iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

In just a decade, India has redefined how nations can harness technology for the public good. Through Digital Public Infrastructure (DPI), such as Aadhaar, UPI, and Account Aggregator, followed by newer innovations like OCEN and ONDC, India has shown the world how open, interoperable, and inclusive digital systems when designed as privately provisioned, public infrastructure; can spark innovation, scale rapidly, and empower communities at the grassroots.

To capture these lessons and provide a practical guide for policymakers, technologists, and global stakeholders, iSPIRT Foundation has contributed to the development of the DPI Handbook: Foundations of Digital Public Infrastructure. This handbook distills a decade of India’s pioneering experience into actionable insights, frameworks, and design principles that can help other nations build their own inclusive and interoperable DPI. The paper is now published on the Research and Information System for Developing Countries (RIS)

This Handbook is not the product of a single author, but rather the culmination of years of dedicated volunteerism at iSPIRT, where technologists, policymakers, entrepreneurs, and thinkers came together to exchange ideas, build prototypes, and debate design choices. Each page reflects this collaborative spirit, proof that when diverse minds work in concert, they can create frameworks that transform entire societies.

We extend our deepest gratitude to the iSPIRT volunteer community, past and present, whose passion and commitment, have been instrumental in shaping India’s DPI journey. Their contributions embody the ethos of building digital public infrastructure as a shared national mission.

We hope the DPI Handbook becomes both a guide and an inspiration, for nations building their own digital public infrastructure, and for all who believe that technology, when designed for the public good, can change the course of societies.

Please note: The blog post is co-authored by our volunteer, Arun Iyer

iSPIRT would like to extend its gratitude to Shri. Rajeev Chawla – IAS, Strategic Advisor and Chief Knowledge Officer- Ministry of Agriculture & Farmer’s Welfare who co-authored this Handbook, for his insightful perspectives. We would also like to thank Shri. Sachin Chaturvedi, Director General – RIS for graciously writing the Preface to this Handbook

iSPIRT volunteers are strivers. We seek the good for our nation and our ecosystem. We brainstorm, ideate, experiment, build, and evangelize to fulfill our mission of making India a Product Nation. Every volunteer draws us into an ever-enlarging realm of intellectual possibilities and purposeful engagements.

Take Nikhil Kumar for instance. He stepped up almost two years ago to evangelize UPI and handhold its early adopters. He set out to create winning implementations that would put traditional payment systems to shame. Needless to say, this wasn’t an easy thing to do. There was no template to follow. And, most didn’t believe in the potential of this new breakthrough payment system. But this didn’t faze Nikhil. He had chosen his adventure inside iSPIRT and nothing could hold him back.

Today, UPI is a success story. However, that’s not the full story.

Nikhil showed us how to stay cool under fire, to foster affinity, and skillfully navigate diverse opinions amongst many stakeholders. His all-hands-on-deck work ethic came with an ability to take decisive action when the situation demanded it. He showed that a young volunteer can be a visionary with big plans and the capacity to bring them to life. He has set an example for all of us on how to pay-forward and serve a cause bigger than all of us. All this makes him an iSPIRT Volunteer Hero.

From tomorrow, Nikhil is shifting gears. He is stepping away from being a volunteer-in-residence. He is taking a few months break. After that, he plans to create a startup. This is great news for iSPIRT. While our India Stack and other technology public platforms create possibilities, it is the products and services that create value. We need all elements of a healthy society – sarkar, samaj, bazaar – to come together to solve population scale problems sustainably. So, we wish him all the very best in this new pursuit of excellence.

All shifts require an adjustment. While Nikhil will remain a part-time iSPIRT volunteer working on WANI, he will no longer be the iSPIRT voice on payments for media, policymakers, startups and financial institutions.

Nikhil’s lasting legacy is that he opened up iSPIRT volunteering for talented youngsters under-30s. Today we have more than a dozen young power volunteers. He has helped all of us see the particular gifts that these young volunteers bring to the cause. His spirit will live on!

By Sharad Sharma, Pramod Varma and Sanjay Khan Nagra for Volunteer Fellow Council

Bharat Inclusion Initiative seeks to equip entrepreneurs with the right knowledge, skills and tools they need to solve some of the toughest problems of India in a scalable manner using technology. While Bharat Inclusion Research Fellows are working on some of the most interesting studies, another important source of knowledge is thought leaders and domain experts who have been there and done that. In this three-part video series, we have Dr Pramod Varma, the Chief Architect of Aadhaar, providing his perspective on how entrepreneurs can go about building solutions for Bharat.

Part 1: The Key Construct

What are Bharat’s unique attributes? Its needs and aspirations? With data becoming one of Bharat’s key assets, how can entrepreneurs leverage it to provide solutions that matter? Watch the video to know some answers to these questions and much more.

Part 2: The Journey So Far

How to leverage the opportunity made available through Data empowerment? Know how Aadhaar, India’s biometric ID, has fundamentally changed the economics of reaching the poor. Understand how the Aadhaar platform has aided in building further platforms of IndiaStack such as eSign and Digilocker which have further reduced cost and increased trust at scale. The video rounds off with another uniquely Indian platform — Unified Payment Interface (UPI).

Part 3: Exciting Times Ahead

Reimagine solutions. With the newer domain, specific stacks being built, learn how even seemingly unrelated domains can use these platforms to offer innovative solutions. With GST and BBPS already in place, and more being built around transport (ETC), National Health Stack, Diksha and Drone Stack it has been never this good for entrepreneurs crafting solutions for Bharat. Watch the video to understand how.

____________________

What is Bharat Inclusion Initiative?

Bharat Inclusion Initiative (BII) is an incubator platform atCIIE that provides entrepreneurs with the domain knowledge, training, financial support, mentorship, and market access they need to bring inclusive, for-profit-business to life. BII’s core design is to promote technology-driven entrepreneurship towards the delivery of affordable services to the Bharat Segment- the poorest 200 million households in India who survive on less than $5 per person a day through programs, fellowships, and funding where possible.

The program focuses on solutions leveraging technology, especially the India Stack. It integrates financial inclusion research with entrepreneurship and training to transform these solutions into scalable, viable and high impact businesses. Keen on partnering with entrepreneurs who are driven by building next-generation digital services for India. Reach out to us at [email protected] or ask your questions in the comments section below.

Please note: The above information was first published by Bharat Inclusion Fellows here: https://medium.com/bharatinclusion/building-for-bharat-df8b12867271

Access to formal credit continues to be one of the largest challenges faced by MSMEs in India due to lack of verifiable data about their business.Digital payments data combined with GST data has the potential to unlock millions of SMEs & bring them into the formal system. India is going through a Cambrian explosion of data usage. It is estimated that the monthly data consumption on every smartphone in India is estimated to grow nearly five times from 3.9 GB in 2017 to 18 GB by 2023 as per a report by Swedish telecom gear maker Ericsson.

As businesses and their processes get digitized, it provides us a unique opportunity to re-imagine credit products for MSMEs like never before.

In order to move from traditional Asset-based lending to Data based lending it is important to make the following design considerations:

Underwriting based on Data – Assess creditworthiness in real time based on the consented data provided by the user

Low-Value – Bringing down the cost of processing a loan using digital platforms like eKYC, eSign & UPI enables one to process sachet sized loans

Smaller Tenures – Offer small tenures to reduce risk and thereby build better credit history of a customer

Customised Loan Offers – In the old world, loan products were designed to be one size fits all; With data & better underwriting, create a “loan offer on the fly” for a borrower based on his need

Getting started with GST Data Based Lending – Basics

Over 8M+ businesses in India will file GST returns

Every invoice in the GSTN system is verified by the counterparty

GST returns are digitally signed and this data can be accessed through consent of a small business

To access this data, you need the understand the three types of GST APIs:

Authentication – Allows a taxpayer to login into his GST account from any application

Returns – Allows a taxpayer to file his returns from any application

Ledger – Allows a taxpayer to view & share his tax data with any application

You can access the GSTN Sandbox & APIs here: bit.ly/GSTAPIs

If you want more insights, do join the GSTN Discussion Forum here: bit.ly/GSTgroup

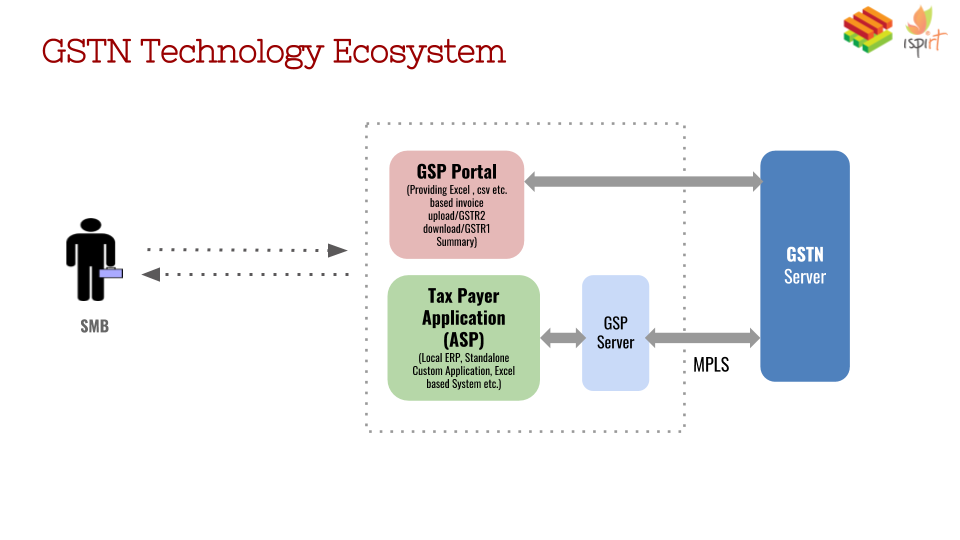

The GSTN Tech Ecosystem

Goods and Service Tax Network is a section 8 company set up to provide common and shared IT infrastructure and services to the Central and State Governments, Tax Payers and other stakeholders for the implementation of the Goods & Services Tax (GST).

In this context, it is important to understand the below two roles of GSTN:

Direct portal for taxpayers – https://services.gst.gov.in/services/login

GST Suvidha Provider (GSP) – Companies which provide GST API Gateway as a service to application service providers; They are appointed by the GSTN and list of the GSPs can be accessed here:http://www.gstn.org/gsp-list/

ASPs – Companies which provide the user interface for business to file or fetch their returns from the GSTN

Naturally, ASPs are a great fit as distribution partners for lending as they own and control the end user experience of small businesses. Some of the examples are:

Accounting Software Providers

They help small business manage their accounting, inventory & even payroll;

They have rich data sets about the small business including their GST returns Eg: Tally (Desktop), Zoho/Cleartax/Profitbooks (Cloud-based)

Tax Filing Software Providers

These companies help business who use excel/manual billing/custom software to prepare their GST return & file it every month;

One of the key stakeholders here is the accountant who essentially is the business advisor for an SMB and tapping into them as an influencer channel is a great opportunity Eg: Cleartax, SahiGST etc.

Supply Chain Automation Companies:

Today many FMCGs and Large manufacturing companies are using software to track their sales/inventory in their supply chain; For e.g: Asian Paints, Tata Steel, ITC etc.

As these companies enable a large of wholesalers, retailers to use their software problem, there is a great opportunity to extend credit to their entire ecosystem

Eg: Moglix, Channel Konnekt, Bizom etc.

Example of a Lender – ASP Partnership

Consider a services-based company which provides advertising services to multiple companies

Let’s assume they use an accounting software like for example Cleartax or Zoho

In the software, the SMB sees a one-click credit button (This is enabled through an integration with the ASP & lender)

In a few clicks, the SMB is able to share multiple types of data like – GST, Payroll, Balance Sheet, Bank Statement etc. with the lender

With consent, the lender uses this data for underwriting, build a credit score and makes a credit offer to the SMB

The SMB provides his bank account details for real-time loan disbursement and based on the type of the business you can complete KYC

Take mandate either digitally or physically based on the customer for repayments

There are various other data sources one could use to improve the underwriting like – Smartphone, Payments Data from the Bank, Bill Payments, Electronic Toll Collection & various others. Algorithms can use these data sources along with other other public data sets like – Seasonal demand for a product, Import/Export, GDP, Consumption Patterns to do contextual lending.

We recommend you go through the presentation above to understand these basics & do watch the pre-recorded webinar session below on How to Leverage GST data for Flow-based lending for more details.

At iSPIRT, we are working with multiple stakeholders to create a winning implementation of Flow-Based Lending. Do watch out for future announcements from us for entrepreneurs working in this space or write to us [email protected] to know more.

About the Author

Nikhil Kumar is a full-time fellow with iSPIRT Foundation, a non for profit think-thank and has been focussed on building the developer ecosystem for the India Stack.