The calendar year 2025 has been a transformative period for the Open Credit Enablement Network (OCEN), evolving from a digital protocol into a powerhouse for financial inclusion. During 2025, OCEN successfully facilitated approximately 70,000 loans, resulting in over ₹1,600 Crore in disbursements.

This journey is not just about the numbers; it is about proving that a digital-first, cash-flow-based approach can solve the long-standing credit gap for underserved MSMEs with unparalleled efficiency.

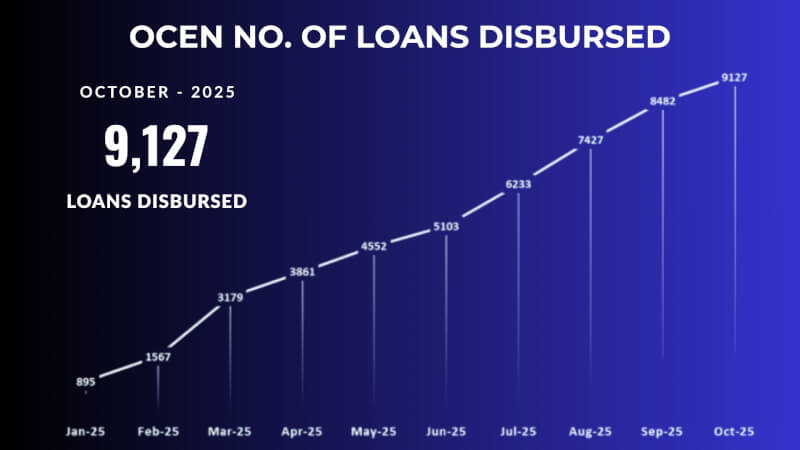

A Year of Relentless Monthly Momentum

The 2025 journey began with a steady climb and rapidly escalated as more lenders and borrower agents integrated into the ecosystem. The monthly growth in the number of loans disbursed showcases a consistent upward trajectory. This steady monthly rise provided the foundation for the explosive quarterly growth that defined the year.

Consistent Quarterly Growth (QoQ)

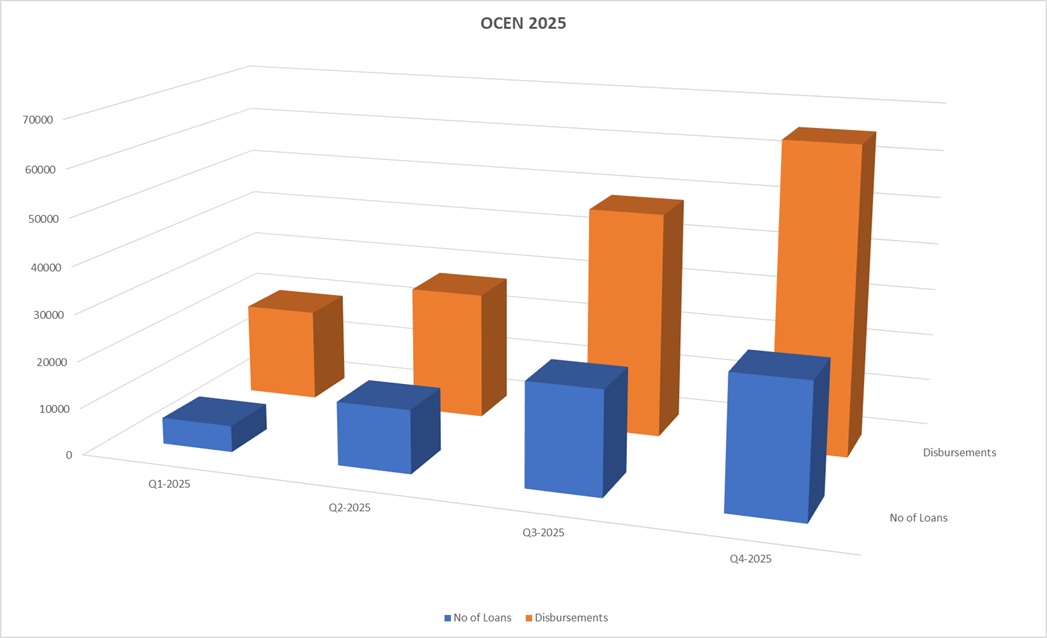

When looking at the 2025 performance on a quarterly basis, the scale of adoption becomes even more evident. The network didn’t just grow; it accelerated every three months.

| Period (2025) | No. of Loans | Disbursements (₹ Lakhs) |

| Quarter 1 | 5,641 | 19,795 |

| Quarter 2 | 13,516 | 27,316 |

| Quarter 3 | 22,142 | 48,092 |

| Quarter 4 | 28,122 | 65,275 |

The jump from Q1 (5,641 loans) to Q4 (28,122 loans) represents an increase of nearly 400% in loan volume within a single year. Similarly, disbursements surged from ₹197.9 Crore in Q1 to over ₹652.7 Crore in Q4, demonstrating the massive appetite for small-ticket, short-tenure credit.

Portfolio Quality: The Ultimate Validator

The most significant achievement of 2025 isn’t just the volume—it’s the quality of the credit. Traditional MSME lending often suffers from high risk and significant non-performing assets (NPAs). OCEN has fundamentally challenged this narrative.

Participating lenders have seen highly encouraging results in portfolio health, characterized by strong performance, minimal portfolio losses and high confidence. The cash-flow-based underwriting model allows lenders to assess real-time business health rather than relying on stale collateral documents. Data-driven, short-tenure lending ensures high repayment rates.

The Future is Cash-Flow Based

OCEN’s 2025 journey proves that when you align technology with the actual business cycles of small enterprises, everyone wins. MSMEs get the “just-in-time” capital they need, and lenders gain access to a high-quality, low-risk asset class. With over ₹1,600 Crore disbursed in 2025, the protocol has set a new benchmark for how India can democratize credit and fuel the next wave of economic growth.

For more information, please visit: http://ocen.dev

Please note: The blog post is authored by our volunteer, Rahul Bhaik