iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

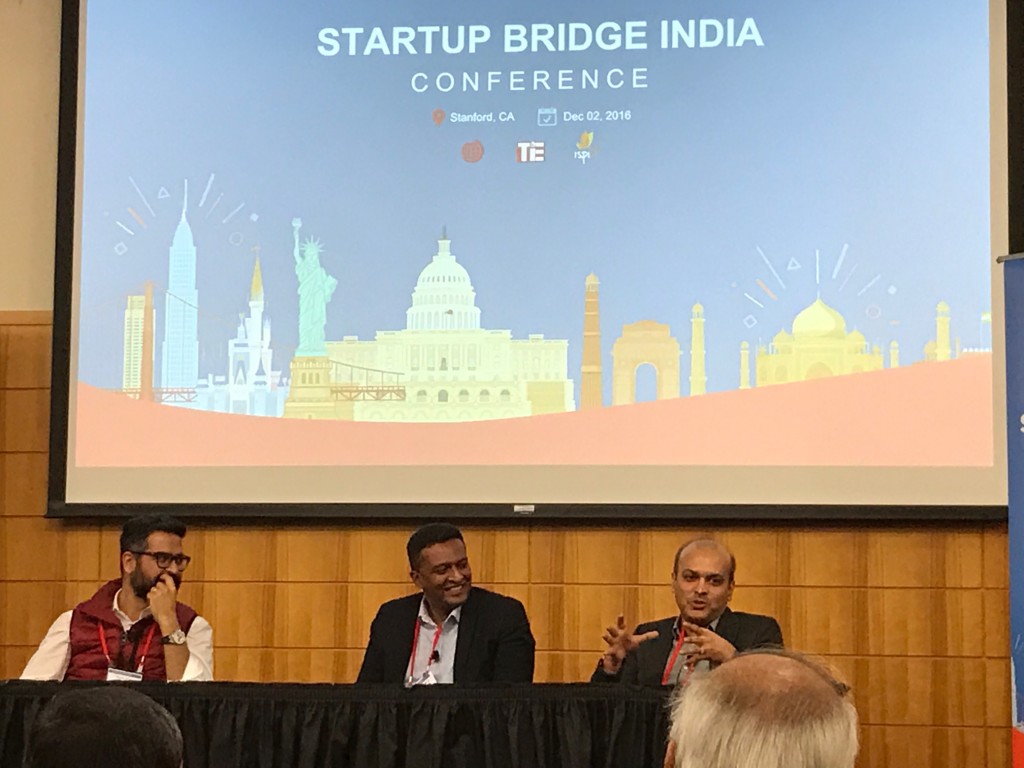

India has fast emerged as the world’s second largest Internet market. Since 2012, nearly $15 billion has been invested in tech startups with over 300 M&A deals. However, a large percentage of deals (80%, 2014-Q3’16) were sub-$5M deals driven by acquihires and restructuring. Looking west to Israel and the US, it is clear that for a healthy technology product ecosystem, further acceleration in later stage M&A and buyouts is undeniably required. And with this very thesis in mind, iSPIRT, along with TiE Silicon Valley and Stanford University, organized the inaugural Startup Bridge India event on Dec 2,2016, with the goal of fostering cross-border partnerships with Silicon Valley corporates to drive investments and/or acquisitions of domestic startups.

We are building auto-pilot software for managing cloud operations. The rocket ship is Silicon Valley and Startup Bridge was our gateway to it. Vijay Rayapati, CEO, Minjar

The event was an important chapter in the history of India’s tech landscape for multiple reasons.

For one, it was the first step in breaking down borders between Silicon Valley and India. It is no easy feat to gather the top BD and Corp Dev executives from the largest tech Silicon Valley giants all together under a single roof. But with representatives from 65 corporates meeting 28 startups driving 120 connections for partnerships and investment/acquisition discussions, the very fact that the doors were opened, some even knocked down, was a giant leap for the ecosystem.

We were able to have of bunch of meaningful 1-1 conversation with potential strategic partners. Sunil Patro, CEO SignEasy

The second win – a powerful collaborative relationship between TiE Silicon Valley and iSPIRT – was one of breaking down barriers. The coming together of two impactful organizations driven by a similar vision so seamlessly to build a momentous event in ~10 weeks of planning was nothing short of inspirational, an affirmation of the power of the volunteer-driven model that iSPIRT has established itself upon.

The third win, however, was arguably the most powerful – that of breaking down the BS among even the most experienced entrepreneurs in India. iSPIRT has long held a position of being an unbiased stakeholder, with the primary goal of driving positive change in the tech startup ecosystem. Mature entrepreneurs in India, historically big fish in a small pond, have long believed their systems, their pitches, their stories, had been tried, tested and proven. However, playing on the global stage is a whole new ball game and iSPIRT stepped in to break down the BS for entrepreneurs.

I thought I had my deck all figured out. I thought I knew my pitch and had the details at my fingertips. But then I started getting really valuable, thought-out feedback from iSPIRT and I realized I had so much to improve on. I had to focus on pitching to partners, not customers. My narrative was made crisper and my focus was changed from ‘what we’ve done in the past’ to what is coming up next. All of that feedback resulted in a much stronger pitch and more engaged conversations with partners after. Pallav Nadhani, CEO FusionCharts

StartUp Bridge India, with an NPS of 68%, was another valiant step towards putting the Indian startup ecosystem on the global map alongside mammoths like the US and Israel. Team Indus, an Indian startup working to land a rover on Mars, is India’s literal moonshot. Startup India, working to increase cross-border investments and M&A, was India’s figurative moonshot. And after Startup Bridge, it was clear, that this moonshop has a robust arm and is gaining an increasingly powerful momentum.

The story of India’s tech landscape is being written as we speak, and the future is nothing short of exciting…

StarupBridge India is an important step forward for India’s journey as a Product Nation. For the first time, it brought together India’s top global startups at this scale to meet and connect with Silicon Valley’s company to explore potential strategic partnership. This conference will be referred as seminal for years to come as it created a key turning point of software products cross border partnerships. M Thiyagarajan (Rajan), CoFounder & Fellow iSPIRT

Last month, for the first time, I witnessed something really special. Even for someone like me, whose very job and calling is to evangelise this nascent software ecosystem of ours, this was something extraordinary.

I’ve been doing this a while, and what happened last month was one of the best feelings I’ve had in this journey.

This is what they got together for: To help 52 other, smaller B2B startups in achieving scale, like they have.

It’s no exaggeration to say that the founders of these companies are some of the most important product leaders we have.

In the first session itself, Shekar Kirani pointed out that a platform like this will not be easily available, and the assembled startups needed to leverage the best from the network and from the folks who had arrived with the the express intention of helping them. And the product leaders who also made an important point – that they did not want the new age startups to go through the same grind, or make the same mistakes they had made in their years of scaling.

I was amazed. It is almost never that you see such accomplished professionals come together towards helping and nurturing young startups from their own learnings.

And what was this? What was happening?

This was the 2nd edition of #PNgrowth.

The first one had been in Jan 2016 at the Infosys Campus in Mysore where we had assembled around 186 founders to help companies think about Category Leadership. It went really, really well, but the feedback was that that perhaps keeping it focussed for fewer founders would help the cause better.

Many heated discussions were conducted over breakfast, lunch, dinner, and beer (especially beer) on the program for the 2nd edition and on how we can add value to the content.

These conversations were typically 4-6 hours long, which meant that the entire program/content took us over 200 hours with 12 founders brainstorming for the past 3-4 months.

It really did take us that long.

And those deep discussions based on the 1st edition’s feedback was what the program for November was based on.

And now that #PNgrowth 2016 is over, I decided to take a look back and share some of the learnings in organising this, and on how we pulled this together.

This year, the program was designed to help companies chase ‘Good Scale’, that is, to achieve high growth without compromising on quality. There were 52 founders with us, from all over India, and a few from outside as well.

Before we get into the details, a larger question must be addressed again, largely because it keeps getting brought up. This time, I’m trying to use a different approach to explain this. Bear with me.

WHY IS iSPIRT DOING THIS ‘MOVIE’ CALLED PNGROWTH?

iSPIRT’s mission is to make India a ProductNation. We have many initiatives like Playbook Roundtables, PNcamp, etc which are focussed around building products and helping companies achieve good scale. Although there are many accelerators in our country, very few offer value to the founders/companies. Keeping this in mind, iSPIRT wanted to do something unique and create a platform which would help companies think about growth in an effective manner. More importantly, we want to make ongoing mentorship accessible to the founders.

The goal was to create 8-10 companies every year which would eventually go on to become $10mn revenue companies in the next 3 years.

WHO ARE THE DIRECTORS OF THE MOVIE?

These are the co-chairs.

The first edition of PNgrowth had just finished and I was looking for someone to be the architect for the second edition. I met Shankar Maruwada for lunch at Muffets & Tuffets and was having a completely different conversation. But, as we touched upon the PNgrowth topic, Shankar had lots of suggestions on how we could do this better. I immediately requested him to help in designing the program and helping me organise it better.. He accepted graciously, and was keen to help.

My next request was to get Pallav Nadhani involved again. There is a reason for this. Pallav, in many ways, was the person who forced us to think around Category Leadership. The first meeting took place at Pallav’s place which went on till 2:30 am.

By then, I had had several interactions with Aneesh Reddy, and the early playbook roundtables on Product Management had been done by him. I reached out to him and he was very keen to be part of the program and help us.

With Shankar, Pallav and Aneesh on-board, the pillars of the event were erected.

WHERE DID I FIND THE STAR CAST FOR THE MOVIE?

These, of course, were the facilitators.

Around 4-6 months in advance, we started working on the content for the event. Various topics were discussed. One thing was clear to me: Every founder had immense passion and commitment to add value to a certain topic. The format we had in mind was to make very interactive session. All of us had had enough of the ‘sage on stage’ approach. The founders were to lead sessions and work along with the participating entrepreneurs to help them extract maximum benefit.

Many discussions later, Pallav & Shankar actually started with using the frameworks & mindflips and were later joined by Girish & Aneesh. Manav & Shekhar also used the same in their session.

It was great to see that all the facilitators did an outstanding job of delivery of the frameworks and ensured that they shared real life stories and lots of data and numbers from their companies. What was more important was that they made sure they spent time with all the attendees and ensured they received personalised attention. They were able to build a personal connect and trust within the startup community by sharing internal information even though they didn’t have to, thereby making the discussion even more credible.

WHO CAME TO WATCH THE MOVIE?

Oh, that. We had huge demand for tickets from the audience, the founders of India’s growing startup community.

HOW DID WE THEN SELECT WHO ACTUALLY GOT TO SEE THE MOVIE?

This time, right from Day 1, we only wanted to get select founders to be part of PNgrowth.

To begin this selection process, we laid out which stage of startups would benefit from PNgrowth. We then went on and created a list of founders and reached out to them. Apart from this, we reached out to folks from within the eco-system and got them to recommend companies to us.

Each company was recommended by atleast 2-3 founders from the PNgrowth curation team. We did zero marketing for PNgrowth except for a video, which we used to communicate to potential participants. We received overwhelming response for the event thus putting me in a fix at several situations where I had to inform founders that they have been rejected for a program/event. It was difficult, but in the interest of the event, it had to be done.

We finally had 54 founders who confirmed their participation, out of which 52 showed up for the bootcamp. These companies were divided into groups of 6 based on the type of customer/geography they were catering to.

WHERE DID WE HIRE THE SUPPORTING ACTORS?

These were the mentors, and we were able to get around 14 founders as mentors and were simply amazed by their commitment for the two and a half days of the event. Mentors were involved in all facets of the event – from intense board room discussions to the dance floor. Let me go little more deeper on the role that they played. In every session, the founders got access to few frameworks, mindflips which they had to fill and discuss with their peers + mentors. Lot of learnings were shared by mentors and it became very valuable to the founders. Very few of them tweeted from the program as everyone was busy interacting, engaging, absorbing content, but here is one of the tweets which acknowledges the mentors.

WHAT ABOUT THE CREW?

Getting to them, the volunteers.

In my work, I get to interact with many volunteers in many initiatives, but this time the commitment and the passion with which the volunteers worked was unimaginable. Folks would go to sleep at 5am and be ready next day at 8am. They would ensure that mentors/founders have had breakfast, etc and would go an extra mile to take care that founders are focussed on their work and don’t get distracted.

Volunteers also interacted with the founders to understand if the pace/level of the sessions suited them. Lot of planning was done in advance that each and every person who is part of PNgrowth goes back with a WOW experience. I still wonder where they get so much of inspiration from.

I don’t know if i would ever be able to do something like that. Hats off to all the volunteers who put together an awesome experience for the PNgrowth family.

SO, WHAT WAS THE MOVIE ALL ABOUT, THEN?

Day 1

The Founders started with a cricket match between the cohorts itself.

Sharad Sharma, our guiding light, kick started the event with his words of wisdom for all the founders.

And then it began with Pallav’s session on Who are you? As founders, entrepreneurs have to pitch or sell their ideas constantly, so as to inspire the listener to believe in their dream to either fund the idea, join the team, tie up with the startup, or write about the startup. Is there a method to this? Can this be an acquired skill?

In this session, founders learnt and practiced a simple framework that enables them to improve their ability to pitch their ideas in the shortest time, to the desired target audience – VCs, journalists, co-founders, customers, business partners, and employees.

The next session was focussed on how to maximise the value of your product. If you as a founder were to increase the perceived value of your offering (Increase average MRR by 1.5X and/or reduce churn to 0.5X),how would your economics change? How would it change your CAC, margins? What would you as a founder then do differently with your product strategy, go to market strategy (positioning, marketing, channel, pricing), team/organization structure, to increase pricing by 1.5X, in the scenarios below as relevant to you. This was followed by an interactive session with the mentors.

This was end of Day 1 and then we had networking dinner, drinks, some dance and lots of conversations led by Vinod & Ashish.

Day 2

The second day was a more power packed with two sessions. To their credit, the founders were highly engrossed in their sessions, sans their mobile phones and laptops which helped in making these sessions successful.

During the first half, Girish and Aneesh engaged in an extremely fruitful session on product-market how to scale 10X with emphasis on how to establish your sales funnel and building a repeatable sales cycle. This session covered on selling processes from SMBs (by Girish) and enterprises (by Aneesh). They also shed some light on how pricing, positioning and selling varies from one geography to another.

Apart from this, Suresh also gave his insights on selling global products out of India.

The complete session went on till almost tea break after which the candidates came back in for the third and final session by Shekhar and Manav.

This session was meant to give a befitting end to the two rigorous days of activity.

While Manav spoke about how to choose your niche category and expand to other similar industries and geographies, Shekhar’s session was centred around what a VC looks for a in a startup. In the session,

Shekhar did a Q&A round with Nags and Girish on what it takes to build a successful organisation.

He also delved a bit deeper on aspects like how to choose the right market and how to intelligently figure a way out of a market and move into one that is expanding by extracting maximum business value.

Here Raghu also added his thoughts on what it takes to raise venture capital and how one should structure an organisation for a CEO to utilise his time in the most efficient manner.

Though the mentors tried to cover as much ground as possible over the two days, they took questions from audiences on anything they still might have a doubt about.

After this was a complete group photograph since some of the mentors had to leave that night. The energy of the picture speaks for itself. Before calling it a day, the founders were given tasks/homework for them to present on the final day.

Day 3

The third day, we had some inspirational stories from Sanjay Anandaram(Seedfund), Mohit Dubey (CarWale), Phanindra Sama(RedBus), Raghunandan G(TaxiForSure), Sanjay Deshpande(FortyTwo Labs). We had actually planned for only Sanjay to talk about “entrepreneurial mindset” and then we thought about inviting all of the above folks to share their energy.

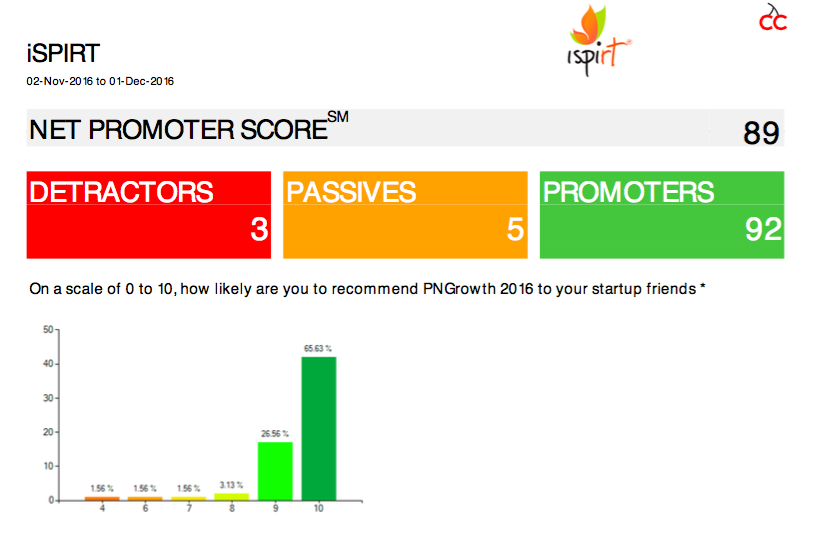

Something which we had planned for 20-30 minutes went on for around 90 mins and it was an absolute pleasure to hear some of the learnings/failures from all these founders. Below is the NPS score of 89 for PNgrowth 🙂

After this, all founders were made to do this exercise on “Getting to 3X Growth in 12 Months”. All mentors with their cohorts spent time with the founders and helped them on what they should be thinking about this. Six Founders got an opportunity to share with the whole group.

Finally Shankar invited all volunteers to share few words on why they volunteered for PNgrowth. With it, a spectacular three days came to end, with some photographs and a lot of hugs, cheers, and greetings.

For me, it was a great feeling to see all of this happen, and at this scale. This probably capped off the year of 2016 for me and iSPIRT as a year in which we were actually able to make the ecosystem function as a cohesive, united entity. Lots of work is ahead of us, but as I write this, I acknowledge a task well begun.

Many thanks to Sairam for editing & Shruti for filling the blanks.

External commercial borrowings(ECB) imply borrowing (debt) from a foreign (non-resident) lender. ECB is an attractive financing route as it generally offers access to finance with low rate of interest available from overseas low interest markets.

ECBs have been in use by many corporations, PSUS and especially by MNCs setting up operations in India. Who can raise an ECB, from where and under what conditions, rate, maturity period etc. are all governed by Reserve Bank of India (RBI) in India. Startups till now did not have access to the ECB route of funding.

RBI announcement on ECB for Startups

Announcement was made by the Reserve Bank in the Fourth Bi-monthly Monetary Policy Statement for the year 2016-17 released on October 04, 2016, for permitting Startup enterprises to access loans under ECB framework.

Sanjay Khan Nagra, iSPIRT volunteer talks about this announcement in the video embedded. Below.

As such RBI circular is self-explanatory attached here. However, for ready reference, some salient features of the RBI announcement are covered in the text given below.

What are the key announcements?

What is a Startups as per circular?

The above circular covers Startups as defined by the Official Gazette of Government of India dated February 18, 2016 (i.e. Startup Policy of DIPP) given here.

How much can a startup borrow and in what currency?

A startup can borrow up to US$ 3 million or equivalent per financial year either in Indian rupee or any convertible foreign currency or a combination of both. In case of borrowing in INR, the non-resident lender, should mobilise INR through swaps/outright sale undertaken through an AD Category-I bank in India.

What is minimum maturity period?

Minimum average maturity period will be 3 years.

For what end-use can startups use ECB?

Usually there are end-use direction for an ECB. However, for startups under the above said circular of RBI, ECB can be used for any expenditure in connection with the business of the Startup.

What is all-in-cost of ECB?

There are no limits. The RBI circular says, this shall be mutually agreed between the borrower and the lender

In what forms can one receive the lending?

It can be in the form of loans or non-convertible, optionally convertible or partially convertible preference shares and the minimum average maturity period will be 3 years.

Can this be converted in to equity?

Yes, conversion into equity is freely permitted, subject to Regulations applicable for foreign investment in Startups.

Who can lend?

Previously, ECB regime inter alia set out various conditions for Indian companies raising loan from external borrowings including conditions relating to (i) eligible borrowers (ii) eligible lenders (iii) permitted end uses etc.

After this circular, the lender / investor shall be a resident of a country who is either a member of Financial Action Task Force (FATF) or a member of a FATF-Style Regional Bodies; and shall not be from a country identified in the public statement of the FATF. (Please see RBI Circular for detail)

However, overseas branches and subsidiaries of Indian banks and overseas wholly-owned subsidiary or joint venture of an Indian company will not be considered as recognized lenders.

What are security norms?

Foreign lenders or Investors are allowed to request security for any collateral in the nature of movable, immovable, intangible assets (including patents, IP rights etc.) but shall comply with foreign direct investment norms applicable for foreign lenders holding such securities.

Issuance of corporate or personal guarantee is allowed. Guarantee issued by non-resident(s) is allowed only if such parties qualify as lender under paragraph 2(c) above. Exclusion: Issuance of guarantee, standby letter of credit, letter of undertaking or letter of comfort by Indian banks, all India Financial Institutions and NBFCs is not permitted.

For more details you are requested to refer the RBI circular here.

A phenomenon that has been pretty popular recently in the news goes by the name of UPI(Unified Payments Interface). However, most people have not been able to experience the revolution and the magic moment that comes along when paying via it.Part of that stems from the myths that keep floating around, regarding how it might not be that secure and worthwhile. Well, allow me to put all of these doubts at ease through this post.

Let us take all the salient features of UPI one by one –

Bye-bye long account numbers and IFSC codes

Convenience factor

Now, there is no need to ask anyone for their account numbers or IFSC codes when sending or receiving money. Apart from the fact that remembering long account numbers and IFSC codes is cumbersome, entering those on a small screen / app is painful (especially considering that the user experience of banking websites and apps is mostly terrible).

Of course, the question is now what replaces these 2 if they are not in the picture any more. Say hello to virtual address (which looks like sunnyrohit@ybl where the first part is a unique ID set by you and the second part is determined by the bank/app which processes your payments). This virtual address is automatically mapped to your bank account by NPCI when you register for the first time.

Security factor

The first thing to observe is that since you no longer need to share your account details (Number and IFSC code) with anyone, hence they are completely hidden from everyone else.

Secondly, what this process does is that it takes your user level identification to a more abstract level where the virtual address (or in our case – mobile number) becomes the key information to know or share with anyone. And sharing it is completely harmless as a common person cannot extract any info from that.

Send and receive money instantly, 24*7 and even on a holiday

Convenience factor

Needless to say that this is a game changer, especially in this new economy where demonetization has brought cash to a near standstill and banks/ATMs are clogged up. Not to mention that when sending / receiving money, we don’t even need to think what day and time it may be.

Security factor

Actually, UPI is built on the existing layer of IMPS (Immediate payment service) which has been running smoothly since 2010. Hence, the key thing to note here is that the basic security concepts have stood the test of time for 6 years now. Not to mention that they have improved along the way and many more locks as well as checks have been added on top.

Linked exclusively to your mobile device

Convenience factor

This is a no brainer as everybody has their personal mobile with them 24×7. And it is also the first device that we think of nowadays when receiving / sharing anything on a speedy basis.

Also not to worry, you can link multiple bank accounts as well with the same virtual address. As well as un-link / delete account at any point of time.

Security factor

Firstly, it is important to remember that your virtual address gets mapped to your device exclusively. Now couple this with the fact that for making any payment (peer to peer and peer to merchant), you need to enter your M-pin (a secure 6 digit pin set by you for the first time), and then you can see how it is a perfect closed loop.

Even if anybody gets hold of your device, they cannot do anything until or unless they have your M-pin. Similarly, for resetting your M-pin, you would need your debit card details (completely separate from your device information for security reasons)

No minimum amount. A single user can do 5 transactions totalling up to Rs. 1 Lac daily

Convenience factor

Taking all common scenarios, a total amount of Rs. 1 lac is good enough to cover all your daily needs be it online / offline. And again the number of transactions can easily be covered within the limit of 5 per person. Hence, yay to good lifestyle needs!

Security factor

These velocity checks also ensure that nobody can wipe out or cause any major havoc in anyone’s bank account (although as we discussed, the chances of any data compromise are next to nothing).

Also, remember that all these aspects and features are valid for non-banking UPI apps (like ours) that have partnered with a bank or individual bank’s UPI apps as well

In today’s age of lightning speed information and open access, keep no room for confusions or myths in your life. It is time to embrace the change and be a part of a much more awesome and well-built economic infrastructure via UPI.

Guest Post by Rohit Taneja, Mypoolin, @sunnyboyrohit

The commodity products (which is a copy of an innovative product)

The innovative products get sign ups and are able to scale because they have built a very useful and handy USP. They get word of mouth from early users which are enough for them to grow to a considerable size.

However, most SaaS products today fall into the commodity category with no innovative features. For such products, three factors are really important to grow.

Pricing

One you have marketed your product well, and have people landing on your website, the first important thing is to get them to Sign up. Here the most important criteria is Pricing. As you are a commodity product, the price point, lower than the market leader will help in getting paying customers. Such a pricing strategy helps you get the price conscious customers to sign up. Remember, pricing is a factor of features. Pricing would be irrelevant without features, and your software needs to provide the features that your competitor is giving at a lower price.

Let’s take the example of Freshdesk. When Freshdesk launched, pricing was their major differentiator from their competitor Zendesk.

Usability, UI, UX

Pricing can get you signups. However, your users need to start using your software to give you their credit card ultimately. If you are not a market leader and want even to become the second best, you will have to focus on the design and usability of the product.

Often the first mover tends to avoid design, as they are competing on their innovative feature and design is where the late movers can compete on. Easy to use design coupled with self-onboarding features will help in getting the customer engaged.

The trials most SaaS products have is for 15/30 days. It is practically impossible to implement the product in the complete organisation in 15 days’ time and try all features of the product. Hence, the usability & design of the product is the most important deciding factor.

As you already have ensured a convincing pricing, there is a very high probability that the user will convert to a paying customer.

Pipedrive is one company which entered the CRM space rather late and still could make it big. This is because Pipedrive focused on the usability of the product. They have taken care of very small things — every time my team cancels a meeting or an appointment, Pipedrive gives an automated pop up which will ask for the next appointment. It reduces the chances of losing a lead in the pile because of not setting up the next activity. I run SoftwareSuggest, and have many friends who run CRM software companies. All of these CRMs are free for us to use, but we still prefer to pay Pipedrive because of its usability.

Customer Service

Converting a user to paid customer is not enough in SaaS. You will need to maximize the lifetime value (LTV) of the customer so that you start making profits. Once the user has converted to a customer, you need to start focusing on ensuring impeccable service quality. Organisations generally don’t prefer to move from one SaaS product to another. It’s a pain. Once they have signed up for a product, they like to stick with it. However, not focusing on customer experience once they have made the first payment will lead to churn. They might even leave before you have recovered your cost of customer acquisition. Hence, you will need to constantly monitor their usage of the product and ensure that the time on the app is increasing. Setting up a customer success team can be a good method. Good service will help in increasing the lifetime value of the customer.

There are many dimensions to India becoming a Product Nation. A thriving local market is critical, which are shaped by changing consumer preference and policy. Also important is increased trade in areas of comparative advantage.

Digital consumer market in India that opened few years ago saw its waves and cycle of valuation however it is already witnessing its next shift from India Metro to Bharat due to technology and regulation disruption going hand in hand (aka India Stack).

An undercurrent that has been largely unnoticed is emergence of B2B companies from India. Top 30 enterprise startups in India that are tracked in the iSPIX B2B is $10.25 billion last year. Saas market for Indian startups is exploding — and is on pace to be over $10 billion annually by 2025.

Like Israel is to Cybersecurity, India is becoming Saas capital for the world.

Ease of doing business in India is improving, out of 34 items in Stay In India check list part of Startup India Policy, 29 critical ones are fixes in progress.

Cross border partnership of US-India startups always existed, it is the right time to come together as software product industry to strengthen this linkage to highlight this new dimension. Two related initiatives to towards this

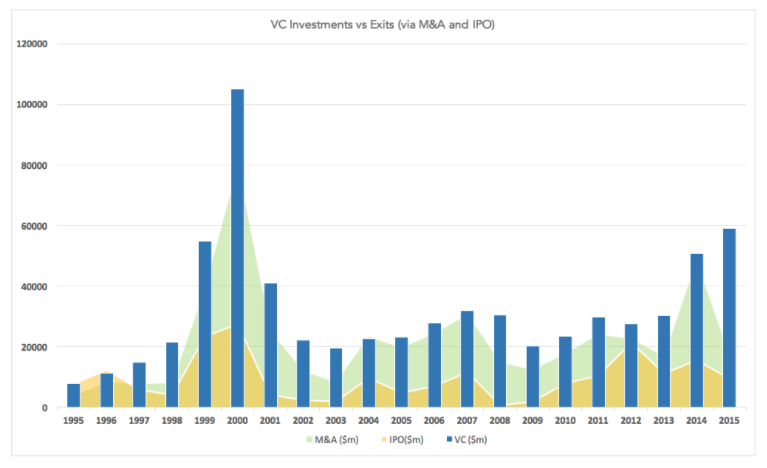

Initiative 1 – India Technology Product Exits Industry Monitor 2016, measuring liquidity especially global.

iSPIRT and Signal Hill in partnership is releasing our annual report for 2016 on state of exit deals in India. During 2014 & 2015, India witnessed a Product Technology funding boom with over $10bn getting invested in consumer tech / e-commerce companies and $1bn in enterprise tech start-ups. Whilst funding levels in 2016 have seen a steep decline (54% decline during first 3 quarters), mainly on account of a very steep drop in hedge fund activity, M&A in Product Technology with $1.34 billion in exits during the first 3 quarters (from 113 transactions), is on track to beat 2015 levels (137 transactions with $1.35bn transaction value) which was a record year for Indian Product Technology M&A. Furthermore, many global Tech majors including the likes of Apple, Google, Facebook, IBM, Naspers and Salesforce have now completed at least one Product Tech acquisition in India. However the large majority (81%) of M&A transactions are still very small (<$5m in transaction value), with the bulk (>70%) of the transaction value in the last 3 years being accounted for by 7 large (>$100m) M&A transactions. Hence there is currently a missing middle in the $5-100m deal range in Product Tech M&A in India. With an increasing number of companies that received funding during the 2014 & 2015 funding boom achieving scale during the next couple of years, we expect Product Tech M&A levels in particular across mid-size and large transactions to pick-up multi-fold from here.

Initiative 2 – StartupBridge India, strengthening foundation to increase cross border linkages.

Towards enhancing cross border linkages iSPIRT is organizing a conference called StartupBridge India in partnership with TiE SV and Stanford Center for International Development (SCID) on Dec 2 at the Stanford campus.

This conference will bring top 30 business software startups from India to the US with aim to foster cross-border partnership and potential strategic opportunities.

The conference is designed to be a symbolic and relationship-building bridge between top Indian SaaS and deep tech startups and US companies, to forge long-term relationships.

Mr. MJ Akbar, MoS, Ministry of External Affairs, brainstorms with iSPIRT.

Mr. MJ Akbar is the Minister of State (MoS) for External Affairs and a Member of Parliament in the Rajya Sabha. An author of several best-selling books, and a veteran Indian journalist who launched newspapers like The Telegraph, The Asian Age and magazines like The Sunday. Mr. MJ Akbar, met up with iSPIRT, in Bangalore to understand the plethora of Technological Breakthroughs that iSPIRT is facilitating to empower more than a billion Indian citizens, by deploying technology in the service of humanity. Mr. MJ Akbar has also agreed to co-create an era of Innovation Diplomacy, by using Software as India’s Soft Power. He provided some very useful advice by participating in interactive sessions for close to 2.5 hours.

On Saturday, at ITC Gardenia, in Bangalore, Mr. MJ Akbar, along with Mr. Bala, Jt Secy, and his team, consulted and deliberated extensively, on opportunities that can be Game Changers for Innovation Diplomacy. iSPIRT with its team of Volunteers which included Sharad Sharma, Sanjay Anandaram, Sanjay Jain etc, along with several innovative startups, presented various breakthrough solutions that are helping India leapfrog the West.

Below are some of the key highlights of the Learning Session.

iSPIRT Show-case – INDIA Going from Software Services To Software Products & Platforms.

The session started with a presentation by Sharad Sharma on how India is transforming itself to Software Products and Platforms. He explained how iSPIRT with IndiaStack is helping new-age startups to build platforms which will drive formalization of the Indian economy. This will materially enable Financial Inclusion, Health Inclusion and provide access to more than 200 million households, by digitization and democratization of essential services, and in-turn will create millions of jobs.

Mr. Akbar’s feedback on this session was that we should highlight stories and narratives which resonate with the aspirational identities of people. Like how did India manage to reach MARS? This was an interesting segway, to then have about 8 startups including Team Indus present their stories. Team Indus, is planning to be the 1st private organization in the World, to land a rover on the moon in Dec 2017.

The remaining 7 teams which presented their stories included companies like Pratco, Foradian, Forus, Indian Money, Knolskape, Hashnode, Niramai. Covering Healthcare, Education, Finance, Technology and Medical Devices, these Startups showed how they are helping millions of Indians not only in Tier 1, but in Tier 2 and Tier 3 India, leverage technology, and avail critical services at a fraction of the Global Cost. It affirmed that yes, while America innovated for the 1st One Billion, India can innovate for the next 5 Billion.

The last session, was by Sanjay Anandaram, who made an intense pitch, for using Software as an Instrument of India’s Soft-Power. India needed to leverage its highly credible and respected brand in global IT to use effectively for political-economic leverage. The 3 pillars for this could be (a) “Digital Non-Alignment” ie advocating Net-Neutrality, (b) “Governance for Hire” ie offering the India Stack to countries in Asia and Africa for running of their programmes and (c) Software as an integral part of bilateral and regional trade deals. Software was an area where India can outmaneuver China in Innovation Diplomacy. India has the requisite legitimate & moral authority to make software a key instrument of its foreign policy to achieve its political-economic goals compared to any other nation.

Insights and Advice from Mr. MJ Akbar

Mr. Akbar was impressed by the Innovation Diplomacy agenda and commented that India would make an orbital shift in the Arab, West Asian and African region with its Knowledge Capital and Strategic Advocacy of Shared Prosperity. He advised that some of the Startup stories of India should be used to co-create external affairs initiatives of the Govt. of INDIA. He gave several golden nuggets of advice, like Value of Knowledge increases only when it is given away for free. Hence a partnership towards Shared Prosperity in the Knowledge economy is vital. Listed below are 5 important pieces of advice given by Mr. MJ Akbar

Empires are not built by Armies, (giving the Genghis khan example), they are built by Technology, Skills and Communication.

Why does a country like India, which had such sophisticated science & architecture like Step Wells (Bawadi) even in the 10th century, keep getting defeated?

We need to showcase to the World, with good statistics, what we represent in terms of Technology and Communication.

We need to highlight to the World that the Frontiers for the Future Lies with INDIA.

Knowledge Economy should connect emotionally with the Global audience to realize Shared Prosperity.

Conclusion

Mr. MJ Akbar set in motion a few immediate co-creation steps to learn how Innovation Diplomacy can become the bedrock of India’s External Affairs. Being a veteran journalist, he definitely had more powerful narratives to showcase Software as India’s Soft Power. As usual, iSPIRT on its part is fostering and facilitating many such learning sessions to co-create with our Law Makers, and nudge our Policy Makers to help the Software ecosystem. Let us all align our collective vigor to catalyze the effort of building India’s Software Strength to be its Global Soft-Power.

I am Taron Mohan, CEO of NextGen Tele and an iSPIRT Volunteer. I usually meet many CXOs of Banks for selling mobile-SIM-overlay based financial inclusion solutions. This one time I was on an email thread with the CEO of a big Public Sector Bank with other iSPIRTers. The discussion was about India-Stack. In my entrepreneurial zeal, I pitched my NextGen Tele SIM-based solution. I quickly realized that this was a mistake. I knew instinctively that I should not use an iSPIRT session to further my own private self-interests. iSPIRT’s credibility comes from Volunteers like me putting India first. While working for iSPIRT we set aside our personal gains for a larger cause of building a Product Nation.

I’m now an advocate for all of us Volunteers signing a Volunteer Code-of-Ethics that sets clear expectations from all of us. This would help us maintain the high standard that we all hold ourselves to. So, working with the iSPIRT Fellows Council we drafted the Volunteer Code-of-Ethics. I have signed it and will abide by it. I plan to even assert my iSPIRT Volunteer Code-of-Ethics in my email signature.

iSPIRT Volunteer Code-of-Ethics

As an iSPIRT Volunteer, I am committed to making India a Product Nation. At no point in time, I shall use my iSPIRT Volunteer status to further my private or business interests. I hope to set a high ethical standard and be an example to others.

On Behalf of the Fellows Council –

Manjunath Nanjaiah, Thiyagarajan(Rajan) & Sharad.

I participated as a volunteer this time around and missed the keynote in day one since I was busy in printing #MindFlip worksheets for 50 odd entrepreneurs. These entrepreneurs were handpicked by a very credible set of people who knows what #Scale means to B2B products.

Pallav and Shankar Maruwada did the priming by asking all the founders to reflect and redefine themselves within a framework that was designed carefully. Here not only they were asked to redefine who they are but were asked to open their heart and mind to play ping pong shooting game with co-participants sitting next to them. Learning to allow others become your mirror is a great way to identify your mistakes faster. These hard hitting peer challenge just bring the hidden self and does the world of good and the benefits will longer. Once they know who they are, they were told to pitch for a different context and at a different level. Mentors and peers played a critical role here and acted as an investor, prospective employee, customer etc.

When Phani talked about how he was lucky and all that happened around him at RedBus just happened and he just sailed through the wave. With all that humility he then explained if he had to present something like Girish, it will be something. The contrast was visible and it was beautiful as nature painted on a canvas. Girish spoke about #GoodScale he narrated the techniques that helped him to shape up Freshdesk. These techniques are not #GrowthHack these are practices that have been experimented, hammered and perfected. The honesty and ability to open up without ego, self-promotion was incredible to see.

Learning sales funnel from people like Aneesh, Suresh, Girish is like dream come true and Aha moment for many. These are something that can be practiced and implemented the next day !!

Manav re-iterated that it’s all about Sale-Sale-Sale for the founders to win. It truly amazing to listen how he closed big deals or key hires over cup-of-coffee, I personally loved the way Manav has navigated the journey by increasing his target market size with one step at a time. Solving one problem at a time and then moving to adjacent space which made it easier to traverse instead of starting big from day one.

Preparing for Final Pitch Selection within a cohort

The mentors were in no mood to get the feel-good emotion to sync deep inside founders, while some of them were in the go-kill-it mood, Sanjay Anandaram, and Sanjay Deshpande did a Jugalbandi and helped people to come down to earth from cloud 9. While everyone one builds a multi-billion dollar business it is also important to understand what the expiry date for the things that we do and then taking the smaller exit when appropriate does a world of good to the founder and as well as the country.

There were some discussions around “let go” — while good scale requires founders to realise it’s important to let go things and have other participate in growth, however depending comfort one could choose to hands-off-and-eyes-on model. Lots of participants participated in this discussion and shared how this could become the biggest bottleneck to scaling.

Building #ProductionNation is not an individual effort and is no less than #FreeDomFight for a country like India. People compare everything we do with #SiliconVally. However, I can’t imagine whether #PNGrowth is possible in #SiliconVally where successful founders will come and spend 3 days apart from spending days together in preparing the content and structure of the program during the last couple of months. The selfless attitude and ability to open their armouries to a group 70 odd startups are simply amazing to see.

Signature Club Resort at Brigade Orchards was amazing in the evenings. Hanging out with 50+ founders with DJ Music and beer gets even better. Ashish Tulsian and Vinod Muthukrishnan are shining star and we discovered them during last PNGrowth. After the heavy and long day, there is no better way than chilling with them. Their unique ability to hold a large group of people and make them laugh is just unthinkable and you can only relate to it if you have been part of the show before. This time the VC teardown in front of a VC was just the killer effect of the whole event !!

Mentors and Volunteers

Hope this has shaken and woken up some of the founders and they will carry all that they got and move from #HappyConfused state to a 100 Million dollar or more startup in years to come.

I am so fortunate to witness this event. Great learning for me as well even though I was not able to sit through all the sessions. My biggest learning: everything has an expiry date and learning how to map that to what I do is key to success small or big !!

RBI relaxes Foreign Venture Capital Investor (FVCI) norms for Startup investment

One more announcement to the stay-in-India check list has come from RBI with respect to registered under SEBI (FVCI) Regulations, 2000.

RBI has announced amendments to the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2000, notified vide Notification No. FEMA 20/2000-RB dated May 3, 2000, as amended from time to time (Principal Regulations).

Sanjay Khan Nagra, iSPIRT volunteer talks about this announcement in the video embedded. Below. Also the main provisions and text is described in this blog below. Those interested in the original regulation may visit this page here.

As per the amendment notification referred to above, any FVCI which has obtained registration under the Securities and Exchange Board of India (FVCI) Regulations, 2000, will not require any approval from Reserve Bank of India and can invest in:

1. Equity or equity linked instrument or debt instrument issued by an Indian company whose shares are not listed on a recognised stock exchange at the time of issue of the said securities/instruments and engaged in any of the following sectors:

(i) Biotechnology

(ii) IT related to hardware and software development

(iii) Nanotechnology

(iv) Seed research and development

(v) Research and development of new chemical entities in pharmaceutical sector

(vi) Dairy industry

(vii) Poultry industry

(viii) Production of bio-fuels

(ix) Hotel-cum-convention centres with seating capacity of more than three thousand

(x) Infrastructure sector (This will include activities included within the scope of the definition of infrastructure under the External Commercial Borrowing guidelines / policies notified under the extant FEMA Regulations as amended from time to time).

2. Equity or equity linked instrument or debt instrument issued by an Indian ‘startup’ irrespective of the sector in which the startup is engaged. A startup will mean an entity (private limited company or a registered partnership firm or a limited liability partnership) incorporated or registered in India not prior to five years, with an annual turnover not exceeding INR 25 Crores in any preceding financial year, working towards innovation, development, deployment or commercialization of new products, processes or services driven by technology or intellectual property and satisfying certain conditions given in the Regulations.

3. Units of a Venture Capital Fund (VCF) or of a Category I Alternative Investment Fund (Cat-I AIF) (registered under the SEBI (AIF) Regulations, 2012) or units of a Scheme or of a fund set up by a VCF or by a Cat-I AIF.

iSPIRT believes these announcements have made Govt. Recognize the importance of opening up investment to promote innovative startups. Right now these announcements are limited to Startups recognized by DIPP. However, we hope in future they may be opened for all startups and an easy investment regime in Indian from foreign funding source.

Think about endgame, chess grandmasters do so to win.

Studies point out that chess grandmasters visualize the chess board state few steps away to a ‘winning game’ and make moves based on memory pattern that can lead to that board state and thus help them win the game.

Many startups however operate in a game where the rules are dynamic and change unexpectedly. An unanticipated flood of competition could sweep in, or the ground gets shaken underneath because of a regulation or policy change. Due to such unpredictability most of the founder’s move is extremely tactical, the focus is in on surviving and not getting killed as opposed to planning to grow like rabbits.

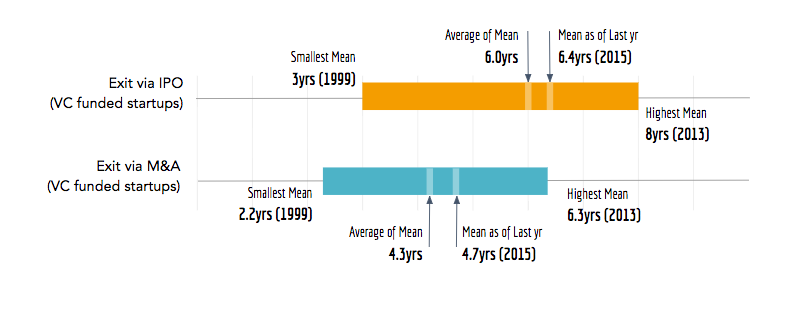

Data from 20 years of startups in US suggest mean time to exit is 4th and 6th year.

Mean exit time for startups

This is simply because If investors don’t do that then they can’t return the capital to their own investors (i.e limited partners) within the 10 year fund cycle.

Same data also reveals that after 1997 there has been more exit through M&A than IPO both in terms of count and value which means that it is more likely for a startup to have an exit via M&A rather than an IPO as the most likely route

VC vs M&A vs IPO

In India with no IPO route, M&A is the most likely endgame

On decade long VC scale, Indian ecosystem is quite young and thus historical data is not available to compare however similar forces broady apply.

Also while scale can become large but technology market growth rates in India are not as fast the US. Add to this the fact there is no IPO market in India for the technology companies. Some efforts are underway to open it such as the new ITP platform by SEBI but nothing has kicked in practice. That makes M&A option all the more important to consider for an Indian startup founder.

From limited data that is available about the Indian ecosystem we can that $14.5 billion of VC money has been invested in last 4 years and $2.5b of exits have happened in the same period spread over 300 deals. This ratio are still very skewed when compared to other ecosystem.

India M&A / VC Ratio – Low

All of this build the strong case for why an Indian startup founder should think about exits via M&A

A reason they don’t think about it is because they don’t know much about exits or the playbook involved in doing that. Second likely reason could be that advisors actively discourage founders from thinking about exits by labeling them opportunistic and not being a visionary founder.

Paradoxically the right time to think about exits is exactly when an exit is not needed.

Founders should think about exit before they are forced to think about it

PS: Exit has a broader significance, applies to open source and even countries. Here is a talk by Balaji Srinivasan that illustrates the importance of exit as key lever of an healthy ecosystem

The November 8th announcement of demonetization of Rs 500 and Rs 1000 notes by Prime Minister Modi caught everyone by surprise. That was the intent. It is, however, widely expected that bank accounts, plastic cards and digital money usage will increase dramatically in the next 12 months. In other words, India will be pushed towards a cashless economy. The purpose of this piece however isn’t about the probability of a cashless economy happening; It is about the definite opportunity presented by the Indian kaysh-less economy. That is, the economy resulting from the removal of hair from people’s heads. India has been going kaysh-less for millennia. It is our kaysh that adorns the heads of Western celebrities like Lady Gaga, Beyonce, Naomi Campbell and any “Hollywood who’s been a mile of a first class weave” according to Mother Jones. It is Indian kaysh – renowned for its length, quality and strength – that is most prized in the making of wigs, weaves and hair extensions (“dry hair”) used by women in the West.

Annually, India exports about 1,300 tons of hair- 80 per cent of the world’s supply – contributing to about US$400 million in revenues and employing thousands in the collecting, cleaning and sorting activities. Our temples sell the best quality hair – 20-30 per cent of all hair is harvested in temples – while barber shops and women’s combs and garbage bins generate the rest. Temple towns like Tirupati in Andhra and Palani in Tamil Nadu are on the world map for their hair exports. In 2013, Tirupati alone generated Rs 200cr from e-auctioning of 106 tons of hair; 25,000 heads are shaved daily in Tirupati where over 600 hairdressers are employed including 50 female barbers. Rural women who get their heads tonsured have prized natural long hair because it is uncontaminated by shampooing and styling chemicals. The significantly less lucrative shorter men’s hair on the other hand is mostly for industrial use eg stuffing clothes, fertilizers and for extracting L-cysteine, an amino acid. It is worth noting that this acid is used in pizza dough and bakery products so spare a thought the next time you bite into pizza and actually find hair in it.

Indian hair is closest to Caucasian hair and is the most heavily priced thanks to it being “remy” ie single cut and orientation of the cuticle. The remy hair from India goes largely to the US and Europe while the non-remy hair goes to China.

The Indian kaysh-less economy can be a global multi-billion dollar market opportunity; Interestingly, Africa alone offers a US$6billion opportunity that Indian companies can target. If only we considered it as such and, instead of just being a supplier of the primary commodity, got into the higher value-added products of branded dry hair. Instead, even in kaysh, like most things that originate in India, someone else is actually harvesting the serious cash! China, on the other hand, generates $2billion from its supplying dry hair products by partly using Indian non-remy kaysh!

India’s domestic kaysh-less economy – as a leading supplier of the best quality human hair – can provide a very lucrative cash generating opportunity for Indian beauty and wellness companies.

With 1.25billion people, India’s original kaysh-less economy isn’t an hairy-fairy business; It is hair today and definitely not gone tomorrow. The country needs a Big Hairy Audacious Goal. All we have to do is say, “hair! Hair!” to that. Will we?

Playbook Round Tables were created with an intention to orchestrate the coordination and exchange of tacit knowledge. Thoughtful Founders acted as facilitators in this sharing of tacit knowledge. We call them Mavens. For them, their contribution to #PlaybookRTs was a labor of love. It is a selfless contribution to making India a Product Nation.

Thanks to the Founder Mavens, PlaybookRTs went on to become very successful. The topic coverage grew. However, we were not able to find Founder Mavens for topics like Design Thinking and Inside Sales. We wondered if we should look for Mavens who were not Founders. But we were skeptical if they would be animated by the Product Nation mission. And, even if they were, would they contribute selflessly in a pay-forward manner that the Founder Maven did? Would they sign the Maven Code-of-Ethics?

Then we ran into Deepa Bachu.

Her commitment to making India a Product Nation was there. Yet we wondered if she would be willing to pay-forward in PlaybookRTs. We knew this was not an easy call to make. After all, it meant forgoing workshop revenue from product startups for the foreseeable future. As we talked, we realized that Deepa’s dilemma wasn’t whether she should make this selfless contribution! Instead, she was worried if the PlaybookRT attendees would value something that was free!

This led to a couple of experimental PlaybookRTs.

And here we are! Deepa learned that Sometimes Free Is Valuable. And we learned that there are contributors to the product ecosystem who will put the cause before their business. We find that the Practitioner Mavens are as vested in the pay-forward model as Founder Mavens. We cherish and value both of them.

A recent article by Andy Mukherjee, predicting the end of India’s IT industry has caused lot of commotion. Though, the ‘end’ is an exaggeration, the warning of the ground slipping is not new. The declining growth is owing to the rapid transformation in technology and Software Industry itself, globally.

The first Software policy of 1986, resulted into Software Technology Park (STP) scheme in 1991. Undoubtedly, the policy was highly successful with IT industry today accounting more than 9 % of GDP.

Despite diminishing growth, even after 25 years, old Software policy (1.0) of 1986 still prevails, with focus on IT services. A reworked IT policy 2012, is generic, remained redundant with no meaningful churn out for new age Industry.

Failure to capitalize on the capability built in last quarter century can have serious consequences. The onus lies with Ministry of Electronics and IT (MeitY). However, MeitY seems to be missing on following four issues.

One, Software is core, not IT enabled Services (ITeS). Two, not able to gauge the shift in fundamental industry structure globally from ‘services’ to ‘products’ and also ‘cloud’ based products. Three, not able to appreciate ‘national competitive advantage’ has moved up the maturity curve to ‘Innovation stage’. Four, a phlegmatic approach resisting shifting gears swiftly.

To address these strategic paradigm shifts, a Software 2.0 policy is needed with ‘product’ as focal to it. We are at least 5 years late in our action here. Let us delve here into the four issues and related actionable.

Software is the focal sector in IT

It is important to understand here, that the genesis of today’s IT Industry was ‘Software’. The empirical evidence highlights real horse power coming from Software. IT enabled services (ITeS) is a derivative or related sector that grew through a ‘pull through’ effect of various related determinants (R. Heeks 2006). This is true even when we cut through the industry’s maturity stages. The ‘core’ has to be energised for new paradigm.

Product focus (new paradigm)

The big sector level transformative shift is ‘Standardised Product’ taking the center stage. This cuts across the ready Software packages (small, modular or enterprise grade), SaaS, PaaS and mobile apps.

The only subtle difference which remains is, whether a ‘product’ is sold to the end-user as ‘goods’ or a ‘product’ is hosted by SaaS or PaaS producer to provision the ‘productised service’. Even IT services business now hinges at standardised ‘products’ for revenues.

Shifting National Competitive advantage

For about a decade no one believed that Software policy 1.0 could make India a super star in Software sector. It is only after about a decade, researchers recognized that India, a developing country could become a follower nation in Software sector. This was in sharp contrast to other 2 rising countries in same period of late 1980s i.e. Israel and Ireland, who were ascribed as Industrialized nation by world bank even in that period among the 3Is.

Usually academic researchers have not been very successful in predicting or prescribing favourable industrial policy for a country. But, they have played an important role when we apply an established research for analysing a sector’s performance and understanding the needed strategic shift.

Also, the classical economics models of ‘comparative advantage’ do not fit well for a sector like Software which is replete with advanced factor conditions.

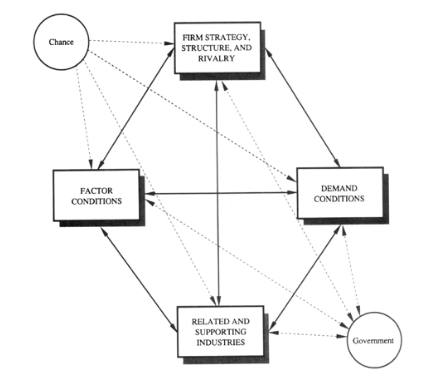

The most comprehensive model to deep delve into this search is Michael Porter’s theory of competitive advantage (The Competitive Advantage of Nations, 1990). It goes beyond the macroeconomic theories on competitiveness and also incorporates the aspects of business and industry with advanced factors such as technology & innovation. The “diamond” model is based on four main determinant categories viz. factor conditions, demand conditions, Related and Supporting Industries and Firm Strategy, Structure, and Rivalry. It also incorporates and interlinks two extra parameters of a) chance and b) Government policy. For India both these played a vital role.

Porter’s Diamond Model.Source: The Competitive Advantage of Nations, 1990, Michael Porter’s (Kindle book, position 3060)

The national competitive advantage is based on the advanced level interplay of these determinants in the above diamond, network.

The model may lack in taking into account the new emerging factors of cloud and mobility computing. Yet, it offers a comprehensive and advanced postulation that can help understand the sectoral impacts.

Richard Heeks (2006), using this model concluded the competitiveness of Software sector of India. So also Bhattacharjee and Chakraborty (2015), further building on Heeks study. Richard Heeks (2006) says, “full diamond is not (yet) in place”. Whereas Bhattacharjee and Chakraborty (2015), recognize the full diamond in place. (Please see reference below at bottom)

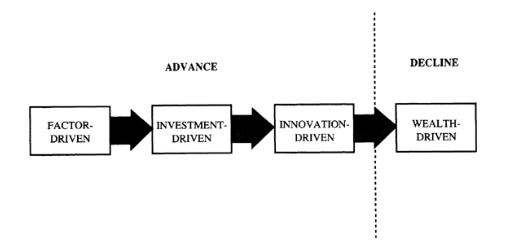

Going beyond famous diamond model, the stages of development as postulated by Porter are more relevant to understand our readiness for ‘product’ stage. The stages in order are ‘factor driven’, ‘investment driven’ and ‘innovation driven’ (the last wealth creation points decline). R. Heeks (2006) finds ‘Investment driven’ stage in 2006. Bhattacharjee and Chakraborty finds ‘innovation’ having swept in the period 2012-2015.

Stages of development. Source: The Competitive Advantage of Nations, 1990, Michael Porter’s from kindle book location 9634

“Govt. helping improve the quality of domestic demand and encouraging local startups” is representative of ‘innovation’ stage, says Heeks (2006). One can easily map here, the conditions arising to launch of StartupIndia policy 2015 and other accompanying developments.

Yet another symptom of ‘innovation driven’ stage is the domestic demand conditions undergoing a rapid change. ‘Digital India’, GST and UPI are not only concurrent, country scale demand generation programs, but also innovation boosters in domestic industry.

Porters, argues for a proactive role for cluster in National competitive advantage. The clusters enable innovation and speed productivity growth. The Silicon Valley and Israel’s Silicon Wadi are clusters that contribute to regional growth as well as making them as global brand. India has a distributed cluster model spread across various Tier 1, Tier 2 and Tier 3 cities. Bangalore, Hyderabad, Pune, Delhi NCR and Chennai being prominent.

India has enriched these clusters in the investment phase recognized by both the referred researches above.

In India, a mass of new age Software product startups has emerged touching wide array of industries. Advanced and specialized factor resources are emanating from the Software product development happening in the captive offshore center, R&D centers of MNCs or by outsourced product development (OPD) vendors, across all major IT cluster in country.

India therefore is poised for a phase 2 of Software Industry this time with product focus.

Emerging SaaS segment has global reach

SaaS can be the next game changer for India. The national competitive advantage can be capitalized for creating a SaaS industry, and puts India in first three slot on global map.

Many Software as a Service (SaaS) companies like Zoho, Freshdesk are already global market place names, pitching for leadership in their own segments. It proves the power of SaaS to give edge in exports.

Out of more than 200 SaaS companies, number of them have incorporated outside, owing to the friction in doing global business from India. Software 1.0 policy doesn’t care for their issues. This loss can be plugged with Software 2.0.

Swift action needed by Government

India’s IT sector is strong enough to face changing technology challenges. It needs a ‘product nation’ based proactive strategy, that deals with ‘product ecosystem’ development, R&D, domestic demand boosters, frictionless trade and tax regime.

MeitY should rise to the occasion and announce a macro level policy framework, without wasting further time. Action plans (schemes, programs, incentives and institutional setups) can follow on need basis and in phased manner. This is how it happened in Software 1.0 policy as well. A new institutional setup is required. ‘National Software Product Mission’ should be setup urgently to cater to emerging Software product industry.

‘Software product power’ is cardinal to retaining global Software ‘power’ tag. Globally Software product market is estimated to be $1.2 trillion by 2025. India needs to target for 10-15 % of this. At home front, India needs to create ~3.5 million new jobs by 2025. Choices are limited.

iSPIRT has been working with MeitY for last 2 years to persuade them for taking a stand for a national level product industry while the service industry keeps growing. A nine point strategy draft is under consideration. But it has taken lot of time. In hardware product space, we have National Electronic Policy 2012. A National Policy on Software Product will replenish the industrial policy basket of MeitY and usher in growth in new areas of both domestic and international trade.

“Mere incremental progress is not enough. A metamorphosis is needed. That is why my vision for India is rapid transformation, not gradual evolution”, said Prime Minister at NITI Aayog recently.

We hope the announcement of the long pending ‘National Policy on Software Product’ (NPSP) will soon be forthcoming. Only then will PM’s dream of rapid transformation, become a reality to catalyze an “Indian Software 2.0 industry”.

Main References used

1. Research article “Using Competitive Advantage Theory to Analyze IT Sectors in Developing Countries: A Software Industry Case Analysis”. By Richard Heeks, Development Informatics Group Institute for Development Policy and Management School of Environment and Development University of Manchester, Manchester, United Kingdom. http://itidjournal.org/itid/article/viewFile/228/98

2. Research paper, “Investigating India’s competitive edge in the IT-ITeS sector”. By Sankalpa Bhattacharjee and Debkumar Chakrabarti (Peer-review under responsibility of Indian Institute of Management Bangalore). http://www.sciencedirect.com/science/article/pii/S097038961500004X

3. The Competitive Advantage of Nations, by Michael E. Porter’s Free Press edition 1990

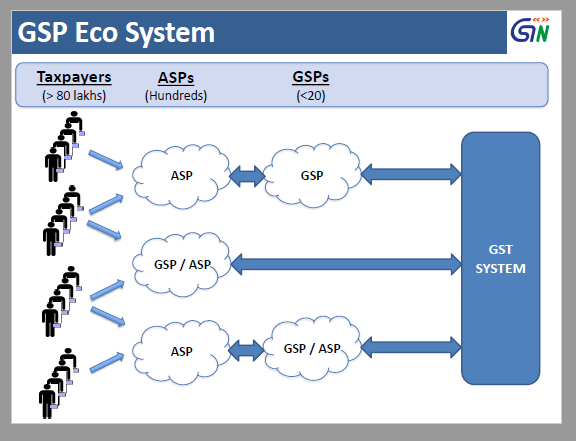

Recently GSTN invited application for becoming GSTN Suvidha Provider (GSP) under GSTN for enabling much awaited Goods and Service Tax. GSTN received total 344 applications. CEO GSTN reported in GSP workshop on 25th October that about 98 of these applicants are qualified for further evaluations according to them.

The GSP application process, when started created lot of confusion and concern on the eligibility criteria. The eligibility criteria are given here. One common concern was the financial capability criteria’s set by GSTN of:

Paid up / Raised capital of at least Rs. 5 crores and

Average turnover of at least 10 Crores during last 3 financial years.

iSPIRT had proposed that instead of a heavy turnover criterion the GSTN could have used a performance guarantee or a surety bond, both to ascertain the serious players and cover the risk of fly by night operators. This would allow some startups to take the risk and succeed to become GSPs.

The announcement did not clarify what is a GSP or what role will it have in the system.

A large number of interested startups through the GSP was about an application provider of product to file and comply with GST. Hence, the above criteria were considered as a barrier to startups. GSTN although off the record said they will accept application from all and will then evaluate who will be fit to become a GSP. This was however a very subjective approach, where GSTN will use their discretion to allow an enterprise to setup a GSP or not.

These concerns and doubts created confusion in minds of many startups, who have been looking towards the GST as an opportunity to innovate and implement in the space of tax compliance with added value with analytics and business intelligence.

It is subsequent to the workshop that many of these doubts have been cleared.

What finally turns out to be is that the GSPs are the middle layer infrastructure or utility provider or a API gateway to large number of GST filing apps. There may be a mix of GSP/ASP model where an ASP sets up a captive GSP. Even in that case GSP is merely a Gateway.

This blog is to answer some of the questions raised by participants in a Google Hangout conducted by Nikhil Kumar an iSPIRT volunteer. Additionally, it also answers other basic question with the related topic of GSP.

What is GSTN?

GSTN stands for Goods and Service Tax Network. It is a section 8, not for profit private company, with shareholding of Government of India, Government of States and UTs and financial institutions.

As a Special purpose vehicle(SPV), GSTN’s mandate is to establish, develop and manage the required infrastructure, systems, technology, partnerships and eco-system for implementation of GST.

What is a GSP?

GSP stands for GSTN Suvidha Provider. GSTN does not want to facilitate or connect to Goods and Service Tax filing application (called ASPs by GSTN and in this document) directly. This is for reasons of security and scale. Therefore, GSTN has planned a number of GSPs who will act as a middle layer between the ASPs or business and GSTN.

GSPs will facilitate the use of GSTN system to the businesses as well as products and application (developed by ASPs) to file the GST returns, match sales and purchase invoices to settle tax credits. The GSPs will hence help secure GSTN from direct exposure to users on internet as well as distribute the load in a large economy like India.

A GSP will hence act as a gateway that will pass enable the pass through of GSTN APIs (application programming interface) to and from users. There are three types of GSPs envisaged:

Plain GSP (Independent GSPs) who will just facilitate the ASPs to use them as Gateways

Captive GSPs – (GSP/ASP) used by large businesses for their API consumption/pass through. These may include ASPs wanting to become GSP and use the GSP for their APS having heavy load

Open GSPs (GSP/ASP + ASPn) who may use for their ASP and also allow independent ASPs

This is how it is depicted in the above slide shown in GSP workshop. However, during the talk on GSP workshop it was mentioned that it will be mandatory for all GSPs to allow any ASP to use the GSTN APIs. Hence, it remains to be clarified by GSTN, weather the model 2 shown in above diagram means a Captive GSP and weather a captive GSP can deny access to third party ASPs to it’s GSP.

GSTN will sign an agreement with the selected GSPs which will govern the contractual relationship between GSTN and GSPs.

How many GSPs would be allowed?

There is no final decision on how many GSPs will finally exist or be allowed. However, in the first phase, 98 GSP applicants would be allowed to participate in the technical evaluation. How many will pass or how many more will be evaluated has not been declared yet.

Who is an ASP? What is relationship between an ASP and a GSP?

Application Service Providers are – Accounting Software, Invoicing Software, Point of Sale (POS) systems and other innovative applications that can enable businesses comply with GST. ASPs can work with multiple GSPs to enable GST for their customers.

Some ASPs may also have their own captive GSP. Dominant accounting and ERP product companies may have their captive GSP as this further opens up in future.

ASPs will have a contractual relationship with GSPs that they use.

How many ASPs can exist? Does ASP is related to GSTN under a formal relationship?

As per GSTN, they do not want to control the ASPs and leave this for market forces to decide how many ASPs can be there.

ASPs are not a directly related party with GSTN. ASPs will have a contractual relationship with GSPs and GSTN will ensure the GSPs provide a free and fair access to ASPs to the GSTN resources.

Can an ASP apply to become a GSP later?

GSTN , says yes they will evaluate on case to case basis. There is no defined policy. On eligible as per the criteria laid out it in the next phase

What are the commercial terms for a GSP?

As per current information, GSTN will waive the first year charges for the GSPs. However, the GSPs would be allowed to charge the downstream ASPs. GSPs can also provide value added services on top of GSTN APIs and charge for them.

Again there is no define answer. The market will decide many things in future. For startups and small ASP players, it is important number of independent GSPs emerge for a fair and free market to exist.

Can GSP share or use Data for business?

As per announcement at GSTN workshop, the GSPs will not be allowed to share the GST data of businesses filing returns or sell the data to third parties. However, GSP can use this data themselves to create value added service offerings like business analytics and charge the individual businesses to do so. This means the data can be used to create a service offering for the given business only and cannot be cross sold to other parties. GSP will have to strictly adhere to data privacy clauses.

How will GSTN ensure third party ASPs get GSP services early on launch of GST?

NSDL e-Governance Infrastructure Limited (NSDL e-Gov) is the depository (promoted by NSE, now running infrastructure and services for many mission mode projects of Government of India. NSDL is also slated to run the GSTN services.

NSDL will provide the neutral GSP services as an official independent GSP to ASPs. GSTN thus ensures that at least one GSP is ready for third party ASP providers get a GSP to serve the market.

Will GSPs expose the same API set as per GSTN Sandbox?

As per GSTN answers to this questions, the GSPs will be legally bound to expose the GSTN APIs on a complete transparent pass through. However, GSP can provide additional rapper APIs for value add that they will like to build or management of their system.

Will the developer sandbox be available to anyone?

As per GSTN response, Yes.

Will there be any further workshops or hackathons?

GSTN may conduct these in the future. However, none planned as of now.

Where can one find the workshop PPT and other resources of GSTN?

One can use following resources of GSTN to get to more details.

At iSPIRT we are continuously involved with GSTN. Role of GST will be a game changer for India’s economy.

Our endeavour is that GSTN is able to offer a thriving platform for number of Product companies existing and new. It is also able to provide an open environment for innovation that can help some startups emerge offering valuable products to the business community.

[this blog is based on Google Hangout conducted on the topic by iPSIRT voluteer Nikhil Kumar, the inputs at GSP workshop conducted by GSTN on 25 Oct 2016 and group discussions with Bharat Goneka, Pramod Verma and Gian Franco Bonini of iSPIRT]

For one, it was the first step in breaking down borders between Silicon Valley and India. It is no easy feat to gather the top BD and Corp Dev executives from the largest tech Silicon Valley giants all together under a single roof. But with representatives from 65 corporates meeting 28 startups driving 120 connections for partnerships and investment/acquisition discussions, the very fact that the doors were opened, some even knocked down, was a giant leap for the ecosystem.

For one, it was the first step in breaking down borders between Silicon Valley and India. It is no easy feat to gather the top BD and Corp Dev executives from the largest tech Silicon Valley giants all together under a single roof. But with representatives from 65 corporates meeting 28 startups driving 120 connections for partnerships and investment/acquisition discussions, the very fact that the doors were opened, some even knocked down, was a giant leap for the ecosystem. StartUp Bridge India, with an NPS of 68%, was another valiant step towards putting the Indian startup ecosystem on the global map alongside mammoths like the US and Israel. Team Indus, an Indian startup working to land a rover on Mars, is India’s literal moonshot. Startup India, working to increase cross-border investments and M&A, was India’s figurative moonshot. And after Startup Bridge, it was clear, that this moonshop has a robust arm and is gaining an increasingly powerful momentum.

StartUp Bridge India, with an NPS of 68%, was another valiant step towards putting the Indian startup ecosystem on the global map alongside mammoths like the US and Israel. Team Indus, an Indian startup working to land a rover on Mars, is India’s literal moonshot. Startup India, working to increase cross-border investments and M&A, was India’s figurative moonshot. And after Startup Bridge, it was clear, that this moonshop has a robust arm and is gaining an increasingly powerful momentum.  The goal was to create 8-10 companies every year which would eventually go on to become $10mn revenue companies in the next 3 years.

The goal was to create 8-10 companies every year which would eventually go on to become $10mn revenue companies in the next 3 years. My next request was to get

My next request was to get  It was great to see that all the facilitators did an outstanding job of delivery of the frameworks and ensured that they shared real life stories and lots of data and numbers from their companies. What was more important was that they made sure they spent time with all the attendees and ensured they received personalised attention. They were able to build a personal connect and trust within the startup community by sharing internal information even though they didn’t have to, thereby making the discussion even more credible.