The Micro, Small, and Medium Enterprises (MSME) sector is the engine of the Indian economy, yet for years, it has been choked by a massive credit gap. Traditional, collateral-heavy lending processes simply could not keep pace with the dynamic, short-tenure funding needs of small businesses.

Open Credit Enablement Network (OCEN): Built on the principles of India Stack, this digital protocol is not just facilitating loans; it is fundamentally rewiring the architecture of MSME credit, making it instant, affordable, and accessible. The monthly growth witnessed in the calendar year 2025 proves the model is not just viable, but highly scalable, marking a new era of financial inclusion.

The Power of Cash Flow-Based Lending

OCEN’s disruptive approach lies in shifting the lending paradigm from asset-based to cash flow-based underwriting. For millions of creditworthy small businesses, their true financial health is reflected in their daily or monthly transactions, not in static, year-old balance sheets. By leveraging India’s digital public infrastructure, OCEN allows lenders to assess risk based on real-time, consented data helping them to take faster decisions and making small-ticket, short-tenure credit economically feasible for lenders.

This framework is specifically designed to solve for the underserved, those who need smaller loans for shorter periods but have previously been locked out of formal credit channels.

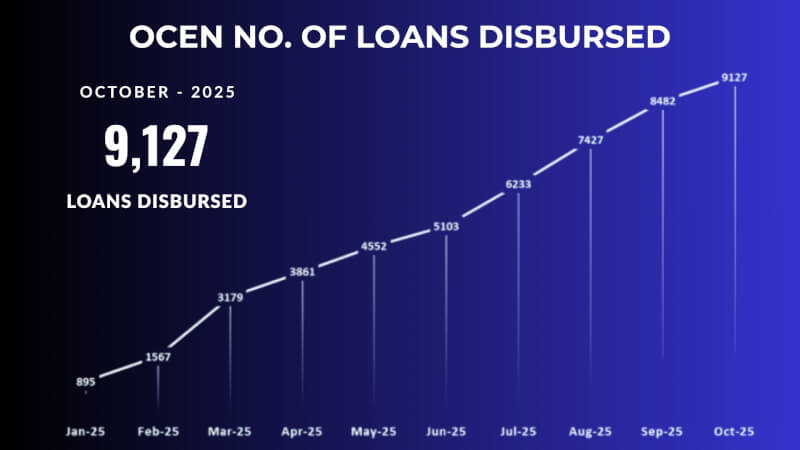

Demonstrating Growth and Inclusion

OCEN demonstrated its ability to deliver on its promise of democratizing credit. The network has disbursed 50,426 loans and amounting to ₹1142 Crore in total disbursement within the calendar year till October 2025.

October 2025: OCEN saw the highest ever monthly disbursement of 191 Crore across 9127 loans Catering directly to the daily needs of MSMEs. The growth highlights how the protocol’s architecture is perfectly suited for mass-market financial inclusion. The emphasis is clearly on the number of lives touched and the frequency of credit access, rather than just the size of the total loan book.

Validating the Model: Exceptional Portfolio Health

The true testament to OCEN’s cash flow-based underwriting is not just the speed and volume of disbursement, but the quality of the loan book. Crucially, the loans disbursed through the OCEN protocol have demonstrated very minimal Non-Performing Assets (NPAs). This performance is exceptionally better than the NPA figures typically observed in traditional MSME lending portfolios across the industry. This is not just a marginal improvement; it is a fundamental validation of the protocol’s ability to accurately identify and price risk among digitally visible, cash flow-rich MSMEs. By moving beyond outdated collateral requirements and relying on real-time transactional data,

OCEN is proving that digital, embedded credit is inherently safer and more sustainable than conventional lending practices, offering a high-growth, low-risk opportunity for participating lenders.

For more information, please visit: http://ocen.dev

Please note: The blog post is authored by our volunteer, Rahul Bhaik