iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

We are thrilled to announce that Open Credit Enablement Network (OCEN) has been conferred with the prestigious Digidhan 2021-22 award for their Special contribution to the promotion of Digital Payments. The award ceremony was held recently in New Delhi, organized by the Ministry of IT and Electronics, and was handed over to Sagar Parikh, the OCEN lead at iSPIRT, by the Honourable Union Minister, Mr Ashwini Vaishnav.

The Digidhan Awards recognize and celebrate the outstanding contributions made by individuals and organizations towards promoting and adopting digital payments in India. This year, the award was presented to OCEN for their revolutionary work in creating a standardized digital credit infrastructure that enables lending institutions to access and disburse loans digitally.

OCEN‘s platform acts as a bridge between lenders, borrowers, and other credit infrastructure providers, enabling them to interact with each other in a secure, reliable, and efficient manner. With OCEN, borrowers can easily access credit from multiple lenders, while lenders can easily verify the borrower’s identity, creditworthiness, and other relevant details before disbursing the loan.

The platform’s open architecture and standard APIs make integrating with OCEN easy for other credit infrastructure providers, creating a robust credit ecosystem that benefits all stakeholders. Moreover, OCEN’s platform ensures that all transactions are secure, compliant with regulatory requirements, and protect user privacy.

Speaking at the event, Sagar Parikh said, “We are honoured to receive the Digidhan award for our contribution to the promotion of digital payments. At OCEN, we believe that access to credit is a fundamental right, and our platform is designed to ensure that every Indian can access credit securely and efficiently. We are grateful for this recognition and will continue to work towards our mission of financial inclusion for all.”

The Digidhan award is a testament to OCEN’s commitment to promoting financial inclusion and enabling digital transformation in India’s credit ecosystem. The platform’s standardized infrastructure and open architecture have the potential to revolutionize the lending landscape in India, making it easier for borrowers to access credit and for lenders to disburse loans.

India has made rapid progress in digitisation of the economy in the last decade becoming a world leader in identity systems, digital payments and tax, and a new data sharing and empowerment framework. However, many deep-rooted issues still exist, such as extending true financial inclusion; formalisation and creating a higher trust economy, that is essential for growth of mostly small businesses.

In this blog post, we look at innovations in blockchain, distributed ledger and other technologies such as zero-knowledge proofs as potential solutions to build a stronger fabric for the economy for decades ahead. The unique opportunity India has is to boost commerce by enhancing trust, thereby culminating the transformation already underway through existing building blocks of digital identity, payments and data sharing to boost commerce. Unlike many other countries, faster and interoperable payments or reducing the dominance of private money are solved problems for India; the missing piece is to digitise commercial contract enforcement, which on the other hand is a solved problem for developed countries. Lack of adequate contract enforcement caused by contracting parties having different versions of the truth; due to data systems that don’t interoperate reduces trust and creates friction for economic growth. Solution requires connecting the goods and services ledger to the money ledger, so that contracts of any kind become binding promises that can be executed programmatically. Using technology to solve this trust problem is a unique opportunity for India.

BADAL (also happens to be a word for Cloud in local language), a techno-legal solution in the form of “Distributed Ledger for Privacy-preserving Trustful Commerce; is proposed as an interoperable fabric underlying a future programmable economy across large and small businesses to create high trust economy.

We also look at the emergence of Central Bank Digital Currency (CBDC) which is one of the core money applications of this framework and global backdrop in Annexure. There are many other use cases being proposed from land records to decentralised clinical trials for blockchain and allied technologies in different areas of government and business1https://www.meity.gov.in/content/national-strategy-on-blockchain likewise, that can be implemented in BADAL.

First of all, why is trust important?

Trust is the basic glue that connects strangers and promotes economic activity. Money is the basic economic institution in a society building that trust2https://press.princeton.edu/books/paperback/9780691146461/the-company-of-strangers. However, trust builds slowly due to a combination of various factors such as the nature of institutions (political and legal) and the level of formalisation. While formalisation of even small businesses is increasingly addressed by the successful rollout of GST for India, formalisation of trust still remains elusive. At a core fundamental level, trust is a public good that creates friction-free commerce and is a recipe for rapid economic growth.

There is a high correlation between the level of trust in society and GDP per capita3https://ourworldindata.org/trust-and-gdp. A study conducted by World Value Survey attempted to measure the level of trust in a country by recording the positive responses received to the question ‘most people can be trusted’. It found that countries with high GDP per capita such as Sweden, Norway and Netherlands recorded high levels of trust exceeding 60% determined in this manner as the graphic below shows.

Douglass C. North, Nobel laureate in economics4https://www.nobelprize.org/prizes/economic-sciences/1993/north/lecture/, found that ‘the inability of societies to develop effective, low-cost enforcement of contracts is the most important source of both historical stagnation and contemporary underdevelopment.’ The Union Minister of Finance and Corporate Affairs has rightly acknowledged the role of the “Hand of Trust”5https://pib.gov.in/PressReleasePage.aspx?PRID=1601273when presenting the Economic Survey of 2019-20.

In societies like India, with limited ability to efficiently enforce routine civil or property contracts, businesses tend to restrict working with those similar to them based on caste, religion etc. (called associational activity) where there is an implicit social and moral enforcement mechanism or with members who have clearly demonstrated reputation in the past (usually the large or the older players). In both these situations, the economic benefit that a new firm can bring with new ideas or new techniques will be muted as its absorption is slower. Similarly, a new player will find it very difficult to compete with incumbents even if such players are economically more efficient. Economist Olson6Olson, M. (1974). The logic of collective action. Harvard University Press showed that associational activity is often more detrimental than favourable for an emerging economy. So we need better ways to break this trust logjam. Trust in the money system in India is comparatively high, as promises tend to be kept with sufficient legal backing and can be digitised with e-mandates or automated payments/ collections; but the same is not the case for goods (or services) ledger, leaving room for delays cascading into a logjam resulting in low trust. This is often felt in day to day life by citizens not getting routine services despite advance payment or small businesses not getting paid despite having supplied goods. Delays, defaults and disputes can become the norm if parties have different versions of the truth.

Every economic activity is thus like a mini-contract with one side on the money ledger (payment from party A to B) and the other side, on the goods/services ledger (from B to A) between counterparties, and can be converted into an electronic contract that automatically executes on both ledgers subject to interoperability. To assure the performance of contracts, the money ledger and the goods/ services ledger need to be connected in a way that is scalable, privacy-enhancing, non-repudiable and programmable. This enables a contract agreed between parties becomes a commitment, and fulfilment is guaranteed by code through the electronic contract. Assuring performance of contracts is critical for a country that is seeking to grow through startup activity, not just in tech but other sectors too.

Currently, litigants lose nearly ₹ 50,000 crores annually in wages or business lost which comes to 0.5% of the country’s GDP, because of litigation, an indication of how expensive litigation can be. The majority of civil disputes in courts are related to recovery of money (30.2 per cent) and land-or property-related matters (29.3 per cent) As reported in the 2016 survey carried out by DAKSH. Common reasons for dispute are different versions of the truth of contracting parties, prior to contract (past) or during the performance of contract (future). Having the same truth and programmability inherent in electronic contracts is a boon in this regard.

In an earlier blog, we have explored the benefits of adapted blockchain technologies to solve the problem of SME financing in India with a related post by global experts7https://balajis.com/add-crypto-to-indiastack/. We build further on that and believe that India can harness recent advances associated with blockchain technology to enable trust between unrelated parties by combining the best of the scalable and centralized legacy world with a secure and private decentralized world. This can benefit the real economy vastly along with the financial world.

Innovations in distributed ledger technologies and BADAL

Distributed Ledger technology can help in two ways – first by being able to verify past performance before one party strikes a deal with another, and second, by being able to enforce a contract in most situations as performance unfolds in future. Thus, building trust about the past as well as the future.

We thus imagine a fabric based on the following basic principles to help create and grow a large number of applications to record economic activity even while reconciling with other activities and past data and help inject a level of trust by creating a reliable, immutable record of trusted data records and programmable contracts

Single platform to allow standards bodies and organisations to publish their schemas, and reuse other schema elements in composing workflows

Fully privacy-preserving capabilities to allow participants to publish relevant zero-knowledge proofs which do not require private data to be shared beyond the participating entities

A programmatic contracts capability that can help automatically carry out the relevant tasks as agreed on without any further manual intervention

By connecting a new digital money ledger (such as Central Bank Digital Currency, or stablecoins) with the new goods & services ledger, we envisage a boost to trust across economy and commerce. As such, BADAL is the first such framework we are aware of globally, uniquely suited to India’s needs, opportunities and strengths.

We have discussed the early version of this in detail in an earlier open-source document8https://github.com/iSPIRT/ppl, called Public Private Ledger. BADAL is thus a privacy supporting, trust enhancing mechanism of coordinating economic activity, and information recording and sharing. Originally this group started out of a process to explore the domain around and figure out the appropriate model to support CBDC, support data sharing between participants, and coordination and automation of event-based standing instructions across events in the goods and services ecosystem and/or money flow.

We then reviewed exciting developments in related areas first to understand their relevance given India’s unique needs. Blockchain technologies generally are seen to enable unrelated parties to trust each other and transact without depending on a central institution or intermediary. These technology innovations are around three key areas:

Maintaining immutability and integrity of data across the distributed ledgers of parties.

Governance mechanisms, especially for decentralised networks

The programmability of such transactions to allow automatic execution.

Public blockchain technologies like Bitcoin and Ethereum, on the other hand, are based on a philosophy of distrust of centralised institutions like Central Banks and are designed for unrestricted access and decentralised decision-making. But they have had to develop new approaches to contend with a few challenges, especially given the huge growth off late that see further wor:

The enormous consumption of resources to establish ‘proof of work’ that limits efficiency and scalability, leading to newer approaches

Exposing all transactions on these networks that generally do not allow sensitive data to be private on the key layer, is as critical for confidential business data as it is for personal data

Rise of many networks that are not interoperable with each other or with the mainstream economy, though some bridges do exist

May have ability to operate outside banking conduits and regulatory frameworks that challenges government’s sovereignty and financial stability through greater oversight has been coming recently

Research on amending throughput, reducing costs and enhancing privacy/auditability/KYC compliance has been ongoing at a rapid pace, especially over the last couple of years.

Despite these unresolved issues, Public blockchain-based tokens, so-called cryptocurrencies, NFTs etc have become an unregulated asset class, especially amongst the young rapidly given the ease of use, creating concerns on possible misuse as well as potential opportunities. We were also part of the recent consultation of the Parliamentary Committee on Finance on ‘Cryptoassets: Opportunities and Challenges’ and had shared with them some of our ideas above in our submission here9https://docs.google.com/document/d/e/2PACX-1vShkuTno_bSILFZPf-Cb_KNwwgM6A_6OgyRiASNS0tXB3ViriHztovrkL7sebiAC7O54y0uwQheTdin/pub.

Various solutions have been employed to address some of these challenges:

Permissioned blockchains, such as Hyperledger Fabric and Corda, allow only trusted parties to participate. Corda uses Notaries for verifying transactions. Such solutions have been successfully used in finance, supply chain, property rights, healthcare, education and e-governance

Zero-knowledge Proofs (ZKPs) allow proving/verification of specific aspects of data without actually making the data public

BADAL builds on the above primitives and is offered as an open and interoperable platform to enable money ledgers such as CBDC/stablecoin along with applications relevant for finance and commerce. This can be designed as a permissioned network relying upon a few regulated entities, and interoperable to ensure that its benefits are widespread and at much lower costs than permissionless systems. It consists of a private ledger that holds sensitive user data withaccess restricted to participating entities only, and a public ledger that contains notarised zero-knowledge proofs about transactions between users. It supports different schemas (configurations) that enable usage across different use-cases.

This programmability coupled with immutability akin to electronic contracts, allows applications in BADAL to be used to leapfrog the trust logjam, without diluting sovereign privileges of control of money given India’s stage of development. BADAL will thus establish provenance that helps establish credibility and reputation of transacting parties, proof of title/ownership of goods and assets, proof of the history of transactions including promises made and ambiguously defined and fulfilled; automatic execution of terms of contracts along with privacy as a fundamental right.

Historically, monetary accounting has solved for only one side of this metaphorical coin- the monetary value. All monetary systems denote a money value to any transfer of goods or services. BADAL, being a ledger that can record value in any domain, solves for the non-monetary aspect of the transaction. Integrated with electronic contracts for a variety of applications, BADAL will enable digital claims on non-monetary assets, including new age asset classes such as crypto assets, NFTs, where claims can be financialized and liquidated. An inherent promissory layer can be enabled into the current transaction mechanism. This extends to all data types, from land records to hospital quality service quality etc, rather than just transactions involving money and goods/ services.

The ability to connect any of the data types across domains can give rise to massive amount of efficiency gains with automated execution thanks to new data from machines like cars, consumer durables like refrigerators or health wearables coming from advances in IoT (Internet of Things), 5G, Imagine a use case of automated crop insurance with sensors that monitor weather from a satellite in space to moisture in soil etc. and deliver claim benefit to the farmer with zero friction in real-time.

One of the biggest problems BADAL could solve at bottom of the pyramid is financial inclusion in India. This is not only in the form of increased monetary transactions through it, but also the ability for MSME’s to gain cheaper credit. This is a possibility as MSME’s will find it easier to prove their liquidity and income to banks and other lenders due to the monetary traceability the system will provide. An increased ability to prove financial stability will lead to greater leverage for borrowers and more systemic trust for lenders. This increase in the systemic trust will not only lead to an increase in credit creation but catalyse an increase in money velocity in India as a whole.

In a subsequent blog post, we will detail the potential use cases; as well as preliminary design of a prototype of one sample use case that is being built currently.

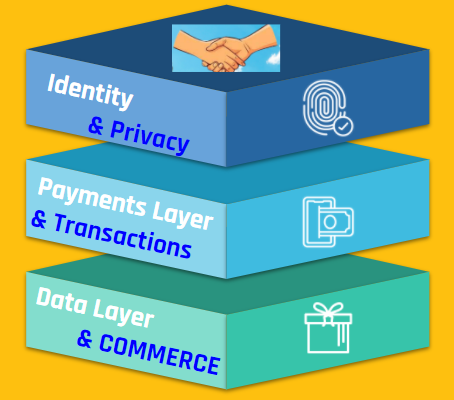

BADAL fabric supporting India Stack could boost digital India

India has pioneered transformations in Identity, Payments, and Data empowerment (these building blocks are popularly called the India Stack) through a techno-legal approach. These address friction of doing business, information asymmetry, and distributed systems. Breakthroughs along the way were public platform (identity), public protocols and standards, and techno-legal approaches to solving big societal problems.

The recent launch of the Account Aggregator (AA) model (based on Data Empowerment and Protection Architecture, DEPA) allows the controlled sharing of private financial data by citizens with various financial institutions to get the best deals. This is a global first and in some sense, an export of a truly global standard12https://twitter.com/Product_nation/status/1435997280692158464?s=20 from India.

Open Credit Enablement Network (OCEN) is creating a way to democratise access to credit, to the level of making it accessible to a street vendor for small sums. These public goods prevent any large player from monopolising the data ecosystem and at the same time reduce the cost of providing service. For instance, microloans as small as Rs.300 can be availed on GeM-SAHAY leading to true inclusion at the bottom of the pyramid.

These techno-regulatory concepts are now being considered for adoption by several countries across the world. Overall, India is arguably ahead of most countries in adopting technology for promoting financial inclusion as well13https://www.bis.org/publ/bppdf/bispap106.pdf.

Image Courtesy: Ananya Phadke

The next building block now is the trust layer through BADAL, ensuring every commitment is met and every contract is enforceable, boosting transparency and growth over the next decade. Trust permeates through all three ends of this triangle as identity is the ‘who’; and data and payment relate to ‘what’ of commerce. In BADAL, identity and data sharing can be achieved without diluting privacy to enable trusted payments (& commerce).

Annexure: CBDC Developments

While BADAL provides fabric to money or goods ledgers, we describe CBDC in detail here, given its importance. Money was traditionally issued by the sovereign (through a Central Banker) and circulated in the economy through layers of banking intermediaries. With the advent of permissionless public blockchains, some of which also seek to portray themselves as alternate currencies, the sovereigns have taken note and introduced their own variant as a public good to protect the financial stability of the nation-states. This sovereign/state-issued digital currency is popularly known as Central Bank Digital Currency (CBDC).

While there are different types of CBDCs such as wholesale/ retail and account-based/ token-based, ultimately a payment using CBDC can be immediately settled. This is akin to using paper money and unlike a cheque or money transfer between bank accounts that require a process of clearing and settlement adding to inefficiency and costs. CBDC can potentially thus leapfrog depending upon the development of existing banking systems in different countries.

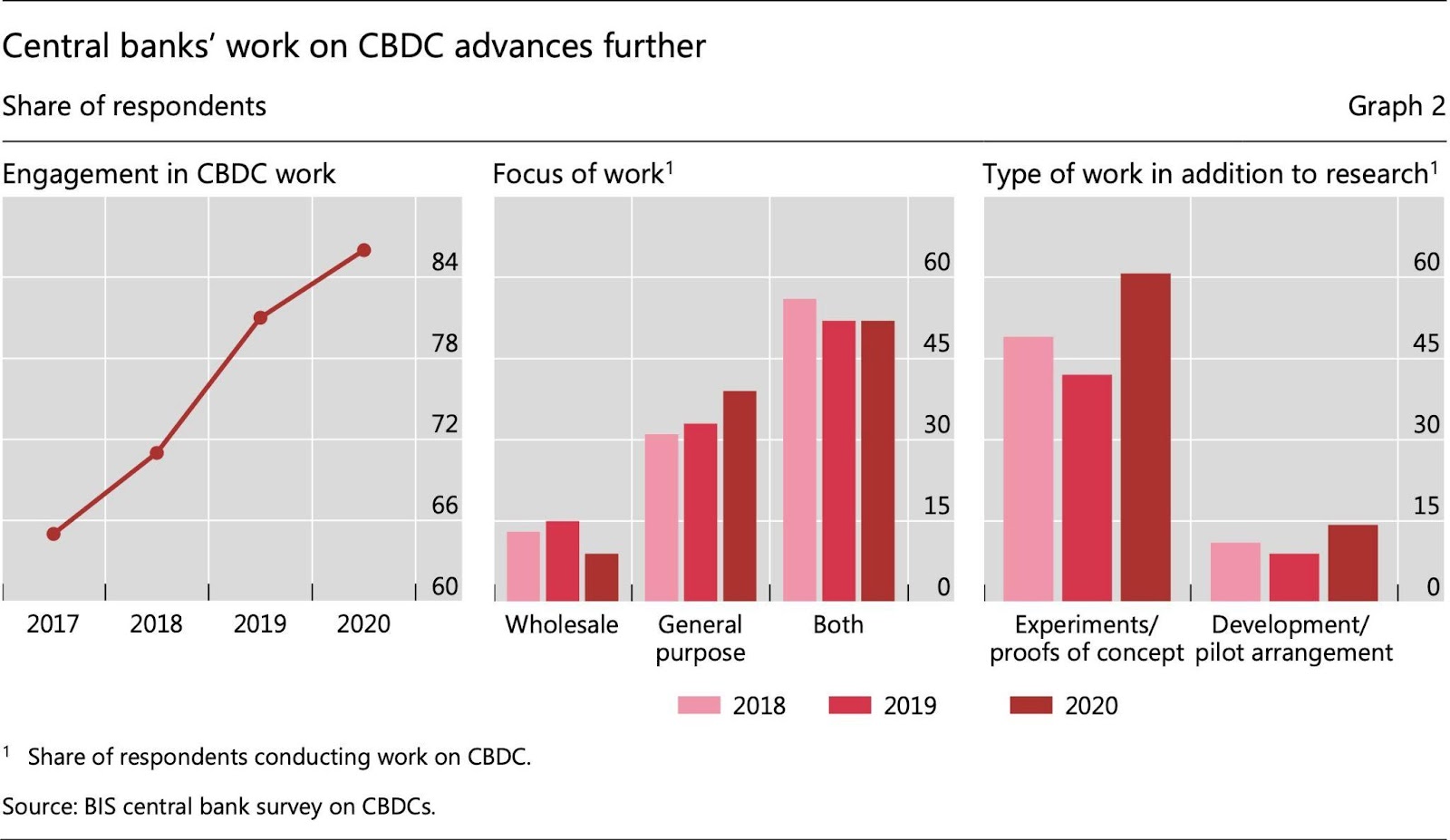

Advanced Economies (AEs) and Emerging Markets and Developing Economies (EMDEs) have different motivations for issuing CBDC to end-users (via Retail CBDC) and financial institutions (via Wholesale CBDC), illustrated in the diagram below.

In the USA, payments are expensive due to its legacy system of banking. This has led to a burst of digital payment options, the latest being ‘stablecoin assets’ (digital currencies backed by real assets like US dollar, treasuries, etc) that also compete with their money-market funds. Stablecoin assets have crossed $100 billion25https://www.statista.com/statistics/1255835/stablecoin-market-capitalization/ in market value and are a popular choice to transact in Decentralised Finance (DeFI). DeFi is a parallel financial system evolving around crypto-assets. DeFI is not subject to transparency and compliance required in the conventional financial world at this point in time. As DeFi becomes big and interacts with the conventional financial world, there is a growing systemic risk arising from failure or fraud in DeFi. The US Government, therefore, wants to regulate some aspects of DeFI26https://www.federalreserve.gov/monetarypolicy/fomcminutes20210728.htm and may thereby bless some stablecoins and crypto-assets as explicitly permitted financial products. Earlier in 2015, Bitcoin was determined to be a commodity27https://www.cftc.gov/sites/default/files/2019-12/oceo_bitcoinbasics0218.pdf by some authorities there. The US Fed has also begun a consultation process towards design choices and feasibility of CBDC implementation.

Indian perspective

In India, the focus of policy has rightly been on promoting financial inclusion to formalise the economy and drive economic growth. One important factor which drives the usage of unregulated informal value transfer systems is the lack of banking facilities and corresponding amenities for managing money, which leaves rural communities without alternatives other than a person-to-person method of transferring monetary value. Even though India has seen a significant increase in the number of bank accounts created, Reserve bank data still highlights little improvement in account usage and institutional borrowings, which feeds into the broader issue of financial inclusivity.

Initiatives like Pradhan Mantri Jan-Dhan Yojana (PMJDY) opened doors to big change. UPI has been very successful as a payment mode but still needs underlying bank accounts to transact and thus depends on the banking system & its motivation to provide access to the poor. The PMJDY scheme announced in 2014 has increased the number of adults with bank accounts to 43.47cr 28Progress Report as on 22-Sep-21, PMJDY, MOF, GOI, https://pmjdy.gov.in/account (~46% of 93.55cr adults with an Aadhaar29https://uidai.gov.in/images/Saturation_Report_State-UT_Agewise_31-08-2021.pdf). Despite this headway, there is still a lot to be achieved. The Financial Inclusion Index (FI) recently launched by RBI shows that India is at 53.9 on March 21 (vs 43.4 in March 2017) – a little more than halfway towards complete financial inclusion (FI of 100)30https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52068. Presently, the banking system acts as the main gateway to financial inclusion as the banking system is the main distributor of cash. Hence, various government programmes (like PMJDY) rely upon banks for financial inclusion, despite those being not remunerative for banks. The accounts also have various restrictions on the number of debits/withdrawals to ensure low cost.

Even with the existence of such low-cost bank accounts, the poor do not have an incentive to use a bank account regularly as they do not save enough to use the bank account as a store of value. They use these accounts mainly to collect remittances and withdraw cash at ATMs as bulk of their transactions is in cash, not leaving a visible money trail that in turn makes financial inclusion difficult. Cash in circulation in India even now is Rs 29.38 trillion31https://rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52274 (~14.9% of estimated GDP for 2020-2132http://mospi.nic.in/sites/default/files/press_releases_statements/Statement_12_1st+September+2021.xls) despite the availability of these cheaper accounts, demonetisation in 2017 and the subsequent formalisation of the economy with GST, RERA, etc.

In addition, the cost of handling cash by the central bank and commercial banks (currency printing, operating currency chests, logistics of moving currency, ATM operations, etc.) has been estimated to be ~Rs 21,000 cr (Rama Bijapurkar) and ~1.7% of GDP ( (Visa Inc., 2016). High adoption of CBDC can help in reducing this cost while creating enormous amounts of data and enabling policymakers to diagnose and regulate better. At a later stage, CBDC can also be used for targeted monetary policy actions when its impact on the financial system is well understood. Experts are concerned that CBDC may result in the disintermediation of the financial system. This risk can be mitigated by following design principles set out by the Bank for International Settlements (BIS)33https://www.bis.org/press/p201009.htm (i) “do no harm” to monetary and financial stability; (ii) coexist with cash and other types of money in a flexible and innovative payment ecosystem; and (iii) promote broader innovation and efficiency.

CBDC inherently provides an alternative to cash to directly reach a customer and can complement the banking network to make adoption quicker. By providing a digital alternative to cash will enable building verifiable money trails that can lead to greater financial inclusion by private players providing customised health, insurance, investment & education products in compliance with privacy laws. In the financially excluded segments, CBDC, being a form of central bank currency, is likely to be well trusted and be adopted easily.

The blog post is co-authored by Sanjay Phadke, Dhananjay Nene, Sharad Sharma, Navin Kabra, R Barve, K Babel, V Agarwal, K Gokarn, Kalyan Narguru, Shashank B, Arun Maharajan, Karan Sirdesai, P Sahu, P Rao, A Kulkarni, Krishna Iyer, V Nene and A Lath.

If you have any queries or comments, please contact us at [email protected].

On 14th August we hosted the fourth open house session on Open Credit Enablement Network (OCEN). This week’s discussion focused on the different roles and market opportunities for ecosystem participants across the lending value chain.

To recap, OCEN (O-Ken) is a new paradigm for credit that seeks to provide a common language for lenders and marketplaces to build innovative, financial credit products at scale.

In last week’s session, we did a deep dive into the underlying OCEN API flows, covering different entity interactions in-depth and addressing common technical queries.

We began by highlighting the shift from balance sheet based lending to cash flow based lending that will be enabled by OCEN adoption. This upgraded methodology gives lenders a more holistic way to assess the creditworthiness of potential borrowers while allowing for more innovation in the kinds of products that can be offered to individuals and MSMEs.

OCEN is built around the idea that any service provider that interfaces with consumers and MSMEs can become a Fintech-enabled credit marketplace i.e. a Loan Service Provider. A key component to the success of this approach is that data from these digital platforms will reduce the information asymmetry between borrower and lender.

There is room for entities to play the role of Derived Data Providers by digesting this data (after obtaining user consent) and helping to inform the lender’s credit rules. Working alongside specialised Underwriting Modellers, these players can map the best the fit between lender and borrower, making for smarter underwriting.

OCEN is designed to enable many types of LSPs offering diverse ‘species’ of credit products. While the last three sessions have focused on MSME credit, this week our volunteers covered several use cases for individual consumers and service professionals. Principally these resemble the ‘Type 4’ loan products highlighted in earlier sessions where the end use for the loan is defined, and the repayment is locked into incoming cash flows.

Through the past few weeks one of our objectives has been to illuminate the range of opportunities for participants (both new and incumbent) to get involved in an OCEN-enabled lending process. Entities can provide value by bringing superior distribution, data, technology, or capital into the equation.

LSPs have an important role to play as ‘agents of the borrower’. Technology Service Providers (TSP) need to work with lenders, LSPs or both, helping them to successfully come onboard the OCEN protocol. Account Aggregators play the role of data fiduciaries, facilitating the consented sharing of financial information in real time. Payment Service Providers (PSP) provide a ready infrastructure for both the disbursement of loans and collection of repayments.

Even incumbent fintech lending marketplaces that have a ‘deep, tacit know-how of the lending domain’ can play multiple roles in the cash flow based lending value chain.

Finally, our volunteers talked about CredAll, which is a collective of lending ecosystem players to drive cash flow based lending. Participants interested in becoming an OCEN-enabled Lender or LSP can have a look through the suggested checklist and basic requirements for each.

The fourth session on OCEN covered the following topics broadly, and the entire webinar is also available on our official Youtube channel:

By Siddharth Shetty

An introduction to iSPIRT and our values

By Nipun Kohli

New cash flow based lending paradigm

Derived data providers

How DDPs and Underwriting Modellers can help assess the creditworthiness of potential borrowers

Types of lending products enabled by OCEN

Product example 1 (Consumer finance use cases like paying school fees or streaming charges)

Product example 2 (For service professionals)

By Ankit Singh

Opportunities for different stakeholders at various stages in the credit lifecycle

Different ways entities can add value

How an LSP is different from a DSA

5 D’s of value addition for LSPs

The role of Technical Service Providers (TSP), Account Aggregators (AA), and Payment Services Providers (PSP)

OCEN opportunity for incumbent fintech lending players

How to become an OCEN-enabled lender or LSP

After the presentation, our volunteers answered some questions from the community including:

How to think about constructing the right business models for LSPs and lenders?

Does a DDP always have to be an LSP?

What are the opportunities for existing fintech players?

What are the KYC implications for OCEN?

As always, in order to successfully create a new credit ecosystem for Bharat it will take the collaborative effort of participants from every corner of our fintech ecosystem.

Readers may also submit any questions about the OCEN to the same email address and our anchor volunteers shall try their best to answer these questions during next open house discussion (P.S: Time and Date is yet to be decided)

If you would like to know more about becoming an LSP, please check out www.credall.org (CredAll is a collective of lending ecosystem players to drive cash flow based lending)

On 7th August we hosted the third open house discussion on Open Credit Enablement Network (OCEN). This week’s session featured a deep dive into the underlying OCEN API flows, covering different entity interactions in-depth and addressing common technical queries.

To recap, OCEN (O-Ken) is a new paradigm for credit that seeks to provide a common language for lenders and marketplaces to build innovative, financial credit products at scale. In last week’s session, we shed light on several potential Loan Service Provider (LSP) products and business cases. We also talked about the various opportunities for ecosystem participants across an OCEN-enabled cash flow lending value chain.

This week we dove into the API flows that make up the standardised end-to-end process of applying for a loan via an LSP, also illustrating how Account Aggregators will fit into this reimagined value chain. Our volunteers also covered the role of CredAll which is a collective of lending ecosystem players to drive cash flow based lending.

The third session on OCEN covered the following topics broadly, and the entire webinar is also available on our official Youtube channel:

By Siddharth Shetty

An introduction to iSPIRT and our values

By Ankit Singh

Recap of what OCEN is, and how LSPs fit in to the framework

Query 1: Is OCEN aggregating and sending loan applications to different lenders or does LSP make API requests with each lender separately?

Query 2: Are all API calls asynchronous? Are there Turnaround Time SLAs for the different services?

Query 3: Architecture diagrams – General LSP and Sahay GST

By Sudhanshu Shekhar

Query 4: API flow sequence diagrams

Query 5: How do I represent other loan products?

By Ankit Singh

Query 6: Using OCEN APIs and becoming an LSP

CredAll – a collective of lending ecosystem players

After the presentation, our volunteers answered some questions from the community including: – What is the role of LSPs in the collections process? – What is the difference between an LSP and a TSP? – How does the Common Pledge Registry fit in?

We will be hosting weekly open house sessions to keep diving deeper into OCEN. The next such event will take place at 5pm on 14 August 2020.

Readers who wish to learn more about OCEN are encouraged to share this post and sign up now for the session below or click here.

As always, in order to successfully create a new credit ecosystem for Bharat it will take the collaborative effort of participants from every corner of our fintech ecosystem.

Readers may also submit any questions about the OCEN to the same email address. We shall do our best to answer these questions during next Friday’s open house discussion.

If you would like to know more about becoming an LSP, please check out www.credall.org (CredAll is a collective of lending ecosystem players to drive cash flow based lending)

On 31st July we hosted the second open house discussion on Open Credit Enablement Network (OCEN). This week’s session covered several potential Loan Service Provider (LSP) products and business cases, and answers to questions that came up following last week’s introductory presentation.

To recap, OCEN is a new paradigm for credit that seeks to provide a common language for lenders and marketplaces to build innovative, financial credit products at scale. OCEN seeks to reimagine the lending ecosystem so that any service provider that interfaces with consumers and MSMEs can become a Fintech-enabled credit marketplace, or more specifically, a Loan Service Provider.

The discussion this week centred around what kind of role LSPs could play in an OCEN-enabled cash flow lending value chain. OCEN APIs can enable lending products for both consumers and businesses, and for both capital and operating expenses. They are designed to allow for several different types of LSPs and financial products to flourish.

To build this new credit economy, we need to move from the ‘Lend and Forget’ mindset of traditional lenders to the holistic ‘Lend, Monitor and Collect’ model allowed by the myriad of service providers and marketplaces in our tech ecosystem. These platforms not only have insightful data into their user’s commercial activity but they have an ongoing interface and interaction with potential borrowers.

With OCEN standardisation, LSPs can improve and contribute to all the five aspects of lending i.e. acquisition, underwriting, ROI, collections and monitoring. Tailored credit products can be plugged in at every stage in a typical supply chain (from ‘Procurement to Pay’) to help ease liquidity concerns and ensure business continuity.

Our volunteers illustrated this with two examples: 1) A seller on the Government e-marketplace (GeM) obtaining invoice financing through the Sahay GeM LSP

2) A truck owner availing of Business-Vehicle Trip Financing through a logistics company performing the role of an LSP

OCEN is also enabling the creation of a new type of credit product that is digitally applied for and disbursed, where the end use of the loan is identified and paid for, and where repayment of the loan is enabled by the locking of incoming cash-flow.

Every participant in our fintech ecosystem is incentivised to take part in this new open credit economy enabled by OCEN. There is an opportunity here for lenders, service providers, aggregators and tech providers to all play their role in bridging India’s credit gap and giving our people and businesses the support they need.

The second session on OCEN covered the following topics broadly, and the entire webinar is also available on our official Youtube channel:

By Siddharth Shetty

An introduction to iSPIRT and our values

By Ankit Singh

Recap of what OCEN is, and how LSPs fit in to the framework

Recap of Sahay, the reference app for OCEN (and the first LSP)

Becoming an LSP (and the role of CredAll)

By Nipun Kohli

Examples of different cash-flow-lending products enabled by OCEN

Key differences between traditional lending and credit products on OCEN

How LSPs can participate across the lending value chain

‘Procurement to Pay’ credit products

Product example 1: GeM – Procurement to Pay

Product example 2: Business-Vehicle Trip Financing

By Praveen Hari

Building new credit products on OCEN

The Type 4 loans

After the presentation our volunteers answered some questions from the community including: – How is Sahay different from TReDS? – How does the underwriting take place for LSP-enabled loans? – How can risk be managed between the LSP and the lender?

We will be hosting weekly open house sessions to keep diving deeper into OCEN. The next such event will take place at 5 pm on 7 August 2020

Readers who wish to learn more about OCEN are encouraged to share this post and sign up now for the session below or click here.

As always, in order to successfully create a new credit ecosystem for Bharat it will take the collaborative effort of participants from every corner of our fintech ecosystem.

Readers may also submit any questions about the OCEN to the same email address. We shall do our best to answer these questions during next Friday’s open house discussion.

If you would like to know more about becoming an LSP, please check out www.credall.org (CredAll is a collective of lending ecosystem players to drive cash flow based lending)

About the Author: The post is authored by Rahul Sanghi