Financial ecosystems are rarely transformed overnight. Instead, they evolve through the steady

alignment of technology, policy, and trust. Over the past year, the Open Credit Enablement

Network (OCEN) has been moving quietly in this direction, acting as a digital bridge between

credit-starved MSMEs and a diverse pool of lenders.

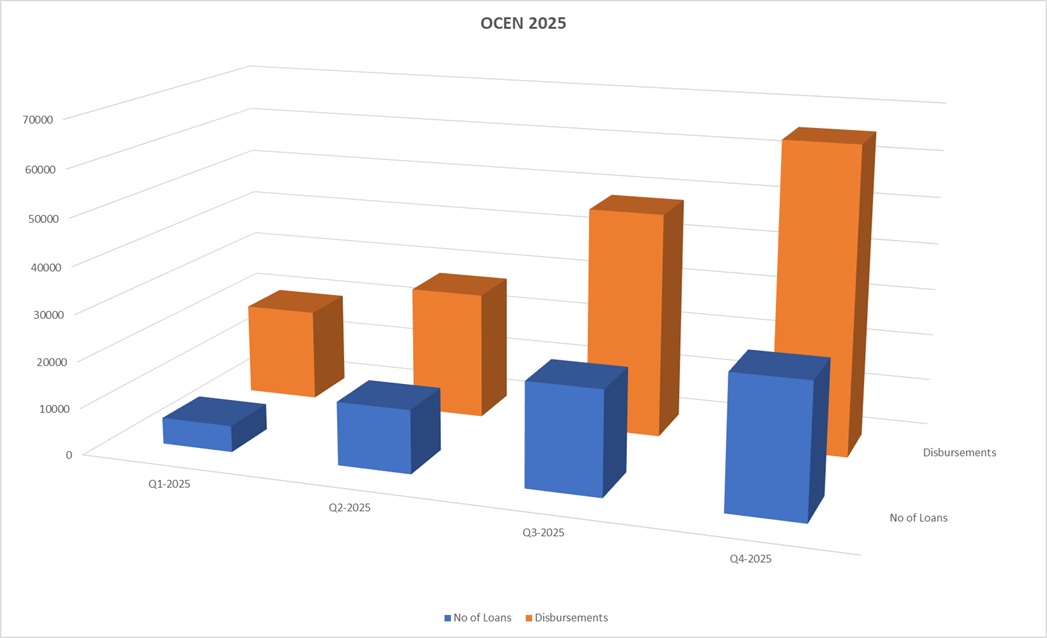

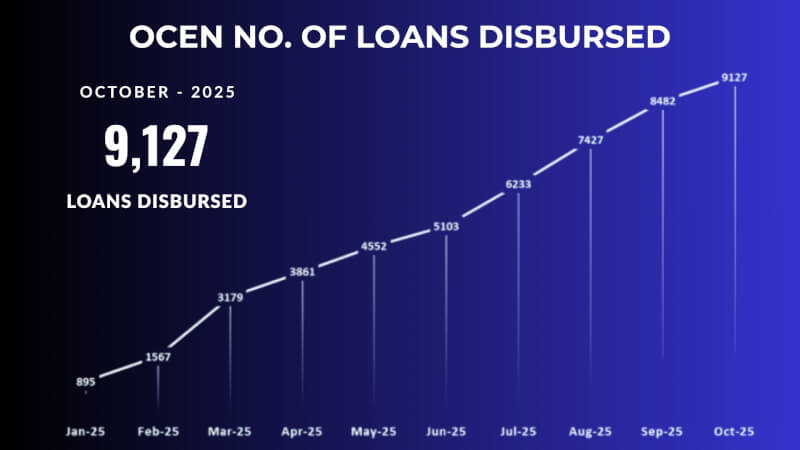

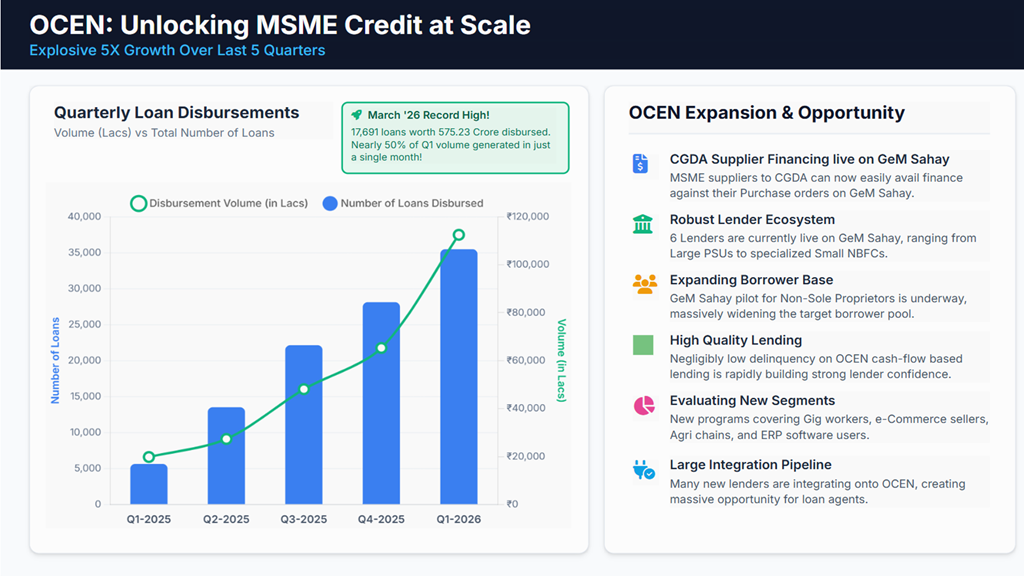

The Growth Narrative: In Q1-2025, the network facilitated 5,641 loans totaling 19,795 Lacs.

Fast forward to Q1-2026, and the momentum has scaled to 35,485 loans with a disbursement

value of 112,484 Lacs. This represents a 468% surge in disbursement value—a testament not to

the protocol alone, but to the readiness of the Indian MSME to embrace digital, cash-flow-based

credit.

Strengthening the Foundation

Beyond the numbers, the structural progress of the ecosystem offers a glimpse into a more

inclusive future. Today, six diverse lenders—ranging from large Public Sector Undertakings

(PSUs) to agile NBFCs—are live on GeM Sahay and many others in the process of integration.

This diversity ensures that credit is not a ‘one-size-fits-all’ product but is tailored to the risk

appetite and specific needs of the borrower.

The horizon is also widening. We are currently piloting programs for Non-Sole Proprietors on

GeM Sahay, significantly expanding the eligible borrower base. Furthermore, MSME suppliers to

the CGDA can now avail finance against Purchase Orders via GeM Sahay, marking a critical step

in supporting those who serve our national interests.

The Quality of Growth

A frequent concern in rapid credit expansion is delinquency. However, OCEN’s emphasis on

cash-flow-based lending rather than traditional asset-based collateral has yielded encouraging

results. To date, lenders have observed negligibly low delinquency across programs, proving that

data-backed lending to the ‘unbanked’ is not just a social imperative, but a sound financial

strategy.

Looking Ahead: An Invitation to the Ecosystem

The journey has only just begun. We are actively developing programs that touch every corner of

the economy:

- Micro-MSMEs: Providing vital credit to the gig economy and individual workers.

- Agri & Dairy: Strengthening the backbone of rural commerce through value-chain

financing. - Digital Sellers: Empowering e-commerce marketplace sellers and MSMEs using modern

ERP/Accounting software. - Regional Clusters: Addressing the unique needs of localized industrial hubs.

For lenders, platforms, and technology providers, OCEN represents a unique opportunity to

participate in a high-growth, low-friction credit market. As we move forward, we remain

committed to a humble approach—learning from the data, listening to our partners, and ensuring

that every disbursed Rupee contributes to the broader story of India’s economic resilience.

OCEN: Empowering Growth, One Transaction at a Time.

For more information, please visit: http://ocen.dev

Please note: The blog post is authored by our volunteer, Rahul Bhaik