iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

In our most recent OpenHouse, we embark on an insightful exploration of the transformative landscape in MSME lending, featuring Bhavik Vasa, the Founder of GetVantage, and Sagar Parikh. The conversation delves into the potential of creating groundbreaking impact through interoperable networks, particularly focusing on OCEN. The discussion navigates the dynamic intersection of finance and technology, highlighting how inventive solutions are reshaping the lending panorama. Emphasizing the crucial role of interoperability, the dialogue underscores its significance in bridging the credit gap, propelling the MSME sector into a new era of unprecedented growth.

Key Takeaways:

Network Effects Unleashed: OCEN catalyzes network effects, narrowing the credit gap and expanding the market, fostering inclusivity and vibrancy.

Efficiency through Interoperability: Standardized protocols cut costs and efforts, providing high-quality data for lenders while empowering MSMEs with smoother access to loans.

Addressing Unmet Needs: Explore how interoperable networks bridge gaps in unsecured lending, catering to shorter tenures and smaller loan sizes.

Tech-Enabled Business Growth: Witness the role of unsecured lending in a tech-driven landscape, fostering a circular consumption economy for economic growth.

Personalized FinTech Solutions: Bhavik advocates for a borrower-centric approach, urging lenders to view lending through a tech and data-driven lens, benefiting both parties.

Collaboration Dynamics: Conclude with insights on how NBFCs and banks can coexist and collaborate, playing to their strengths for a more robust lending environment.

Ready to unlock the future of MSME lending? Join the conversation now!

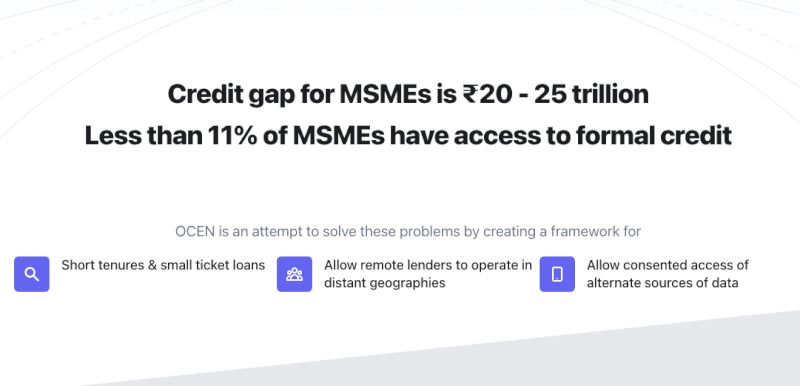

Intermediaries and Fintechs have played an important role in the lending ecosystem, but the impact is mostly seen in consumer lending and not so much in MSME lending, especially for unsecured, small ticket and short duration loans. What are the missing pieces in the lending process for which advanced tech and a mindset shift can utilise a digital infrastructure like OCEN (Open Credit Enablement Network) and unlock this credit supply for MSMEs?

Recently, we hosted Lizzie Chapman in an insightful conversation with Sagar Parikh. She shared her views on where the intermediaries and FinTechs can further become a value add in a profitable manner by pushing the boundaries of technology.

Points discussed:

Digital infrastructure & its impact on the costs, penetration & process for lending eco-system

Unsecured MSME loans not as solved as unsecured consumer loans. Cashflow lending addresses the concerns around unsecured lending to MSMEs.

DPI such as OCEN facilitating the availability, quality, aggregation of data for credit underwriting along with loan disbursement for MSMEs

Need for Intermediaries & Fintechs to harness technology to conceptualise innovative lending products, advanced ways of pricing and matching risks & address the opex challenges in collections & repayments

Investors tend to prefer businesses that touch the customer end to end. They should see that being part of the value chain can be as profitable as owning the value chain.

OCEN is creating dispute resolution mechanisms but intermediaries should also innovate for transparency and building trust with the customers so as to enable a safe, stable, secure growth in short term cashflow lending for MSME credit.

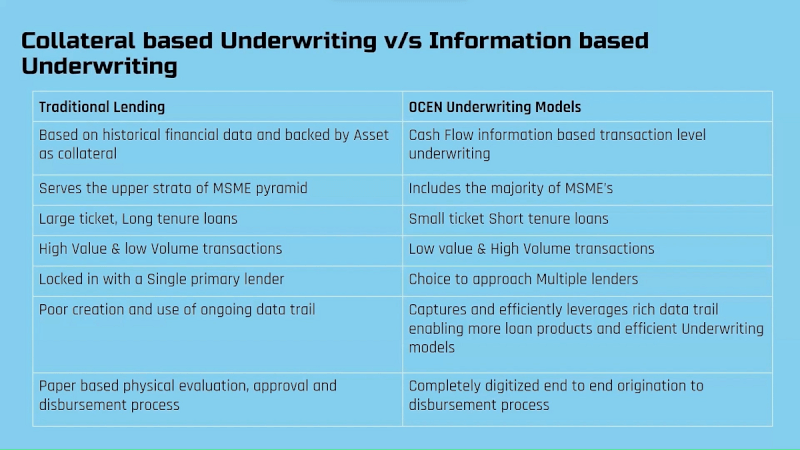

In an era of evolving financial landscapes, the realm of lending is witnessing a significant shift—from the traditional collateral-based approach to the more contemporary cash flow lending model facilitated by OCEN (Open Credit Enablement Network). Recently, we hosted UGro Capital in an insightful conversation with Shachindra Nath, shedding light on this transformative paradigm in lending and delving into its profound implications.

Points discussed:

Transitioning from Collateral to Cash Flow Lending

OCEN plays a pivotal role in revolutionising MSME lending in India. This innovative open network is specifically designed to serve those new to credit, employing an omni-channel approach that democratises and simplifies access to lending.

Currently, the market lacks a scalable and profitable model for short-term, low-value MSME loans – a significant gap that OCEN has adeptly filled with itsGeM-SAHAY pilots.

Amidst the confusion and excitement surrounding OCEN versus ONDC, and the broader impact of open networks in the lending sphere, this blog aims to provide clarity and insight. Let’s dive in and explore these transformative developments.

🔀 OCEN or ONDC: Which is better for short tenure MSME lending?

There’s much debate about which lending framework potential partners should explore. Rahul Mathur (Associate Director, InsuranceDekho) captures this perfectly in his tweet, presented as a checklist below:

🗣️ “Turns out, the focus in lending for ONDC v/s OCEN is very different (see the

image below)

(1) 💰Type of loan: Type 1 personal loan v/s Type 4 MSME loan

(2) 🔎GTM: Online v/s Omni-channel (assisted)

(3) 🙇Persona: Eligible for credit v/s New to credit

(4) 🌟Objective: Bring credit to point of commerce v/s Democratize credit access

To summarize, there are some good reasons why ONDC has launched loans

independently of the OCEN network.

Over time, OCEN will expand to include further lending use-cases & products.

And, at that point, ONDC <> OCEN interoperability would make sense.”

Clearly, OCEN is the undisputed option for short tenure, low ticket size lending for new to credit MSMEs. Over time the lending use cases will be expanded to service the traditional form of loans.

OCEN and ONDC, while both operating in the lending space, are tailored for very different use cases and audiences. While they may overlap in some cases, the larger ecosystem benefits from introduction of newer networks. In the end, it’s all about solving the most challenging problems 🙂

Let’s further understand how OCEN addresses the MSME lending problem in India.

📈 OCEN makes small ticket size lending a reality

OCEN’s primary goal is to make short-term lending profitable. Something which we’ve achieved in our pilots with the Government e-Marketplace, through the GeM-SAHAY app.

One of our volunteers explains the economics in this blog post:Evaluating the short term lending opportunity, where he shows how lenders can earn 2.2x higher revenue with the same capital through the adoption of the OCEN framework.

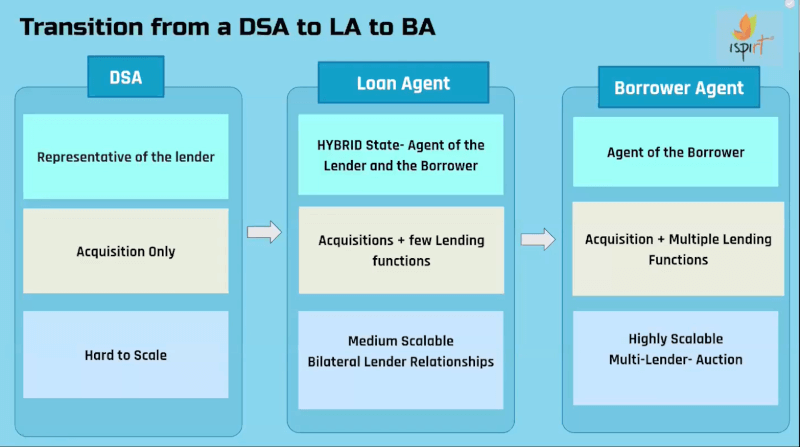

The significant 2.2x increase in revenue is attributed to the introduction of a crucial role known as the borrower’s agent. These agents not only reduce the cost of servicing a loan but also heighten accountability within the system.

Borrower’s Agents (BAs) assume a variety of roles traditionally outsourced by lenders, BAs function as data providers, collections agents, escrow account managers, and product providers.

By integrating these services and cohesively binding the network, BAs enable lenders to efficiently service low-cost loans even in remote areas. In performing these four key roles, the borrower’s agent emerges as the cornerstone of the open network, vital for its effective operation.

The role of borrower’s agent has been discussed in depth in one of our open house sessions:

OCEN is changing the game by making even the tiniest loans worthwhile for both the lender and the borrower.

🌐 Efficacy of Open networks and streamlining the lending process

Some people we’ve spoken to, worry that open networks will lead to the commodification of lending, which, in turn, is bad for the overall market. However, this couldn’t be farther from the truth 🙂.

OCEN streamlines the lending process by introducing roles such as the borrower’s agent, KYC agents, and collection partners. These roles combine to create a bundle that lenders can easily integrate into their processes to start lending.

Newer and smaller lenders will benefit from the transparency and scale offered by open networks.

Closed network auctions, which are common today, see lenders bidding down for loans. However, their lack of transparency and scale often results in low profitability.

Open networks, on the other hand, provide scale and transparency that leads to low cost of servicing, more borrowers to choose from, and reliability in the system through a borrower’s agent.

Larger lenders benefit from the low cost of servicing a loan that comes with open networks

Larger lenders will benefit from open networks as it provides the technical chops of a borrower’s agent. BAs can help with KYC, collections and other parts of servicing a loan while absorbing some of the costs.

We’ve seen such effects before, with the introduction of Aadhaar and UPI, where KYC and collections became far cheaper enabling large lenders to facilitate smaller ticket size loans.

In conclusion

Through OCEN, the potential to unlock a ~$300 billion credit market in India becomes a tangible reality. This is demonstrated by the increased revenue potential and the introduction of the borrower’s agent role, enhancing loan servicing efficiency and accountability.

Moreover, OCEN’s streamlined lending process benefits the entire market, by offering scalability and cost-effectiveness to both emerging and established lenders.

Thus, embracing OCEN is not just a choice but a strategic direction for expanding market possibilities and empowering both lenders and borrowers in the dynamic credit landscape of India.

📢Calling all lenders to understand how a short tenor loan can become both an effective and profitable business opportunity under OCEN 4.0. 🔑📈

If you are a lender looking for the next big opportunity in lending to the thousands of MSMEs currently unable to access loans, then don’t miss this introduction to OCEN 4.0. 💡

Here we deep-dive into how a new underwriting model enabled by OCEN 4.0 makes it viable and profitable to provide loans to MSMEs traditionally considered unfavourable candidates for loans given the associated high delinquency rates. Our OCEN pilots show, in some cases, it is even possible to create short tenor loans that are twice as profitable as long tenor loans. 🌟🚀🚀

📢Calling all loan agents keen to understand the OCEN 4.0 business opportunity. 🔑📈

OCEN 4.0 introduces a new and powerful role – the Borrowers Agent(BA). If you are looking to play a pivotal role in the MSME lending ecosystem without lending from your own balance sheet, this new role of a BA may be what you want to understand really well. 💡

The BA role is critical to the OCEN story. In this session, we deep-dive on what this role entails, why it is the linchpin of the OCEN 4.0 model, how BAs enable lenders to go remote, and how this role wields a lot of power. We also talk through how to get started, possible business models for BAs and what to focus on to be a successful Borrowers Agent. 🌟🚀🚀

📢👷🧑💻Calling all TSPs and participants eager to dive into OCEN 4.0 APIs.

If you are wanting to understand the tech, the APIs and get started on building for OCEN 4.0, our second open house on OCEN 4.0 is here for you !! 💡

In this session, we do a deep-dive on the architecture, the loan journey on OCEN 4.0 components, the APIs in the OCEN spec and share how you can build for a participant by mocking the APIs of the other. 📝🔑🧑💻

We’re thrilled to unveil OCEN 4.0, the latest advancement in our Open Credit Enablement Network protocol, revolutionizing cash flow-based MSME lending. 🌟

OCEN 4.0 represents a significant leap forward from our ongoing GeM SAHAY and GST SAHAY pilots. In this iteration, along with updated API specifications, we have also added the OCEN Registry, Product Network and rules, specialized participant roles and much more. All these features help us unlock cash-flow-based lending to match the scale, complexity and needs of Bharat. 🔑📈

Check out our introductory open house session on OCEN 4.0

🔍 More details? The API and documentation of OCEN 4.0 are publicly available at http://ocen.dev and will be updated with FAQs from the open house sessions.

🔮 What’s next? Yes, a lot is happening. We have more open house sessions coming out in the following weeks. We are also actively onboarding Wave 1 partners for OCEN 4.0.

❓Questions? Submit your questions here. 📩Contact? Reach the OCEN 4.0 team at [email protected]

Please note: The blog post is authored by our volunteers, Aravind R andSagar Parikh.