If you have not come across ONDC – Open Network for Digital Commerce, its time you know about it and this post is to help better understand what problem it addresses, how it operates, and the value that it brings to consumers, businesses, retailers, existing e-commerce platforms and the state.

Problem statement

There are a number of pain points around current digital commerce:

- Its dominated by a few players e.g. Amazon, Flipkart, Zomato, MakeMyTrip, etc.

- Consumers have to go to multiple platforms to search and explore the products/services they would like

- Consumers are restricted to only a subset of products/services available on the platforms

- Consumers need to go to multiple places for different products/services

- Penetration is not widespread across the country and small towns

- Small businesses are not able to participate and sell in the digital commerce space

Solution

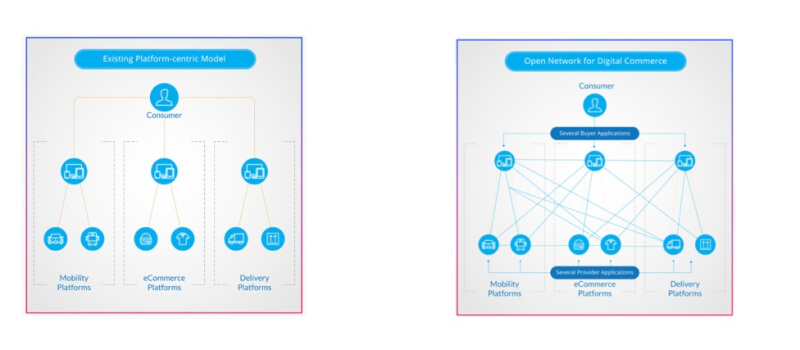

Open Network for Digital Commerce is a network of e-commerce. It is a network-centric model where, so long as platforms/applications are connected to this open network, buyers and sellers can transact irrespective of the platforms/applications they use. It’s like “UPI of e-commerce”

Source: ONDC.org

ONDC works on 3 important use cases to solve the problems, which explained very well by ThinkSchool

Discoverability – allows you to discover products across different platforms using a common catalog

Interoperability – where you can combine multiple platforms to accomplish different services e.g. product with delivery, services with payments etc.

Price comparison – allows you to compare prices across these platforms e.g. ticket prices across different ticketing platforms.

How does it work?

Through an open protocol network, various selling /buying apps such as flipkart, dunzo, airtel, paytm will connect to the network and the consumer will be able to access the product/services through any of the apps.

You can either connect to the buyer network or seller network. One of the important aspects of ONDC is to standardize the product/services catalog so that consumers get a common experience. All the technical specifications are available here

Role of ONDC

ONDC will play three roles as laid out by their CEO

Development – Build and sustain the network with cutting-edge tech and facilitation widespread participation of ecosystem players

Network Management – Establish a code of conduct for the network, with policies and rules for the network

Service Delivery – Foundation services for operations of the network e.g. registry, certification, grievances redressal

Value for stakeholders

Consumers – amazing way to explore and get the best product/services across platforms, sellers

eCommerce Companies – Gets a wide reach with Govt. backing to get to a large user footprint, make them more competitive

Small Businesses – Gets them to sell products and services across the country, without having to be associated with a single platform

Government – Accomplish the mission of connecting India digitally and enhancing the economy significantly

Challenges

This is a massive and ambitious project, balancing of different stakeholders is going to be huge, as well as connecting all of them. Also ensuring the quality of service is going to be a big factor, as the trust factor of the platform plays a big role in deciding where to buy.

But given the Government backing and really smart think tank behind this, these challenges may likely be overcome.

Key Takeaway

ONDC looks to be a huge potential and another game changer for an Atmanirbhar Bharat.

More Resources

With the growing penetration of technology, Internet, and digital medium, there is an increasing need for protecting critical infrastructure of the country. If compromised, these infrastructure can bring down the entire nation to stand still. With the nation going Digital India and the Prime Minister himself talking about security frequently, and challenging Indian citizens to create products that will server the nation and the world, we at iSPIRT are taking this

With the growing penetration of technology, Internet, and digital medium, there is an increasing need for protecting critical infrastructure of the country. If compromised, these infrastructure can bring down the entire nation to stand still. With the nation going Digital India and the Prime Minister himself talking about security frequently, and challenging Indian citizens to create products that will server the nation and the world, we at iSPIRT are taking this