can be financialized and liquidated. An inherent promissory layer can be enabled into the current transaction mechanism. This extends to all data types, from land records to hospital quality service quality etc, rather than just transactions involving money and goods/ services.

The ability to connect any of the data types across domains can give rise to massive amount of efficiency gains with automated execution thanks to new data from machines like cars, consumer durables like refrigerators or health wearables coming from advances in IoT (Internet of Things), 5G, Imagine a use case of automated crop insurance with sensors that monitor weather from a satellite in space to moisture in soil etc. and deliver claim benefit to the farmer with zero friction in real-time.

One of the biggest problems BADAL could solve at bottom of the pyramid is financial inclusion in India. This is not only in the form of increased monetary transactions through it, but also the ability for MSME’s to gain cheaper credit. This is a possibility as MSME’s will find it easier to prove their liquidity and income to banks and other lenders due to the monetary traceability the system will provide. An increased ability to prove financial stability will lead to greater leverage for borrowers and more systemic trust for lenders. This increase in the systemic trust will not only lead to an increase in credit creation but catalyse an increase in money velocity in India as a whole.

In a subsequent blog post, we will detail the potential use cases; as well as preliminary design of a prototype of one sample use case that is being built currently.

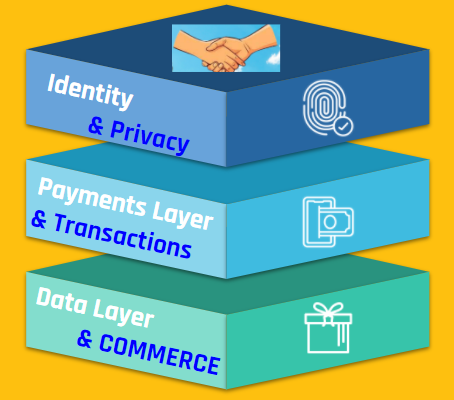

BADAL fabric supporting India Stack could boost digital India

India has pioneered transformations in Identity, Payments, and Data empowerment (these building blocks are popularly called the India Stack) through a techno-legal approach. These address friction of doing business, information asymmetry, and distributed systems. Breakthroughs along the way were public platform (identity), public protocols and standards, and techno-legal approaches to solving big societal problems.

The recent launch of the Account Aggregator (AA) model (based on Data Empowerment and Protection Architecture, DEPA) allows the controlled sharing of private financial data by citizens with various financial institutions to get the best deals. This is a global first and in some sense, an export of a truly global standard12https://twitter.com/Product_nation/status/1435997280692158464?s=20 from India.

Open Credit Enablement Network (OCEN) is creating a way to democratise access to credit, to the level of making it accessible to a street vendor for small sums. These public goods prevent any large player from monopolising the data ecosystem and at the same time reduce the cost of providing service. For instance, microloans as small as Rs.300 can be availed on GeM-SAHAY leading to true inclusion at the bottom of the pyramid.

These techno-regulatory concepts are now being considered for adoption by several countries across the world. Overall, India is arguably ahead of most countries in adopting technology for promoting financial inclusion as well13https://www.bis.org/publ/bppdf/bispap106.pdf.

Image Courtesy: Ananya Phadke

The next building block now is the trust layer through BADAL, ensuring every commitment is met and every contract is enforceable, boosting transparency and growth over the next decade. Trust permeates through all three ends of this triangle as identity is the ‘who’; and data and payment relate to ‘what’ of commerce. In BADAL, identity and data sharing can be achieved without diluting privacy to enable trusted payments (& commerce).

Annexure: CBDC Developments

While BADAL provides fabric to money or goods ledgers, we describe CBDC in detail here, given its importance. Money was traditionally issued by the sovereign (through a Central Banker) and circulated in the economy through layers of banking intermediaries. With the advent of permissionless public blockchains, some of which also seek to portray themselves as alternate currencies, the sovereigns have taken note and introduced their own variant as a public good to protect the financial stability of the nation-states. This sovereign/state-issued digital currency is popularly known as Central Bank Digital Currency (CBDC).

While there are different types of CBDCs such as wholesale/ retail and account-based/ token-based, ultimately a payment using CBDC can be immediately settled. This is akin to using paper money and unlike a cheque or money transfer between bank accounts that require a process of clearing and settlement adding to inefficiency and costs. CBDC can potentially thus leapfrog depending upon the development of existing banking systems in different countries.

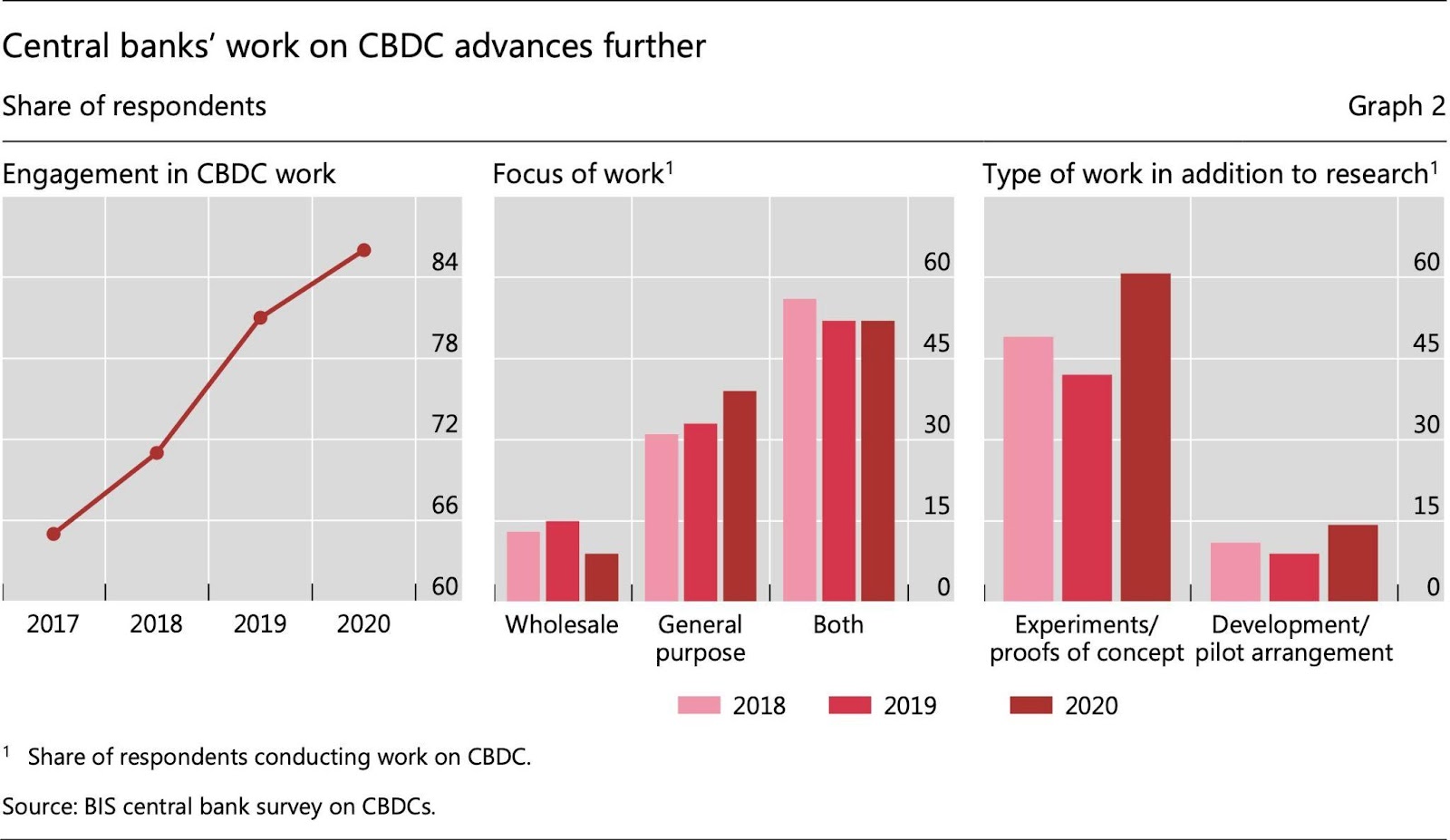

Advanced Economies (AEs) and Emerging Markets and Developing Economies (EMDEs) have different motivations for issuing CBDC to end-users (via Retail CBDC) and financial institutions (via Wholesale CBDC), illustrated in the diagram below.

In the USA, payments are expensive due to its legacy system of banking. This has led to a burst of digital payment options, the latest being ‘stablecoin assets’ (digital currencies backed by real assets like US dollar, treasuries, etc) that also compete with their money-market funds. Stablecoin assets have crossed $100 billion25https://www.statista.com/statistics/1255835/stablecoin-market-capitalization/ in market value and are a popular choice to transact in Decentralised Finance (DeFI). DeFi is a parallel financial system evolving around crypto-assets. DeFI is not subject to transparency and compliance required in the conventional financial world at this point in time. As DeFi becomes big and interacts with the conventional financial world, there is a growing systemic risk arising from failure or fraud in DeFi. The US Government, therefore, wants to regulate some aspects of DeFI26https://www.federalreserve.gov/monetarypolicy/fomcminutes20210728.htm and may thereby bless some stablecoins and crypto-assets as explicitly permitted financial products. Earlier in 2015, Bitcoin was determined to be a commodity27https://www.cftc.gov/sites/default/files/2019-12/oceo_bitcoinbasics0218.pdf by some authorities there. The US Fed has also begun a consultation process towards design choices and feasibility of CBDC implementation.

Indian perspective

In India, the focus of policy has rightly been on promoting financial inclusion to formalise the economy and drive economic growth. One important factor which drives the usage of unregulated informal value transfer systems is the lack of banking facilities and corresponding amenities for managing money, which leaves rural communities without alternatives other than a person-to-person method of transferring monetary value. Even though India has seen a significant increase in the number of bank accounts created, Reserve bank data still highlights little improvement in account usage and institutional borrowings, which feeds into the broader issue of financial inclusivity.

Initiatives like Pradhan Mantri Jan-Dhan Yojana (PMJDY) opened doors to big change. UPI has been very successful as a payment mode but still needs underlying bank accounts to transact and thus depends on the banking system & its motivation to provide access to the poor. The PMJDY scheme announced in 2014 has increased the number of adults with bank accounts to 43.47cr 28Progress Report as on 22-Sep-21, PMJDY, MOF, GOI, https://pmjdy.gov.in/account (~46% of 93.55cr adults with an Aadhaar29https://uidai.gov.in/images/Saturation_Report_State-UT_Agewise_31-08-2021.pdf). Despite this headway, there is still a lot to be achieved. The Financial Inclusion Index (FI) recently launched by RBI shows that India is at 53.9 on March 21 (vs 43.4 in March 2017) – a little more than halfway towards complete financial inclusion (FI of 100)30https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52068. Presently, the banking system acts as the main gateway to financial inclusion as the banking system is the main distributor of cash. Hence, various government programmes (like PMJDY) rely upon banks for financial inclusion, despite those being not remunerative for banks. The accounts also have various restrictions on the number of debits/withdrawals to ensure low cost.

Even with the existence of such low-cost bank accounts, the poor do not have an incentive to use a bank account regularly as they do not save enough to use the bank account as a store of value. They use these accounts mainly to collect remittances and withdraw cash at ATMs as bulk of their transactions is in cash, not leaving a visible money trail that in turn makes financial inclusion difficult. Cash in circulation in India even now is Rs 29.38 trillion31https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52274 (~14.9% of estimated GDP for 2020-2132http://mospi.nic.in/sites/default/files/press_releases_statements/Statement_12_1st+September+2021.xls) despite the availability of these cheaper accounts, demonetisation in 2017 and the subsequent formalisation of the economy with GST, RERA, etc.

In addition, the cost of handling cash by the central bank and commercial banks (currency printing, operating currency chests, logistics of moving currency, ATM operations, etc.) has been estimated to be ~Rs 21,000 cr (Rama Bijapurkar) and ~1.7% of GDP ( (Visa Inc., 2016). High adoption of CBDC can help in reducing this cost while creating enormous amounts of data and enabling policymakers to diagnose and regulate better. At a later stage, CBDC can also be used for targeted monetary policy actions when its impact on the financial system is well understood. Experts are concerned that CBDC may result in the disintermediation of the financial system. This risk can be mitigated by following design principles set out by the Bank for International Settlements (BIS)33https://www.bis.org/press/p201009.htm (i) “do no harm” to monetary and financial stability; (ii) coexist with cash and other types of money in a flexible and innovative payment ecosystem; and (iii) promote broader innovation and efficiency.

CBDC inherently provides an alternative to cash to directly reach a customer and can complement the banking network to make adoption quicker. By providing a digital alternative to cash will enable building verifiable money trails that can lead to greater financial inclusion by private players providing customised health, insurance, investment & education products in compliance with privacy laws. In the financially excluded segments, CBDC, being a form of central bank currency, is likely to be well trusted and be adopted easily.

The blog post is co-authored by Sanjay Phadke, Dhananjay Nene, Sharad Sharma, Navin Kabra, R Barve, K Babel, V Agarwal, K Gokarn, Kalyan Narguru, Shashank B, Arun Maharajan, Karan Sirdesai, P Sahu, P Rao, A Kulkarni, Krishna Iyer, V Nene and A Lath.

If you have any queries or comments, please contact us at [email protected].

iSPIRT Foundation welcomes you to the virtual launch of the industry-wide Account Aggregator (AA) ecosystem on September 2, 2021.

This event announces the major financial institutions that have gone live, and demonstrates the powerful use cases of AA. It will be a major milestone for the AA framework for consented data access and sharing in the financial sector.

Time (IST)

Session

Speaker(s)

4:00-4:10 PM

A Regulatory Framework for Account Aggregators and the Path Ahead

Shri M Rajeshwar Rao, Deputy Governor, Reserve Bank of India

4:10-4:30 PM

The Account Aggregator Leapfrog is Here!

– Presentation by Shri Nandan Nilekani, Chairman, RBI Committee on Deepening Digital Payments (2019) and Volunteer, iSPIRT – Workflow demonstration by Shri Siddharth Shetty

4:30-4:35 PM

The Early Builders on AA

Hear from a cross-section of ‘early mover’ CEOs and leaders of major Banks/NBFCs, Account Aggregators, and Technology Service Providers

4:35-4:45 PM

A Global Perspective on India’s Account Aggregator Model

Shri Siddharth Tiwari, Chief Representative for Asia and the Pacific, Bank for International Settlements

4:50-5:35 PM

Fintech Roundtable: Innovating on AA for Improved Financial Services

Panel discussion moderated by Shri Rajesh Bansal, CEO RBI Innovation Hub.

Fireside Chat on the Future of Cross-Sectoral Data Sharing

Moderator: Shri Amitabh Kant, CEO, NITI Aayog; Panellists: Dr RS Sharma (Chairman, National Health Authority); Shri Ajay Seth, Secretary, Department of Economic Affairs and Member, Financial Stability and Development Council (FSDC)

5:55-6:00 PM

Designing User Control over Data for India

Hear from current and future Account Aggregators on innovating for control over our personal data

The internet connected the average Indian to millions of sources of information. Could crypto protocols connect Indians to millions of sources of capital?

To achieve its goal of a five trillion dollar economy by 2025, India needs to close an enormous financing gap for its small and medium-size enterprises (SMEs). It already has important assets with which to attract global capital: the youth of its population, the energy of its tech sector, the growth of its internet connectivity, and the rising acceptance of so-called informational collateral in lieu of traditional physical collateral. But what hasn’t yet been done is to integrate these assets into the new multi-trillion dollar cryptoeconomy, which may have the most risk-tolerant, internationally oriented, growth-seeking pool of investors in the world.

In this piece we begin by reviewing India’s need for SME and startup capital. We then tick through India’s existing assets, with particular focus on informational collateral, which combines the previously separate concepts of due diligence and physical collateral into an internet-friendly financing package. Finally, we discuss why global crypto investors could help meet India’s capital needs.

India’s need for SME and startup financing

India is home to more than 60 million businesses, 10 million of which have unique GST registration numbers, most of them SMEs. However, of the one trillion USD worth of total commercial lending exposure of the banking system, only ~25% of it is provided to SMEs, which are considered less creditworthy than larger corporates or multinationals. This has resulted in a financing gap estimated to be between 250-500 billion USD, where meritorious businesses without national profiles aren’t able to access the capital they need to finance their growth. India’s next trillion in GDP growth depends upon solving this problem, but the incumbent financial system may not have the resources to fix it alone. Despite ever-increasing bank branches, India’s legacy financial system is still slow, costly, and unwieldy for borrowers— in sharp contrast to the databases, online KYC systems and intelligent lending apps of new-age fintech companies. And in addition to this high cost of capital for MSMEs, India also has a low baseline level of financial inclusion.

The baseline issue is being partially addressed with low-frill Jan Dhan accounts, which are providing partial banking support for millions of previously excluded individuals. Many of these Jan Dhan accounts are held by small businesses, entrepreneurs, students and self-employed people in rural India, the same folks who are running India’s SMEs. But these accounts have only inflow data, with outflows typically in cash. Even though cash still plays a big role in the self-organized and informal sectors, it’s not easy to provide business-related financing in cash. The so-called JAM trinity (Jan Dhan accounts, Aadhaar digital identities, and Mobile phones) offers a partial solution for this under-banked population, but it only supports what we might think of as consumer-grade applications like basic peer-to-peer payments and individual savings accounts. Access to capital sufficient to finance a business — a true measure of financial inclusion — is still not yet present for these low-income, mostly feature-phone possessing groups.

On the other end of the spectrum from rural SMEs are India’s tech startups. Over the last decade, India has broken into the ranks of global technology and is now the #3 generator of unicorns in the world. Supportive governmental policies, combined with a young, creative, and aspirational workforce has helped reimagine large swathes of the economy including diverse industries such as e-commerce, logistics, SAAS, education, food, healthcare etc. This rise has attracted global equity and loan-funds that could in turn help many start-ups become world beating players in their respective domains. But the startup sector is just as hungry for capital as the rural SMEs, and India’s startup economy is still somewhat disconnected from global venture capitalists and financial markets.

India’s assets: youth, growth, connectivity, and informational collateral

India does have assets with which to close the capital gap. It has a youthful population. It has a fast-growing economy, even given the setbacks of COVID-19. It has an enormous population of hundreds of millions of new internet users. And it has something new, which is the possibility of informational collateral as a sort of combination of traditional concepts of due diligence and physical collateral.

Specifically, the SME funding gap is most pressing for the Indian cash-flow businesses that don’t have the physical assets to take out loans, which are the mainstay of the current, hard-collateral-backed credit system.

One alternative is to use trustworthy digital records to ascertain whether a business is worthy of credit or equity investment. India’s Goods and Services Tax (GST) helps to address this by generating invoice and payment data in a format suitable for credit underwriting and risk analysis. The GST data also enables a small enterprise in a large value system to provide data and visibility across the supply chain; for example, one can track the progress of parts from a small parts supplier to an auto component manufacturer to a large passenger car maker all the way through to distributors, sub-dealers, and retail sales.

The digital version of an SME’s sales and purchase invoices ledger thus amounts to informational collateral on both the company and the larger ecosystem within which it sits, that could become the basis for extending credit, as an alternative to the hard asset or collateral-based financial system. This is similar to how Square Capital and Stripe Capital already function in the West.

In addition to credit-based financing, the trustworthy records furnished by GST’s informational collateral can also support equity or quasi-equity financing, to support growth without increasing debt. These might take the form of direct equity investments in small businesses, or even personal micro-equity investments in individual consultants or students.

India’s innovation: use new pools of crypto capital to address long-standing financing needs

So, we understand that (a) Indian SMEs need capital, and that (b) IndiaStack’s UPI and Aadhaar can help GST generate informational collateral for potential investors and lenders.

Now the question arises: what class of investors is most willing to use this newfangled type of informational collateral to invest in potentially high-risk businesses outside of the proven venues of America, Europe, East Asia and the large Indian enterprises? Who are the most risk-tolerant, international, forward-looking, class of investors in the world — willing to risk millions of dollars purely on the basis of internet diligence alone?

It may turn out to be the new class of wealthy, globally-minded crypto investors. After all, the 10-year old cryptoeconomy is now worth trillions of dollars, there are more than a hundred million crypto holders around the world, and there are at least fifty crypto protocols valued over one billion dollars, a “unicoin” analog to the traditional tech unicorn. While still small in comparison to global capital markets, a sector worth $2T that is growing at more than 100% per annum could become a much larger piece of the global financial puzzle in short order. This is a new source of risk-tolerant digital capital that could flow into India to help close the SME financing gap, if we can make it an attractive proposition for the global investor.

Specifically, India could offer a viable path to deploy this new crypto wealth in a controlled manner, while solving for SME financial inclusion. Inflows of cryptocurrencies from KYC-ed investors through approved Indian and global exchanges can potentially be allowed into India for the purposes of enhancing SME access to low-cost global capital. GST-registered companies could, for instance, receive capital against their issued e-invoices and other information collateral in special accounts opened via a controlled conduit such as GIFT city, which is one of India’s favored bridges to international markets. The companies benefiting will need to explicitly consent to sharing their information and receiving funds into a new account at system-level while capturing cash flows against invoices for repayment. Inflows of global crypto-capital into Indian SMEs could also enable the rest of the credit system to migrate to informational collateral-based lending. And the special account could eventually be ported to a wallet backed by a national digital currency, such as the proposed digital rupee.

For more detail on this possibility, we invite your attention to Balaji S. Srinivasan’s companion piece on the subject, where he proposes to Add Crypto To IndiaStack. Balaji makes the case for crypto-powered extension of IndiaStack, which broadens IndiaStack from its current mostly domestic remit into an international platform for attracting capital from around the world. He describes several case studies by which the emerging world of decentralized finance or “defi” could help enrich the Indian economy, without competing with the digital rupee. For example, Indian startups could benefit from crypto crowdfunding, Indian SMEs as discussed could access global defi lending pools, and Indian students might even be funded with the emerging concept of personal tokens, like an equity-based version of microfinance. As the former CTO of Coinbase, the $100B crypto goliath, and a former General Partner at Andreessen Horowitz, the $16B venture capital firm, Balaji’s proposals have technical and social support from the very class of investors we’d seek to attract. At least insofar as they relate to the issue of plugging the SME financing gap, we believe they deserve serious consideration by policymakers in India.

In short, India has a unique opportunity to close the SME financing gap by attracting the new class of global crypto investors, by using everything the IndiaStack team has helped build over the last decade — particularly UPI, Aadhaar, GST, and the informational collateral they generate — to help connect the trillion-dollar cryptoeconomy to capital-hungry Indian entrepreneurs.

A Committee of Experts under the Chairmanship of Shri. Kris Gopalakrishnan has been constituted vide OM No. 24(4)2019- CLES on 13.09.2019 to deliberate on Non-Personal Data Governance Framework. Based on the public feedback/suggestions, the Expert Committee has revised its earlier report and a revised draft report (V2) has been prepared for the second round of public feedback/suggestions. iSPIRT had provided a past response to the previous report and in this blog post contains a response to the revised report.

At the iSPIRT Foundation, our view on data laws stems from the following fundamental beliefs:

Merits of a data democracy (that is, the user must be in charge)

Competitive effects must be well understood, for creation of a level playing field amongst all Indian companies, and some ring-fencing must exist to protect against global data monopolies

Careful design enables both high compliance and high convenience

It is with these perspectives that we have analyzed the revised Non-Personal Data report in our response.

Key Sources of Ambiguity in the NPD Report

The key sources of ambiguity in the report are:

Purpose of techo-legal framework for Non Personal Data: The non personal data framework is meant to provide the right legal and technology foundations for world class artificial intelligence to be created out of India for the betterment of financial, health, and other socio-economically important services. The current version of the report sidesteps this completely by constraining the applicability to only “public good” purposes rather than taking a holistic approach to “business & public good purposes”

Data Business entities need a harmonised definition (given the interplay with data fiduciaries as proposed in the MeitY Personal Data Protection Bill) and clear incentives for participation. The current report relies excessively on regulation & processes for data businesses to achieve the outcome.

Institutional structure for Data Trustees: The report restricts Data Trustees to government agencies and non-profit organisations; however, in a domain consisting of fast evolving technology by excluding the private sector in offering the base infrastructure creates a severe limitation on the ecosystem of modellers that can be created.

Technology Architecture: The illustrated technology architecture is unclear around the public infrastructure (through the form of open standards, public platforms, and others) that need to be created & adopted to bring to life the non-personal data ecosystem in an accelerated manner.

Conclusion

While we’re aligned with the vision of the committee, it’s critical that the above ambiguities are resolved in order to create a strong non-personal data ecosystem created in India. Till these ambiguities are resolved, the recommendations of the Report should not be operationalized.

For any press or further queries, please drop us an email at [email protected]

Two Cs are extremely critical for startups: Capital and Customers. In India, with a population of 1.3B, customers for B2C or B2B2C startups is not an issue. For B2B startups, although the market in India is promising, global markets are still very important. Capital on the other hand is trickier. The total capital raised by startups India from 2010-2020 is around $100B. In the same period, startups in China have raised 4x and startups in the US have raised 10x the capital raised by startups in India. India needs to have a stronger mechanism to enable more Capital. There is a need to increase Capital availability in India.

IGP platform proposed by SEBI is a very refreshing initiative that aims to address the Capital issue. It provides another great avenue for startups looking to raise series B and beyond. This platform can double the available capital over the next 5 years. It addresses a key pain point of Capital availability for startups raising between INR 70 to INR 200 Cr. There is a chasm in this space- there are early-stage VC funds and there are PE funds for growth companies. However, there is not enough growth stage VC funds in India to fill this gap. IGP has the potential to be the platform to bridge this void.

The design of IGP has been very thoughtful with the key focus is on technology startups. The precursor to IGP was ITP (Institutional Trading Platform). Due to various reasons including the maturity of the startup ecosystem, the response to this platform was tepid. IGP addresses a few key pitfalls of ITP.

IGP restricts the listing to technology-focused companies with a proven Product-Market Fit and entering its growth phase. The revenue of the companies listing on this platform is expected to exceed INR 50 Cr. This will greatly help in mitigating the risk of listing by ensuring a good understanding of Product-Market Fit beforehand.

The governance issues are well balanced – protects the investor interests but at the same time provides enough flexibility for the founders to have control over strategy and execution. The companies listing on this platform cannot be burdened with the same rules of the public markets as they need to be very nimble. A balance between taking risks and moving fast with financial discipline as against governance practices such as quarterly reporting and stability is advised.

As in the case of investments in Alternative Investment Fund, the platform is selective about its investors. The companies listing on this platform need to operate as startups and not as mature companies. The risks are much greater with these companies and hence it is very critical to have investors who understand these risks and who can understand these nuances.

M&As have been a key hurdle for startups in India. This is one of the key reasons for companies opting to flip. The platform is designed to simplify the process of M&As, post-listing. Simplifying the M&A process encourages corporates and PEs to participate on the platform. However, this spirit should be maintained in the implementation of the platform as well. This is one of the critical success factors for the platform.

For the Indian startup ecosystem to become one of the major contributors to the economy, key policy changes are needed. IGP is one such platform that has the promise to increase capital availability significantly. IGP has the added advantage of enabling exits for early stage investors. This increases the liquidity in the market that will further spur the startup ecosystem- a much needed virtuous cycle.

NASDAQ encouraged and enabled technology startups to list because of its adaptability and easier listing and governance guidelines. This accelerated technology startups in the US. IGP has the potential to be that platform in India. India can build products for the world and has the potential to be startup capital, but it needs a perfect storm of- Capital, Liquidity, Policy, Customers, and Entrepreneurs. IGP certainly has the promise to address the Capital and Liquidity aspects. Most importantly it enables Indian startups to stay in India!

“If you want to go fast, go alone. If you want to go far, go together.”

Over the course of four weeks in July and August 2020, iSPIRT conducted a series of Open House Discussions to introduce and familiarise India’s fintech ecosystem with the new Open Credit Enablement Network (OCEN).

Background

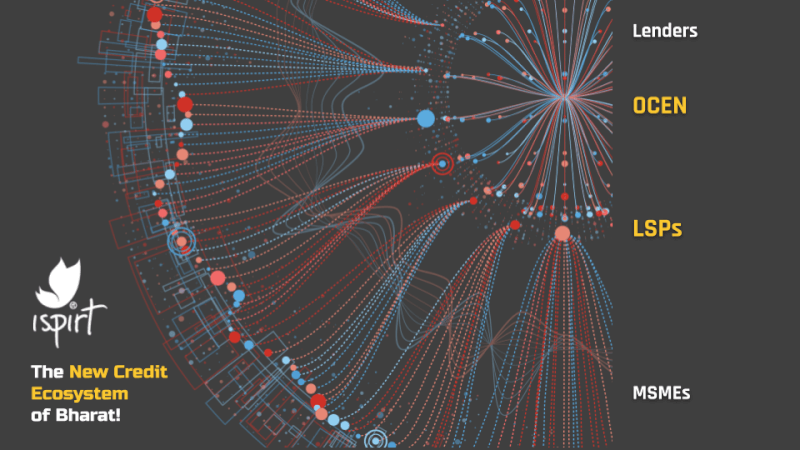

OCEN is a new paradigm for credit that seeks to provide a ‘common language for lenders and marketplaces to build innovative, financial credit products at scale’.

Announced recently, it is a reimagination of the credit ecosystem, where any service provider that has an interface with users (individual or MSME) can now effectively ‘plug in’ lending capabilities into their current operations through the use of a standard set of APIs, thus taking on a new role as Loan Service Providers (LSPs).

The idea behind OCEN is to standardise the various components of a typical lending value chain so that any marketplace, app or platform that already aggregates users can make use of these APIs to cater to the credit demands of their customers. This eliminates the need to expend time and energy on setting up individual integrations with potential lending partners.

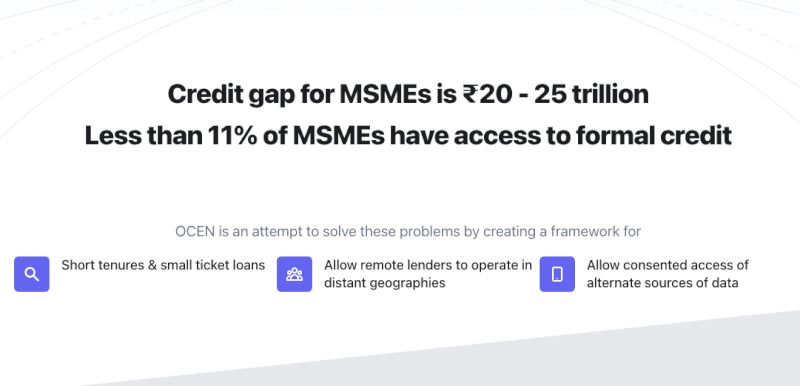

OCEN is trying to solve for one of India’s most devastating roadblocks to financial inclusion i.e. access to formal credit for the individuals and businesses that need it most. The unit economics and archaic models of our existing lending setup have led to an MSME credit gap of $330 bn with only 11% of our small businesses being able to access credit from traditional lenders.

By tapping into the existing customer pools of LSPs and working in tandem with other components of our public digital infrastructure (UPI, Account Aggregators, e-KYC etc), lenders can nullify the costs of discovering and servicing new customers, while also leveraging alternate data to offer more personalised, innovative credit products. OCEN will help to facilitate a methodical shift from balance sheet-based lending to cash-flow based lending that will help to bring more borrowers under the canopy of our formal credit system.

There are numerous ways for participants to contribute across this new OCEN-enabled lending value chain, and indeed it will take the combined efforts of lenders, LSPs, TSPs PSPs, and everyone in between for OCEN to achieve its lofty ambitions.

OCEN Developer Community

Based on the interactions with the ecosystem over the past two months, iSPIRT would like to formally announce the creation of the OCEN Developer Community, whose role is to help build and share knowledge required to make OCEN a success for all participants. The specifications for OCEN can be found here.

The goal of this community would be to:

Help reduce the implementation cycles and turnaround times for OCEN APIs

Transfer learnings and best practices from those who are creating and maintaining the OCEN API specs to all the entities keen to implement and experiment with OCEN (LSPs, FIs, AAs etc)

Seek feedback from the developer ecosystem about what changes and/or improvements to make for future releases

Onboard enthusiasts and ‘super users’ to play a more hands on role in overall API creation and implementation

If you’re interested in contributing to this group and being part of the discussion, please log in to http://ocen.discussion.ispirt.in/. For any other questions on becoming an LSP, Technical Service Provider (TSP) or Lender, drop us an email at [email protected].

In case you are curious about other ongoing initiatives outside of OCEN, there are also communities for the Account Aggregator framework (discourse.sahamati.org.in) and National Health Stack (HealthStack.discussion.ispirt.in) that you are also welcome to join.

We know that an engaged developer community is key to ensuring that this initiative is conceptualised and executed properly. We welcome the participation of our talented developer ecosystem and are looking forward to working alongside you.

On 14th August we hosted the fourth open house session on Open Credit Enablement Network (OCEN). This week’s discussion focused on the different roles and market opportunities for ecosystem participants across the lending value chain.

To recap, OCEN (O-Ken) is a new paradigm for credit that seeks to provide a common language for lenders and marketplaces to build innovative, financial credit products at scale.

In last week’s session, we did a deep dive into the underlying OCEN API flows, covering different entity interactions in-depth and addressing common technical queries.

We began by highlighting the shift from balance sheet based lending to cash flow based lending that will be enabled by OCEN adoption. This upgraded methodology gives lenders a more holistic way to assess the creditworthiness of potential borrowers while allowing for more innovation in the kinds of products that can be offered to individuals and MSMEs.

OCEN is built around the idea that any service provider that interfaces with consumers and MSMEs can become a Fintech-enabled credit marketplace i.e. a Loan Service Provider. A key component to the success of this approach is that data from these digital platforms will reduce the information asymmetry between borrower and lender.

There is room for entities to play the role of Derived Data Providers by digesting this data (after obtaining user consent) and helping to inform the lender’s credit rules. Working alongside specialised Underwriting Modellers, these players can map the best the fit between lender and borrower, making for smarter underwriting.

OCEN is designed to enable many types of LSPs offering diverse ‘species’ of credit products. While the last three sessions have focused on MSME credit, this week our volunteers covered several use cases for individual consumers and service professionals. Principally these resemble the ‘Type 4’ loan products highlighted in earlier sessions where the end use for the loan is defined, and the repayment is locked into incoming cash flows.

Through the past few weeks one of our objectives has been to illuminate the range of opportunities for participants (both new and incumbent) to get involved in an OCEN-enabled lending process. Entities can provide value by bringing superior distribution, data, technology, or capital into the equation.

LSPs have an important role to play as ‘agents of the borrower’. Technology Service Providers (TSP) need to work with lenders, LSPs or both, helping them to successfully come onboard the OCEN protocol. Account Aggregators play the role of data fiduciaries, facilitating the consented sharing of financial information in real time. Payment Service Providers (PSP) provide a ready infrastructure for both the disbursement of loans and collection of repayments.

Even incumbent fintech lending marketplaces that have a ‘deep, tacit know-how of the lending domain’ can play multiple roles in the cash flow based lending value chain.

Finally, our volunteers talked about CredAll, which is a collective of lending ecosystem players to drive cash flow based lending. Participants interested in becoming an OCEN-enabled Lender or LSP can have a look through the suggested checklist and basic requirements for each.

The fourth session on OCEN covered the following topics broadly, and the entire webinar is also available on our official Youtube channel:

By Siddharth Shetty

An introduction to iSPIRT and our values

By Nipun Kohli

New cash flow based lending paradigm

Derived data providers

How DDPs and Underwriting Modellers can help assess the creditworthiness of potential borrowers

Types of lending products enabled by OCEN

Product example 1 (Consumer finance use cases like paying school fees or streaming charges)

Product example 2 (For service professionals)

By Ankit Singh

Opportunities for different stakeholders at various stages in the credit lifecycle

Different ways entities can add value

How an LSP is different from a DSA

5 D’s of value addition for LSPs

The role of Technical Service Providers (TSP), Account Aggregators (AA), and Payment Services Providers (PSP)

OCEN opportunity for incumbent fintech lending players

How to become an OCEN-enabled lender or LSP

After the presentation, our volunteers answered some questions from the community including:

How to think about constructing the right business models for LSPs and lenders?

Does a DDP always have to be an LSP?

What are the opportunities for existing fintech players?

What are the KYC implications for OCEN?

As always, in order to successfully create a new credit ecosystem for Bharat it will take the collaborative effort of participants from every corner of our fintech ecosystem.

Readers may also submit any questions about the OCEN to the same email address and our anchor volunteers shall try their best to answer these questions during next open house discussion (P.S: Time and Date is yet to be decided)

If you would like to know more about becoming an LSP, please check out www.credall.org (CredAll is a collective of lending ecosystem players to drive cash flow based lending)

“The ‘Landline to Mobile’ leapfrog for MSME credit is here.”

On Friday evening we hosted the first open house discussion on the new Open Credit Enablement Network (OCEN). It is the next chapter of the ‘India Stack’ story, one that has provided the building blocks for public digital infrastructure in our country.

The past decade has seen us widen the net for financial inclusion in India on the back of open infrastructure for digital identity (Aadhaar, eKYC, eSign) and payments (UPI, AEPS). This year will also see the launch of the Account Aggregator framework, ushering in a new era for data governance in India. Similarly, OCEN is a new paradigm for credit that seeks to provide a common language for lenders and marketplaces to build innovative, financial credit products at scale.

The first session on OCEN covered the following topics broadly

By Sharad Sharma

An introduction to iSPIRT and our values

An overview of India Stack and where OCEN fits in

By Siddharth Shetty

A product demo of Sahay, the reference app for OCEN

By Ankit Singh

The reason for the credit gap in India

The challenges for lenders and prospective credit marketplaces

A reimagined credit ecosystem with OCEN and Loan Service Providers (LSPs)

Access to credit is a crucial part of any flourishing economy. It is safe to say that India’s economic engine has not yet gotten out of second gear because of our inability to guide formal credit into the hands of the people and businesses that need it most. The unit economics of our current lending set-up are broken, and don’t suit the needs of either borrowers or lenders. The challenges range from high costs of customer discovery to lack of trustworthy data for underwriting, and an overall mismatch in ticket size, tenure and interest rates of loans. This has resulted in a whopping MSME credit gap of over $330 bn.

OCEN is an effort to recognise that the touchpoints for delivering financial products to individuals and MSMEs extends beyond traditional lenders. In order to democratize access to credit in India, OCEN reimagines an ecosystem where every service provider can become a Fintech-enabled credit marketplace.

This means that whether you’re an aggregator, a payment gateway, a software provider or any other company that interfaces with consumers, you can now fill in a crucial role in India’s lending value chain. OCEN will allow you to effectively ‘plug in’ lending capabilities into your existing product or service offerings, enabling you to play the role of a Loan Service Provider (LSP) in this framework.

At one end this will simplify and reduce the cost of acquiring and analysing new customers. Working in tandem with the Account Aggregator framework it will also allow applicants to leverage different data sources so that lending can become a Cash flow based operation instead of the existing balance sheet focus. Overall these open standards will enable lenders to accelerate the disbursal of formal credit while allowing LSPs to holistically serve their existing customers.

India’s new credit rails are ready to be laid out, and we look forward to working with our spirited fintech ecosystem participants over the coming months.

We will be hosting weekly open house sessions to keep diving deeper into OCEN.The next session will focus on Open Credit Enablement Network (OCEN) APIs at 5 pm IST on 31st July 2020.

Readers who wish to learn more about OCEN are encouraged to share this blog post and sign up again for the session here: https://bit.ly/LSPOpenHouse (same embedded below)

As always, in order to successfully create a new credit ecosystem for Bharat it will take the collaborative effort of participants from every corner of our fintech ecosystem.

Readers may also submit any questions about OCEN on the google form: https://bit.ly/LSPQA. We shall do our best to answer these questions during next Friday’s open house discussion.

About the Author: The post is authored by our volunteer Rahul Sanghi.

The DigiSahamati Foundation, the non-profit Self Regulatory Organization responsible for evangelizing the nascent Account Aggregator (AA) ecosystem, is organizing a hackathon featuring lots of masterclasses for the public to attend and learn from.

As a refresher, an AA is a new kind of legal entity defined in this RBI circular. The basic idea is that the average Indian today generates lots of financial data. Each credit card payment, sale of a mutual fund, repayment of a loan, and filing of an invoice generates some new data about users, be they individuals or businesses.

This data trail is actually very valuable – understanding a person’s financial activity can tell you a lot about that individual’s behaviour, preferences, and profile as a consumer. Today, banks use this data about customers to sell them various kinds of products (insurance, loans, savings products), and they also sell the customer’s data to marketers and advertisers. This is not necessarily a bad thing, as long as it happens in a secure way, with the customer’s consent and in such a way that the customer gets some value out of it too.

This is where the AA comes in. In today’s world, the customer doesn’t have any say nor cut of revenue when the bank shares their data with marketers. It is also difficult to extract the valuable financial data outside of a bank’s database to share with a third party provider such as a lender, insurer, or wealth manager. Until now, the only ways customers could get their data out of the bank today is through physical passbooks, downloaded PDF statements, or by giving access to their SMS/emails/netbanking account.

These methods are painful and unsafe, and they don’t help a customer get the best deals. If the customer could easily and cheaply move their data to third parties, then maybe they would get better interest rates and prices, and their existing bank would also have to offer more competitive products and pricing.

Fortunately, the banks and RBI have figured out that in order for India’s financial sector to really grow, individuals and companies need a more safe and efficient way to maximize the value of their ever growing data. This will not only benefit consumers, it will also result in a richer and more innovative banking landscape with a larger customer base. The AA is the entity which helps users give their consent to move data outside their bank account to a third party in a safe and easy manner. The customer gets to choose exactly what data to share, with who, for how long, and under what conditions. This consent is granularly programmable and revocable. Detailed information about this new system can be found on the Sahamati blog.

The AA framework is about to go live in the next months with some of the country’s largest financial institutions including SBI, HDFC, ICICI, IndusInd, Axis, IDFC First, Bajaj Finance, and others. Given this timing, Sahamati decided to organize a hackathon in order to spread awareness of this powerful new infrastructure.

The response so far has been excellent for them. More than 600 hackers were accepted to take part in this four-week long virtual hackathon. During these four weeks, participants in the hackathon will learn about all the different facets of this new technology, from UI/UX to security to product innovations in fields like lending, insurance, personal finance management, and more.

All of these masterclasses, as well as the final presentations by hackathon participants, are open to the public. The list of masterclass presents can be found here.

When reality changes, it’s important for the firms to acknowledge and adjust to the new situation. This is the time to remember the mantra ‘Revenue is Vanity, Profit is Sanity, Cash is Reality’.

The Covid-19 crisis is much written about, debated and analyzed. If there is one thing everyone can agree about on the future, it is that there is no spoiler out there for this suspense. The fact is that no one knows the eventual shape of the business environment after the pandemic ends.

When revenue momentum slows down or even hits a wall as it is happening in the current scenario, costs take centre stage even as every dollar of revenue becomes even more valuable for the firms. So, enterprises need an arsenal of strategic weapons to operate and survive, maybe even thrive, in this period of dramatic uncertainty. The same old-same old, push-push methods will not move the needle of performance.

As an entrepreneur and CEO, I have always found the theory of Marginal Costing (MC) to be practically powerful over the years. Let me tell you why.

At the best of times, MC is a useful tool for strategic and transactional decision making. In a downturn or a crisis, it is vital for entrepreneurs and business leaders to look at their businesses through the MC filter to uncover actionable insights.

Using MC-based pricing, the firm can retain valuable clients, win new deals against the competition, increase market share in a shrinking market and enhance goodwill by demonstrating dynamism in downmarket.

As the firm continues to price its products based on MC, the idea is to continually attempt to increase the price to cover the fixed costs and get above the Break-Even Point (BEP) to profitability. However, this happens opportunistically and with an improving environment.

Pricing for outcomes is more critical during these times and playing around with your costing models can go a long way in determining the most optimal outcome-based pricing approaches.

Steps to Get the Best Out of MC:

1. Determine bare minimum Operating level

Estimate the bare minimum operating level or fixed costs you will need to bear to stay afloat and capitalize on revenue opportunities. This is the BEP of the business. This estimate can include:

Facilities, machines, materials, people and overheads.

All R&D expenses required to support product development

Necessary support staff for deployment and maintenance of products/services.

2. Ascertain the variable costs

Identify the incremental costs involved in delivering your business solutions to fulfil contractual and reputational expectations to both existing and new customers. These costs are the variable costs in your business model. Try to maximize capacity to flexibly hire, partner or rent variable costs as needed, based on incremental revenues.

3. Distinguish between fixed costs and transactional variable costs.

Take your fixed costs at your operating level as costs for a full P&L period. Let’s say, the fiscal year. Take your variable costs as what it takes to fulfil the Revenues that you can book. Make sure you only take the direct, variable costs. Note that if Revenues less Variable costs to fulfil the revenues is zero, then you are operating at MC.

4. Sweat the IP already created.

For every rupee or dollar you earn over and above the MC, you are now contributing to absorbing the fixed costs. Do bear in mind that all historical costs of building the IP are ‘sunk’, typically to be amortized over a reasonable period. Hence, it doesn’t figure in the current level of fixed costs. The idea now is to ‘sweat’ the IP already created.

5. Peg the base price at marginal cost.

Start at the level of marginal cost, not fully absorbed costs. Then, try and increase the price to absorb more and more of the fixed costs. The goal is to get to BEP and beyond during the full P&L period. At the deal level, be wary of pricing based on the fully-loaded costs (variable and fixed costs, direct and indirect).

6. Close the deal to maximize cash flows

Price your product at marginal cost + whatever the client or market will bear to get the maximum possible advance or time-linked payments. This is a simple exchange of cash for margins wherever possible and an effective way to maximize the cash flows. Many clients, especially the larger ones, worry more about budgets than cash flow.

Let’s look at a high-level illustration.

Assume a software product company providing a learning and development platform to the enterprise marketplace. Let’s call this company Elldee.

Elldee has a SaaS business model that works well in terms of annuity revenues, steady cash flows and scale. Clients prefer the pay-as-you-model representing OpEx rather than CapEx. Investors love the SaaS space and have funded the company based on the future expectations of rapid scale and profitability.

However, given the ongoing crisis condition, Elldee needs to take a good re-look at the licensing model. By applying MC filters, it may make more market and financial sense to maximize upfront cash by doing a longer-term `licensing’ deal for the software-as-a-service at even a deep discount, with back-ended increments in price. The variable costs of on-boarding a client are similar to a SaaS deal yet the revenue converts to contribution to absorb fixed costs quickly to help survival and longer runway for future growth. So the client pays lesser than what they would have for a three year SaaS deal but Elldee is able to sweat its IP while maximizing cash flows.

Elldee can even move its existing SaaS clients to this model to capture more revenues upfront by being aware of MC and figuring out the right pricing models to get to the BEP of the business or product. Outcome-based pricing can also be designed to deliver margins beyond the MC, contributing to the absorption of fixed costs more aggressively.