MSME Lenders need to start looking beyond AUM to truly value short-term loan pools. OCEN helps minimize loan processing costs and provide easy access to new borrower segments at scale. Specialized roles, including collections partners, help reduce the burden on lenders. Short-term lending products for marketplaces where Loan Agents also control the income-source for the borrower can use escrow-based-repayments to mitigate the collections risk. New datasets enable lenders to make easier underwriting decisions for cash-flow based lending.

Both TReDS and OCEN play critical roles in improving MSME access to credit, albeit for different segments of the market. Unlike TReDS, OCEN eliminates the buyer acceptance bottleneck. Instead, it leverages alternative underwriting models, specialized loan products, and digital collections to offer small‑ticket, short‑tenure working capital loans to MSMEs.

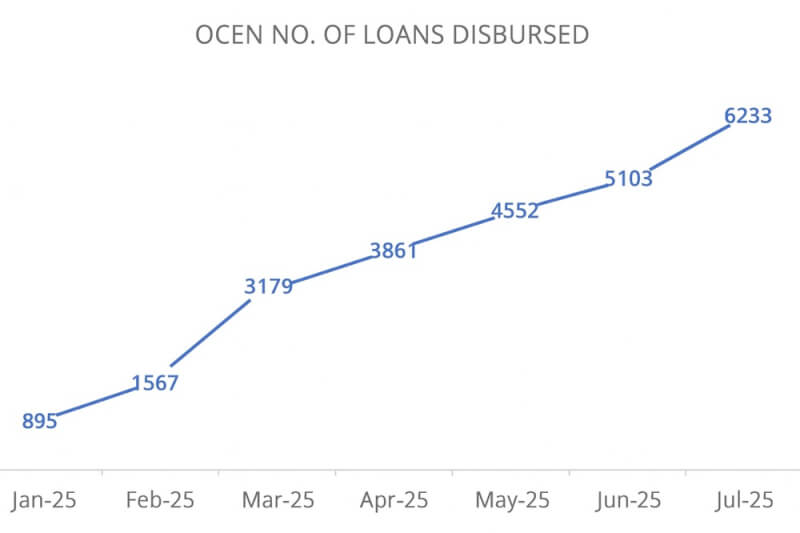

While TReDS will likely continue growing in disbursal volumes and strengthen formal receivables financing, OCEN’s focus on smaller, flexible loans positions it to grow much faster in terms of number of loans disbursed. Though TReDS and OCEN are targeting the same goal, both have its own unique features to succeed and co-exist to meet the common goal faster. OCEN becomes the next choice to solve for smaller businesses with small ticket loan requirements who are beyond the formal credit net and do not fit in the TReDS window. OCEN is growing fast with 30% MoM increase in number of loans due to the framework capabilities.

| Metric | Jan-25 | Feb-25 | Mar-25 | Apr-25 | May-25 | Jun-25 | Jul-25 |

|---|---|---|---|---|---|---|---|

| No. of Loans Disbursed | 895 | 1567 | 3179 | 3861 | 4552 | 5103 | 6233 |

| Disbursement Amount in Lacs | 2517 | 3367 | 13911 | 7613 | 9082 | 10621 | 13886 |

For more information, please visit: http://ocen.dev

Please note: The blog post is authored by our volunteer, Rahul Bhaik