iSPIRT works to transform India into a hub for new generation software products, by addressing crucial government policy, creating market catalysts and grow the maturity of product entrepreneurs. Welcome to the Official Insights!

Author: ProductNation Network

ProductNation has been set up by a team of enthusiasts who have created a platform for entrepreneurs, employees and indeed, onlookers to share ideas, ask questions and gain knowledge about various dimensions of the software product business.

Micro, Small, and Medium Enterprises (MSMEs) are the unsung heroes of India’s economy. Employing over 11 crore people and contributing nearly 30% to the country’s GDP, MSMEs are not just businesses – they are drivers of innovation, inclusion, and local development.

On this MSME Day, we celebrate their resilience and ingenuity. But it’s also a moment to reflect on what holds them back – and how access to credit remains one of the most critical challenges they face. For MSMEs, timely and adequate credit is often the difference between scaling up and shutting down. Credit powers, yet, the reality is stark: a majority of MSMEs in India still rely on informal sources of finance or are denied loans due to lack of collateral or formal credit history.

According to estimates by the IFC, India’s formal MSME credit gap exceeds ₹25 lakh crore. Despite government schemes and fintech innovations, many small businesses struggle to access formal credit. This gap doesn’t just hurt MSMEs – it stifles job creation, reduces GDP growth, and hampers economic inclusivity.

A Shift Towards Cash-Flow-Based Lending

The good news? The ecosystem is evolving.

With initiatives like Account Aggregator, OCEN (Open Credit Enablement Network), and digitization of GST and banking data, lenders are moving towards cash-flow-based lending models. These innovations focus on real-time business performance rather than outdated collateral-based methods.

Such models enable more flexible, faster, and inclusive credit access to deserving MSMEs, especially those in Tier 2 and 3 cities.

To truly empower MSMEs with credit, the following steps are critical:

Financial literacy programs to help MSMEs manage credit and build a borrowing track record.

Policy support to incentivize banks and NBFCs for lending to first-time or underserved borrowers.

Greater public-private collaboration to build robust digital lending infrastructure.

Simplification of loan application processes through digital channels.

Celebrating MSMEs, Supporting Their Dreams

On this MSME Day, let’s go beyond celebration. Let’s reaffirm our commitment to unlocking finance for the backbone of our economy.

Whether you’re a policymaker, lender, fintech innovator, or simply a consumer – supporting MSMEs means supporting India’s future.

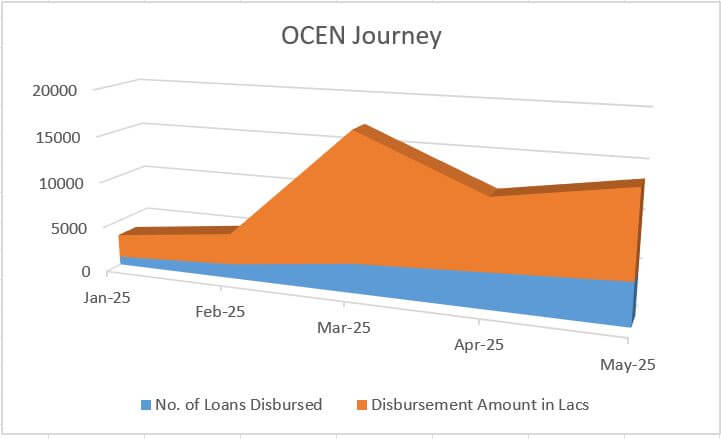

The Open Credit Enablement Network (OCEN) post its initial pilot deployment and continuous upgrades and improvements has seen growing participation across the ecosystem. OCEN’s transition from its early stages into the growth phase is now reflecting in its growing volumes and addition of new ecosystem partners.

Monthly Progress Report:

With the start of the new financial year, the April-June quarter is usually considered a sluggish season in financial services, more particularly in lending business. Corresponding trend reflects in the April performance on the OCEN traction as well, however April & May are still looking progressive in comparison to Jan & Feb performance, considering March financial year end rush as an exception. As newer products and lenders go live on OCEN, the trendline growth looks promising.

Here’s a quick look at the latest numbers on the OCEN ecosystem:

Metric

Jan-25

Feb-25

Mar-25

Apr-25

May-25

No. of Lenders Live on OCEN

7

7

7

8

8

No. of Borrower Agents Live

6

6

6

6

6

No. of Technology Service Providers (TSPs) with active deployment

2

3

3

3

3

No. of Loan Products

11

11

11

12

12

No. of Loans Disbursed

895

1567

3179

3861

4552

Disbursement Amount

₹25.17 Crore

₹33.67 Crore

₹139.11 Crore

₹76.13 Crore

₹90.82 Crore

Average Loan Ticket Size

₹2.81 Lakh

₹2.14 Lakh

₹4.37 Lakh

₹1.97 Lakh

₹1.99 Lakh

OCEN continues to engage with ecosystem partners to build the momentum for new cash flow lending products for MSMEs.

The volumes and traction on Open Credit Enablement Network (OCEN) continues to grow month on month. The growing trajectory highlights OCEN’s ability to streamline and democratise credit access for MSMEs by leveraging digital public infrastructure and fostering collaboration among lenders, agents, and technology providers.

Here is a snapshot of the OCEN ecosystem’s key updates for March:

Metric

Jan-25

Feb-25

Mar-25

No. of Lenders Live on OCEN

7

7

7

No. of Borrower Agents Live

6

6

6

No. of Technology Service Providers (TSPs) with active deployment

2

3

3

No. of Loan Products

11

11

11

No. of Loans Disbursed

895

1567

3179

Disbursement Amount

₹25.17 Crore

₹33.67 Crore

₹139.11 Crore

Average Loan Ticket Size

₹2.81 Lakh

₹2.14 Lakh

₹4.37 Lakh

As OCEN continues to evolve, it is poised to further bridge the credit gap for MSMEs, enabling faster, more transparent, and more inclusive financial support for this vital sector of the Indian economy.

The Open Credit Enablement Network (OCEN) is steadily progressing from its early stages into a more robust growth phase. With its current ecosystem participants, OCEN has started facilitating smoother credit delivery to MSMEs. At the same time, numerous other players are integrating into the protocol and developing specialized loan offerings tailored to the needs of MSMEs.

Here’s a snapshot of the OCEN ecosystem’s key updates for February:

Metric

Jan 2025

Feb 2025

No. of Lenders Live on OCEN

7

7

No. of Borrower Agents Live

6

6

No. of Technology Service Providers (TSPs) with active deployment

2

3

No. of Loan Products

11

11

No. of Loans Disbursed

895

1567

Disbursement Amount

₹25.17 Crore

₹33.67 Crore

Average Loan Ticket Size

₹2.81 Lakh

₹2.14 Lakh

OCEN continues to engage with new participants to further expand the ecosystem, adding new products and scaling up efforts to transform credit access for MSMEs on a large scale.

There is a need for a continuous conversation about the best way to shape the future of Indian cities. This conversation will take place across multiple cities, with learnings from each other.

Therefore, it is proposed to hold an ‘Imagining Indian Cities’ Workshop annually in different Indian places. The first of those took place in Bangalore from 10 to 15 March 2025, with the next two planned for Chennai and Pune.

These Workshops will gather academics, practitioners and urban innovators in multi-day get-together. Half of each conference will focus on the host city, and the other half will be for learnings from elsewhere.

This ‘Creative Bangalore’ Workshop was organised by the Indian think tank iSPIRT Foundation and supported by IISc/IUDX, IIHS and Dassault Systèmes, for bringing together various participants, chosen to form a sustainable collective capable of shedding light on a certain number of key questions and moving towards increasingly measurable contributions. Initial key questions were:

Genericity and reproducibility of the Creative Cities model developed by Patrick Cohendet

Digital Urban Data, Digital Public Infrastructure (DPI) and territorial intelligence

Placement of (Digital) Commons

Digital representations of culture

Digital representations of Wicked Problems

Results:

5 full days, hosted by Bangalore International Centre (D1), IISc/India Urban Data Exchange (D2), Sabha (D3), Indian Institute of Human Settlement (D4) and Dassault Systèmes (D5);

The Open Credit Enablement Network (OCEN) built on open network principles, unbundles MSME lending into specialized components, creating an ecosystem where different entities excel in one specific part of the lending process. These specialized entities focus on various tasks such as sourcing, distribution, identity verification, underwriting, capital arrangement, and collections. The result? A seamless, scalable model for MSME lending, made possible by OCEN 4.0.

Since its initial pilot deployment, the OCEN protocol has undergone continuous upgrades and improvements. Based on invaluable feedback and insight from ecosystem participants, the latest specifications address key challenges such as incentive alignment, dispute resolution, and network settlements through robust techno-legal frameworks. With these improvements, OCEN has already transitioned from its early stages and is now entering the growth phase.

OCEN Ecosystem Progress Snapshot:

We are now starting to publish monthly numbers of the OCEN ecosystem to build a trendline of progress.

As of January 2025, here’s a quick look at the latest numbers on the OCEN ecosystem:

Metric

Month – Jan 2025

No. of Lenders Live on OCEN

7

No. of Borrower Agents Live

6

No. of Technology Service Providers (TSPs) with active deployment

2

No. of Loan Products

11

No. of Loans Disbursed

895

Disbursement Amount

₹25.17 Crore

Average Loan Ticket Size

₹2.81 Lakh

As the OCEN network grows, it is actively engaging with new participants to expand the ecosystem and scale up with additional products. As new products and partnerships are developed, we are excited to witness how OCEN will continue to evolve and transform credit access for MSMEs at scale.

iSPIRT Foundation, a technology think-and-do tank, believes India’s hard problems can be solved only by leveraging public technology for private innovation. iSPIRT, as a think-and-do-tank, pioneered the concept of Digital Public Infrastructure (DPI)

Industry watched and waited to see if this budget will have bold, strategic announcements with long-term vision, aiming for Viksit Bharat 2047. Instead the budget has become more a tactical prescription for handling short-term economic correction.

Three themes capture our attention in the 2025 budget: The Investment in Innovation, Regulatory Reforms and MSME Credit.

Given our Product Nation initiative at iSPIRT, we were looking for bold steps in two major areas: Private sector R&D funding and Ease of Doing Business.

The funding for R&D made incremental progress in this budget. Under the theme ‘Investing in Innovation” the Finance Minister announced Rs. 20,000 Crore to be allocated from the policy announcement of 1 Lakh Crore made in previous budgets. There is no major decision or clarity on how this funding will be routed. In addition, intent is expressed to explore a Deep-Tech fund in the future.

Similarly two welcome announcements towards achieving strategic autonomy are, an outlay for 20,000 crore to develop Small Modular Reactors (SMR) and operationalise at least five indigenously developed SMRs by 2033 and, a National Geospatial Mission to develop foundational geospatial infrastructure and data.

There is a marked improvement in intent to solve the Ease of Doing Business (EoDB) problem in the budget made evident by yesterday’s Economic Survey.

We have been pursuing the Government of India (GOI) on EoDB to implement a comprehensive three-pronged approach, to bring India into the top 5 or 10 EoDB countries. This includes decriminalising 1200 provisions; rationalising multiple laws and implementing a National Regulatory Compliance grid at the center and then extending it to states. Our approach gels with the “Whole of Nation” thinking given by the Honorable Prime Minister.

The GOI appears to reflect this thinking in the statement, “A light-touch regulatory framework based on principles and trust will unleash productivity and employment. Through this framework, we will update regulations that were made under old laws. To develop this modern, flexible, people-friendly, and trust-based regulatory framework appropriate for the twenty-first century…”.

However, the specific action of forming a High-Level Committee for regulatory reforms that “will be set up for a review of all non-financial sector regulations, certifications, licenses, and permissions”, is welcome but appears to be incremental in nature and a slow-moving approach.

The Janvishwas 2.0 announcement has also been repeated stating 100 items to be taken up instead of 1200 reported by us.

Sudhir Singh, iSPIRT’s policy expert volunteer said, “The concept of digital transformation through National Regulatory Compliance Grid (NRCG) has been ignored in the budget. However, another idea of “Digital Port”, pursued by iSPIRT for more than two years now, on digital transformation of cross border trade has received attention and GoI seems to have framed it as ‘BharatTradeNet’ in the budget 2025.”

The budget speech states, “a digital public infrastructure, ‘BharatTradeNet’ (BTN) for international trade will be set-up as a unified platform for trade documentation and financing solutions”. This indeed is an important and welcome announcement.

The Finance Ministry’s move to separate R&D funding and Startup funding is encouraging. The startup-related announcements reflect the government’s continued support to startups.

The government has taken several steps to boost credit enablement for SME and Nano enterprises, a significant part of Priority Sector Lending. Some good announcements were made such as the Kisan Credit Card (KCC) limit increasing from INR 3 lakh to 5 lakh, which in three states – Karnataka, Maharashtra and Uttar Pradesh – is based on Open Credit Enablement Network (OCEN), an initiative of iSPIRT. Other welcome announcements include an increase in credit guarantee cover for MSMEs from INR 5 crores to 10 crores, introduction of customized credit cards for MSMEs, and capital infusion into select public sector banks.

A new Fund-of-Funds with a fresh contribution of another 10,000 crore has been announced. It is encouraging to see the time limit for u/s 80-IAC to avail income tax exemption benefit for startups has been extended by 5 years to 01.04.2030. Another announcement of interest for startups is an extension of credit credit availability with a guaranteed cover of INR 10 crores to 20 crores, with the guarantee fee being moderated to 1 per cent for loans in 27 focus sectors important for Atmanirbhar Bharat.

iSPIRT cofounder Sharad Sharma said, “It is heartening to see private sector R&D funding rolling out with a 20,000 crore fund allocation. Formation of Ease of Doing Business (EoDB) committee is also welcome. However, there is a need to take big moves and expedite these steps to meet 2047 deadlines. BharatTradeNet is a welcome announcement and we hope there will be a thorough and transparent industry consultation on it. Overall we are missing bold and specific actions on Strategic Autonomy and Product Nation. “

About iSPIRT Foundation – We are a non-profit think-and-do tank that builds public goods for Indian product startups to thrive and grow. iSPIRT aims to do what DARPA or Stanford University did in Silicon Valley for startups. iSPIRT builds four types of public goods – technology building blocks (aka India Stack), startup-friendly policies, market access programs like M&A Connect, and Playbooks that codify scarce tacit knowledge for product entrepreneurs of India. For more, visit www.ispirt.in.

In the evolving landscape of financial inclusion and digital lending, India has introduced several innovative frameworks designed to streamline access to credit, enhance transparency, and create seamless financial ecosystems. Among these, the Unified Lending Interface (ULI), Open Credit Enablement Network (OCEN), and Account Aggregator (AA) stand out as key initiatives aimed at modernizing the way credit and financial data are managed.

While all three initiatives aim to transform the lending sector, each has distinct roles, benefits, and functions. To better understand their unique features and how they interact with one another, we’ve put together a detailed comparison chart.

This side-by-side breakdown helps you identify the core differences between ULI, OCEN, and AA, their respective use cases, and how they collectively contribute to building a more inclusive and tech-driven financial ecosystem in India. Whether you’re a fintech enthusiast, a policy maker, or simply looking to understand the future of credit access, this comparison will offer valuable insights into these transformative frameworks.

ULI(Unified Lending Interface)

OCEN(Open Credit Enablement Network)

AA(Account Aggregator)

Purpose

Standardized API interface for Lending institutions providing borrower’s financial and non-financial data from various sources, including government databases, and financial institutions. Helps financial institutions to reduce friction for accessing the information needed for quick loan underwriting decisions and efficient loan application processing.

OCEN is a framework of application programming interfaces (APIs) for interaction between lenders, loan agents, collection and disbursement partners, derived data providers, and account aggregators OCEN facilitates flow of credit between borrowers, lenders, and credit distributors using a common set of standards. Various participants in the credit ecosystem can seamlessly connect with one another without needing to build customised APIs and infrastructure. OCEN aims to enable cash-flow based unsecured financing for MSMEs as against balance sheet and collateral based financing. Both ULI and AA can be derived data providers in the OCEN ecosystem.

The Account Aggregator (AA) framework allows users to share consent driven financial data across institutions. Users can access their financial information from multiple institutions in one place, and can decide who can access their data, for how long, and for what purpose. The FI Types are managed by ReBIT.

Users

Regulated entities like Lenders, etc

MSME-focused Borrower Agents and Lenders. Other ecosystem participants include Derived Data Providers, Collection Agents, Disbursement Agents and KYC Partners

Financial Information Users which are Regulated entities and Individuals who wish to access their own financial details

Key Functionality

Enabling RE’s and Marketplaces to fetch different types of financial and non-financial data for underwriting using standard interface.

Standard rails to connect various participants in the Cash flow based MSME lending ecosystem. Enabling building customised credit products for MSMEs and empowering the Borrower agent as a lynchpin and a representative of the borrowers.

Providing safe, user-consented sharing of financial information between regulated financial institutions via the Account Aggregator framework. Individuals can have a holistic single source to view financial data across various institutions.

Data Usage

Utilizes borrower data from diverse sources like banks, land records, and financial history.

Utilizes specific business data of MSMEs like invoices, transactions, etc., for the credit product creation. Any kind of data can be passed to the Lender in the form of derived data. For eg. Government e-Marketplace shares borrower performance data with lenders post consent.

Uses consolidated financial data like bank accounts, GST, income, etc., from FIPs.

Role in Ecosystem

Streamline credit access by integrating borrower data from multiple sources for accurate financial assessment, enabling faster loan approvals through advanced analytics, facilitating easy integration with standardized APIs, and providing lenders seamless access to comprehensive borrower information to simplify credit appraisal and reduce documentation

Fosters innovation in MSME credit by enabling tailored loan offerings and faster credit flow thus enabling access to credit to MSMEs which earlier did not have access to the same. Reduce cost of short tenure, low ticket lending and making it viable to give loans to MSMEs which are end use controlled and enable collection control.

Promotes financial inclusion by simplifying financial data sharing and improving credit decision-making. Allowing user to share their data directly with financial institutions in a consented manner removing the data passing through multiple hands.

Technology Backbone

Consent-based data-sharing infrastructure; APIs to connect various data sources with lenders.

API infrastructure based on standard OCEN protocol for credit enablement. Participant and Product registries to enable discovery and standardisation within the ecosystem.

API-driven, centralized consent architecture defined by ReBIT under the RBI framework.

Regulatory Framework

Proposed under RBI’s initiative to enhance digital lending infrastructure.

Digital Public Infrastructure at a mass roll out stage. Once formalised will be managed and regulated as advised by regulators.

Governing law is the RBI’s Account Aggregator framework under the NBFC-AA license.

Use Cases

A farmer applies for a loan to purchase farm equipment. Lender is able to access land records and other non-financial and financial data through ULI interface to underwrite the loan application.

Zomato as a Borrowers agent on behalf of restaurants enrolled on its platform being able to offer custom loan products specifically built for restaurant partners by the participating lenders based on alternate platform data, ability of providing collection control to lenders via cash flow entrapment and acting as a representative of the borrowers instead of agent of lenders. Like Zomato any of platforms or institutions (like FPO) sitting on a Captive database can utilise OCEN to enable lending on their platform benefiting their users.

Individuals being able to share their multiple bank accounts for specific time periods and for specific purposes with the AA framework using consent mechanism. Businesses being able to share GSTN data to RE’s for loan underwriting purpose using consent mechanism.

Implementation Stage

Proposed platform; Some pilot Implementations for certain data sources have been done. Overall the ULI is in a development phase.

Few pilots – GeM Sahay, GST Sahay, Jan Aushadhi Kendra and Private network have been successfully tested. More implementations are underway at various stages and gaining traction.

Well-established under the RBI’s regulatory framework with multiple FIP’s and FIU’s already integrated.

This workshop was organized by the Indian think tank iSPIRT Foundation, French Embassy in India, Consulate General of France in Bangalore, and La French Tech in India, based on the following principles:

Gathering high level contributors from India and France: industrials, transdisciplinary academics, diplomats, officials, business founders, think tank members, technology makers;

Pushing a Workshop format (not an event, not a round table, not a scientific conference), organizing 3 different days with 3 different viewpoints:

Philosophical/epistemological/ human sciences,

Economical/techno-legal/social sciences/adoption,

Application domains and use cases (Health, Culture, Creative Cities, Agriculture);

Targeting recommendations toward the AI Action Summit (Paris, February 2025).

Results:

More than 80 speakers, 100 participants in person (in Bangalore or in Paris), 200 participants online;

14 different countries represented all over the world (India, France, Canada, USA, Mexico, Guatemala, Brazil, Germany, Netherland, Italia, Spain, Portugal, Belgium, Thailand);

An opening session figuring the Ambassador of India to France H.E. Mr. Jawed Ashraf, the French Digital Affairs Ambassador H.E. Mr. Henri Verdier, the Consul general of France in Bangalore Mr. Marc Lamy;

Many of you asked when the volunteer programme would be available to apply, and here we are again. We do have some changes, though, so please pay attention.

This application process will be available only for the next couple of months and close by December 20th, 2024. It’s on a rolling basis, so apply immediately.

Many of you are already familiar with iSPIRT and its activities; this is your chance to join this volunteer movement. So take some time to review the programmes listed and watch the videos, not just the current ones but also the previous ones, to better understand the journey. Also, please read the Playground Coda and the Volunteer Handbook.

Are there tools we can help build to solve privacy issues, or what kind of packets will help get the internet to remote parts of India? Do you have a better solution to some pressing matters discussed in the videos? Then, you need to apply. Some legacy options and some new options are also available.

Is there some project that strikes your fancy, some part that calls out to you, and you know you can do it? To apply, click this link and follow the process.

I am reminding you again that the deadline is December 20th, 2024.

A journey with iSPIRT is also about the journey with yourself.

A gathering of iSPIRT volunteers in Bangalore turned into an interesting discussion: How does India become a Product Nation by espousing values that are inherent and ingrained in us as Indians?

Here are some answers from that meeting. We hope this gets you thinking on how to draw inspiration from familiar cultural concepts while building for India!

In any culture where people have performed well in achieving a goal, that culture has encouraged training one’s mind. Mental performance therefore is key.

For example, Americans athletes do well at the Olympics. If you look at American culture, it champions working hard, winning, and training your mind to focus on winning.

You have the Japanese concept of Ikigai, where purpose gives you a reason to live a long, happy life. The authors who wrote a book on Ikigai shares a Japanese proverb that says, “Only staying active will make you want to live a hundred years”.

Or let’s take the theory of Flow. It’s a state of mind where we are so immersed in the joy of our work “that nothing else seems to matter”. In a state of flow the mind is trained to focus and enjoy a task, even the challenges that come with it. As iSPIRT volunteer Rinka Singh says his best work happens when he is having fun framing questions and thinking through challenging problems.

So, what of our culture do you think can help us train our minds to be disciplined and dedicated? And can teach us to enjoy our work even in tough times? Here are some examples iSPIRT volunteers shared at the meeting:

After all the culture we have grown up in has cultivated some great skills in us. To give you real life examples, look at the artist who is capable of creating exquisite, complex Rangoli designs or take the Indian programmer who is a whiz with math and logic.

Or take the Bhagavad Gita teaching us not to be attached to an outcome but simply focus on doing your tasks well. The less resources your mind spends obsessing about an outcome, the more time and focus your mind has to work on completing tasks really well. In addition, when you are not attached to an outcome, your mind can deal with failure much better. It becomes easier to retrain your mind to learn from failures and simply try again.

As iSPIRT volunteer Girish Elchuri says, “no greed, no glory” is the basic theme of thinking beyond self. It helps to expand your view beyond you to help find good solutions that can benefit those around you.

Or for example take how Indian culture also values family time, food and meditation or prayer. These could potentially create a better balanced healthy mind that can focus longer, and is less prone to burnout and depression.

iSPIRTer Shoaib Ahmed believes the powerful action of placing palms together and greeting each other Namaste is truly us saying, ‘the divinity in me recognizes the divinity in you’. This invisible force of divinity running through us all connects us and lays a sound foundation for Indian product builders to collaborate at a soul level.

Referring to the Bhagavad Gita, iSPIRTer Sharad Sharma reasoned that the essence of Gita is having confusion in your life and that having confusion in your life is not a bad thing, as long as you can take a step back to look at it philosophically and figure out the answer. What Indians are good at is reframing the problem. Gita is about reframing the problem and saying ‘don’t look at it the way it looks to you now. Let me tell you an alternative way of looking at the problem and that alternative way will help the answer to reveal itself.’

“Indians succeed because we can reframe the question at a higher level of abstraction and find answers, which to me is R&D. We can be the best R&D nation in the world”, is Sharad’s learning from what he has learned from the Gita.

iSPIRT’s Hari Subramanian feels the one core part of India’s culture over the centuries has been to question and constantly learn, seek knowledge. Hari feels this ability to question will propel India’s current generation of young builders to make us a Product Nation.

As Hari puts it, “The essence of Gita is, you are born to do something. Do that and don’t be tied down to what the outcome may be. Do what you are born to do, day in, day out and excellence will follow.”

To conclude, we have a golden opportunity to change India for the better by combining the ethos of US, Japan, and India. Let’s not miss it.

Let us take the YOLO spirit of the US. Let us learn from Japan that doing your tasks well means to master it. Then let us embrace the Indian principle of not worrying about the outcome but only focusing on your work and allowing excellence to follow. If we combine all this maybe magic can happen.

In this insightful dialogue, Sagar Parikh engages with Deepak Sharma to explore the transformative potential of cash flow lending for Indian MSMEs. Deepak underscores the significance of democratizing credit access through short-tenor and small-ticket loans, especially for micro-enterprises that comprise 99% of the MSME sector in India. Drawing from his rich experience in banking and financial services, Deepak Sharma provides invaluable guidance on navigating the complexities of B2B financing, highlighting the critical role of innovative lending models in fostering inclusive growth.

Deepak Sharma delves into the pressing challenges faced by MSMEs in accessing financing, particularly in the realm of B2B transactions. Leveraging his extensive experience and deep insights, he offers a fresh perspective on the traditional lending landscape, emphasizing the need for agile and tailored solutions to empower MSMEs. By advocating for cash flow-based lending and trust-based scoring systems, Deepak Sharma presents innovative approaches to address credit gaps and unlock opportunities for sustainable economic development within India’s dynamic MSME sector.

Deepak Sharma’s perspectives on banking innovation and financial inclusion provide several key learnings for the industry:

Leveraging Technology for Inclusion: Sharma emphasizes the transformative impact of technologies like UPI and Aadhaar in fostering financial inclusion. These initiatives not only revolutionize digital payments but also open doors to credit access for underserved segments like SMEs.

Proactive Engagement with Tech Ecosystem: Deepak advocates for proactive engagement with India’s tech ecosystem, encouraging early adoption of initiatives like IndiaStack. He challenges banks to rethink their approach and prepare for future changes in the financial landscape.

Importance of Early Adoption: Reflecting on his experiences at Kotak, Sharma stresses the importance of early adoption of innovative initiatives. Banks that jump in early can leverage emerging opportunities and drive meaningful change.

Value of Learning from Ventures: Deepak highlights the significance of learning from both successful ventures like OCEN and past failures. This learning process is essential for banks to navigate the evolving tech landscape effectively.

Structured Innovation with the 5C Model: Sharma’s structured approach to innovation, encapsulated in the 5C model, emphasizes critical aspects such as customer acquisition, commercial viability, credit assessment, compliance, and collections. This framework ensures alignment on objectives and risk management strategies.

Startup Mindset and Controlled Pilots: Adopting a startup mindset within traditional banking institutions, Deepak advocates for establishing small, specialized teams focused on data analysis, technology, and risk management. Controlled pilots with defined success metrics enable banks to manage—- risk effectively and drive innovation.

Importance of Trust-Based Scoring: Sharma underscores the importance of trust-based scoring systems and proprietary scorecards for credit assessment. Moving away from traditional methods, these innovative approaches provide a holistic view of creditworthiness, especially for SMEs with limited credit histories.

Optimism about OCEN: Deepak Sharma’s views on OCEN reflect a visionary approach to addressing India’s credit gap. He sees OCEN as a pivotal platform to harness India’s data richness and enable comprehensive credit assessment and lending solutions.

In conclusion, Deepak Sharma’s insights emphasize the necessity of embracing innovation and leveraging technology to drive inclusive growth in the financial services sector. By adopting proactive strategies, banks can navigate the evolving landscape of digital lending and unlock opportunities for underserved segments, contributing to India’s economic development.

OCEN is an initiative to unbundle lending and enable the creation of specialized entities, each specialized at one part of the job. Therefore, we envision the future of lending to be a partnership between multiple firms individually focused on sourcing/distribution, identity verification, underwriting, capital arrangement, recollections, etc. The entities like marketplaces who have high business-connect with their customers (businesses or individuals), can embed credit offerings in their applications now. These entities are referred to as Loan Agents’ (LAs) and were previously referred to as ‘Loan Service Providers’ (LSPs).

OCEN (Open Credit Enablement Network) aims at democratising the lending ecosystem. The core philosophy is using open networks to reach out to maximum borrowers and lenders, with reduced risk, more transparency, strict control on funds (both end use & collections) and thus building a robust lending ecosystem. At the borrower level, using consent driven architecture and personal data as information collateral, any type of borrower (even new to credit or people with poor credit scores), can access financing. The end-to-end digital processes not only reduces the total cost of operations, but also has the advantage of reaching out to anyone and everywhere, without the lender having a physical presence. For example, sitting out of Jaipur, a NBFC has disbursed OCEN loan on GeM Sahay to borrowers operating from Andaman Nicobar Islands, Manipur, Baramullah etc and the smallest loan transaction has been of Rs.160 for business purposes.

OCEN is the right protocol, to bring credit/finance to the bottom of the pyramid and at the same time lenders also make money with this same section of people at the bottom of the pyramid. OCEN not only levels the playing field between incumbents and challengers, but also reduces the concentration risk which comes with size at bigger players. Most MSMEs are working capital intensive businesses that need quick money and do not have collateral securities to put up to banks for conventional Cash Credit limits like financing. For such businesses, this is a tool to grow their businesses, and improve their credit scores.

Lenders see opportunities in not only sourcing new business, but also reduced risk due to high quality data and use of DPI (Digital Pubic Infrastructure), like GSTN, Account Aggregator, Digilocker and its associated APIs, like mobility, Health, Fastag etc.

Why OCEN

Low Cost of Acquisition >> The Borrower Agent brings his borrowers on the network, reducing the cost of acquisition through various channels. OCEN framework benefits the Lenders to gain easy access to borrowers. Not just borrowers of one network, but easy access to multiple sets of borrowers of multiple networks.

Lower Cost of Underwriting >> The Borrower Agent also acts as a Provider of Derived Data along with other Underwriting data from various sources like GSTN and Account Aggregator which helps in lowering the Cost of Underwriting

Digitisation >> OCEN Digitises the whole process which involves various activities like Bureau pull, KYC validation, Account Aggregator data, E-Sign on documentation, e-NACH for repayment etc and reduces the time and effort of processing at reduced costs.

Reduced Cost of Collections >> OCEN provides a large opportunity to Lenders and Borrowers to participate in T4 (Type 4) loan products which have End Use Control and Collections control for ensuring higher portfolio quality and cash flow control as well as reduced Cost of collections

OCEN solves for MSME’s Credit requirements: Small Ticket Short Tenure Loan

Small businesses need loans of smaller amounts and for shorter tenures (15/30/90 days) for their businesses compared to larger businesses to help them navigate through the requirement of day-to-day Working Capital needs.

It also helps Lenders to create Loan books for smaller loans which are granular loan exposure on a rotational basis, compared to large bulky loans. Hence reducing concentration risk.

As these Loans are for short tenure, there is higher predictability and lower risk compared to long tenure loans in which recovery of loans may sometimes be a challenge.

The Loan Agent (LA) model is a departure from the Direct Sourcing Agent (DSA) model and is an ‘agent of the borrower’. The LA explains to borrowers their ‘bill of rights’ ensuring transparency and safeguarding of borrower interests. They educate the borrowers about the various credit product offerings, pricing and more details. They help the borrowers get access to formal, affordable credit at low interest rates and collaborates with lenders to create more tailored offerings for borrowers.

In their simplest form, LAs are a loan marketplace that enables borrowers to compare loan offers from multiple lenders and choose the best one. In a more advanced version, the LAs are akin to a borrower’s financial advisor, looking after their interests, fetching the best offers and advising the customer to make good decisions.

In the longer run, it is envisioned that many more LAs (with apps) will be created. Each of them would focus on distinct borrower pools and build the specialized experiences suited to their customers. This would allow lenders to focus purely on their underwriting and collections logic and cater to diverse collaborations with the LAs.

OCEN 4.0

The OCEN model has been built incrementally in phases, with reinforced learnings from each of the previous pilots. The goal for OCEN 4.0 is to build an ecosystem of participants that creates a Cambrian explosion of cash-flow based loan products across different MSME sectors and different types of borrowers.

Participant Roles

OCEN 4.0 supports specialized roles for the participants. The purpose of introducing new roles is that it promotes specialization and enhances system efficiency. For example, by establishing a local network of participants, the burden on lenders is reduced, resulting in increased credit accessibility in underprivileged areas.

Role

Description

Lender

Lenders are the regulated entity that create and own the credit products. They work with other participants as part of a Product Network to serve the Borrower. The Loan-agent understands the borrowers’ credit requirements and works with the lenders to create the product.

Loan-Agent (LA)

Agent of the borrower who will help the Borrower to pick up the best loan offer. The Borrowers agent will charge the Borrower a fee for helping them select the best loan. Loan agent is a more inclusive term that encompasses both Borrower Agent (BA) and Lender Service Provider (LSP), spanning across the existing DLG model referred to as LSP and the emerging model in which BA operates as the borrower agent.

Derived Data Partner (DDP)

A derived data provider is a collaborating partner within the network that furnishes supplementary data to the Lender, aiding in enhancing their underwriting engine with additional information.

Collections Partner (CP)

A Collections Partner is a network-affiliated collaborator designated by the Loan Agent (LA) to aid in the collection process. The lender retains the option to either opt for the Collections Partner or continue using their existing collection procedures.

Disbursement Partner (DP)

A Disbursement Partner (DP) is responsible for supporting Purpose Controlled products. This partner will establish integration with suppliers, retrieve their catalog, and facilitate seamless direct payments to suppliers within the OCEN journey.

KYC Partner

A KYC partner is a collaborator selected by the Loan Agent (LA). This partner can be engaged for Assisted KYC or any technology-related specialization available on the network. The lender retains the choice to employ the KYC partner within the network or continue with their existing procedures.

In addition to the participant roles above, OCEN framework also relies on Account Aggregator and Credit Guarantees (CGTMSE) as part of the loan journey.

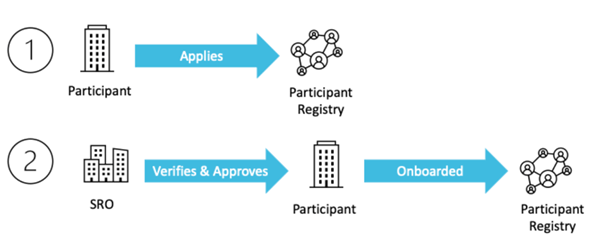

Participant Onboarding

All participants are onboarded to OCEN 4.0 via the participant registry. A standard onboarding process is followed for all participants, and their verification is guaranteed by SROs to ensure that new members receive an equivalent level of trust within the network.

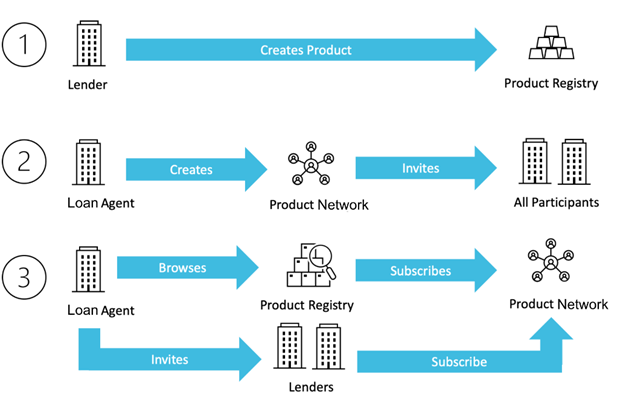

Product and Product Network onboarding

Lender will create & manage the Product and the Loan Agent will create & manage the Product Network to serve that product. All participants in OCEN 4.0 can browse the Products and Product Networks on the Product Registry and subscribe to serve a Product via the Product Networks.

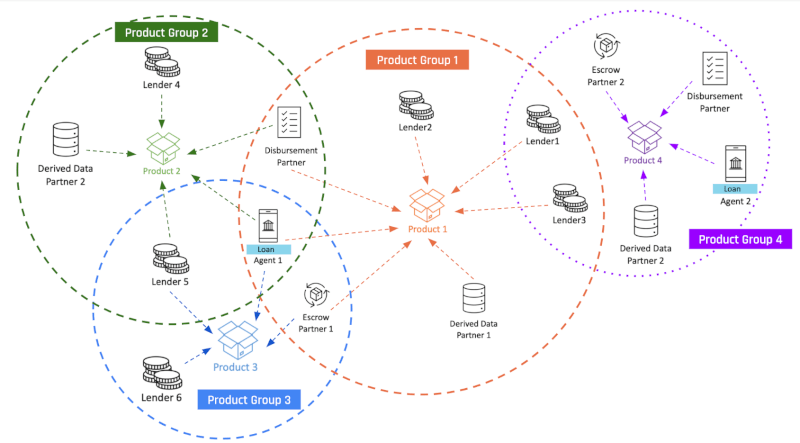

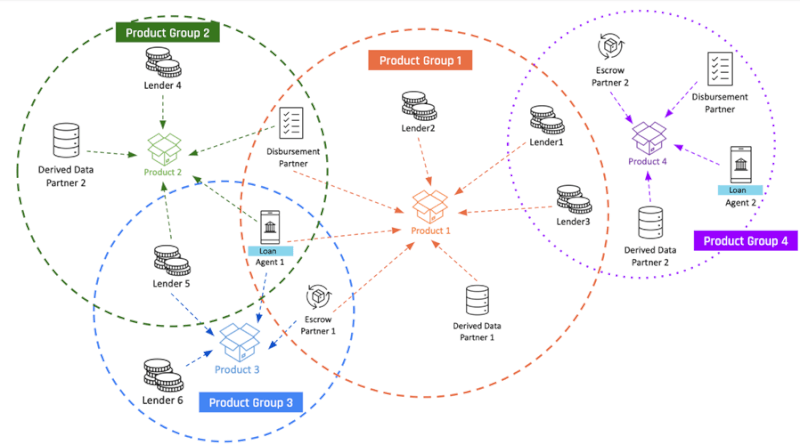

Product Networks

OCEN 4.0 enables a network of product networks that participants can discover, collaborate and serve products to borrowers. See sample example below:

Network begins with Product Network 1

Created by Loan Agent 1 who onboards as network participants – 3 lenders, disbursement partner, collections partner and a derived data partner

Loan agent 1 can serve their borrowers other products as well.

Network expands with Product Network 2

Created by Loan Agent 1 who onboards as network participants – 2 new lenders, the same disbursement partner, and a new derived data partner

Loan agent 1 can continue to serve their borrowers other products as well.

Network expands with Product Network 3

Created by Loan Agent 1 who onboards existing participants and a new lender (Lender 6) to serve the product

Participants can discover products and join the product network

Network expands with Product Network 4

Created by a new LA, Loan Agent 2, who onboards existing and new participants to serve the product to their borrowers

GeM is a short form of one stop, ‘Government e-Marketplace’ where common user goods and services can be procured by various Ministries and agencies of the Government. Government e Marketplace (GeM) offers both products and services as part of its offerings to its registered buyers. GeM facilitates the procurement of a spectrum of Product and Service categories in a way to facilitate Buyer in ease of selection and procurement. GeM SAHAY is an online platform built on the OCEN protocol that provides loans against Purchase Orders to the sellers.

GeM SAHAY is the pilot project on OCEN to validate the idea of cash-flow based lending for MSMEs. In this pilot, GeM (Government e-Marketplace) is the Loan Agent. The Lenders onboarded onto the pilot offer loans to MSMEs on the GeM portal against government purchase orders. The pilot validates that short-tenure, small-ticket size loans enabled via the OCEN network works for all participating parties.

GeM as a Loan Agent allows the Goods and Service Providers on GeM to apply for Loans against Purchase orders received through various Government buyers on the GeM portal.

GeM as a Loan agent helps onboard borrowers for lenders reducing the acquisition cost for the lenders

GeM being a loan agent also acts as a Derived Data Provider as it carries rich data of the participating MSME borrowers in terms of past number of orders, value of orders executed, quality incidences, completion timelines, etc and these data points help the participating Lenders to underwrite the MSME loan application.

GeM facilitates digital loan process for MSMEs on its GeM SAHAY portal by ensuring integration with multiple lending institutions and helps the Borrower MSMEs to receive multiple offers for its loan applications. Allowing the MSME to choose the best suitable loan offer creates a market shift from Lender’s market to Borrower’s market.

GeM also acts as a Collection partner for the Lending institutions as it helps the lender with repayment of the loan for the purchase order though the Escrow account where the payment for the orders executed is credited by the purchasing entities.

A second pilot that expanded on the above is the GST SAHAY pilot project. This pilot uses GST data to enable working capital loans where SIDBI is acting as the Loan Agent. An additional parameter for validation on this pilot was the inclusion of the Account Aggregator data for loan underwriting.

In GST SAHAY, borrowers can seek loans against unpaid B2B Invoices for supply of Goods and Services to other businesses. Any business registered with GSTN and filing the statutory returns on GSTN can seek financing against Invoices where goods or services are supplied on credit period.

Borrower can register on GST SAHAY application and upload Invoices against which it seeks to avail financing.

The GST SAHAY application, after seeking the consent of borrower will pull details available from the GST network for its past invoice transactions filed with GSTN, periodic return filings and share the same with Lenders for evaluation and underwriting and credit decisioning.

Similarly, GST SAHAY application after seeking the consent of the borrower will pull details of the Bank statements available from Account Aggregator framework for its past banking data and share the same with Lenders for evaluation and underwriting and credit decisioning.

Lenders will parallelly also check the Credit Bureau of the borrower to assess credit worthiness and past performance on existing credit facilities from other lenders, if available.

Lending institutions will digitally consume all these data points, along with details available on the Invoice to be financed and by using its proprietary rule engine for underwriting and scoring model, will provide an offer to the borrower for the respective Invoice to be financed.

Borrowers may receive multiple offers (higher loan amount, lesser interest rate, longer tenure) from different Lenders based on their evaluation criteria and will have a choice to select the best suitable offer for seeking the disbursement in a digital way by e-signing the loan agreements, e-Nach / Standing instructions, wherein the amount will be credited to the borrower’s account within few minutes.

There are other OCEN innovative product networks which are at various stages of development and are expected to go live to provide seamless credit to the credit starved MSMEs using OCEN API specifications for communication between the parties (Borrowers, Lenders, Loan Agents and other participants)

In this recent OpenHouse, Sagar Parikh discusses with Dr Ravi Modani how democratizing credit through short-tenor and small-ticket loans can help finance Indian MSMEs, 99% of which are micro-enterprises. Dr Modani shares his insights and invaluable guidance to navigate the complex world of B2B financing for MSMEs.

He also delves deep into the challenges faced by them in accessing financing, particularly in the realm of B2B transactions. Drawing from his extensive experience and research, he offers a fresh perspective on the traditional lending landscape and presents innovative solutions to empower MSMEs.

Key Insights from the Video:

The MSME Financing Dilemma: Dr. Modani highlights the significant hurdles that MSMEs encounter when seeking short-tenor and small-ticket loans. He emphasizes the need for a paradigm shift in lending practices to better serve the unique needs of these businesses.

A New Way Of Financing for MSMEs: Dr. Modani advocates for a pioneering financing approach for MSMEs, highlighting the effectiveness of short-tenor and small-ticket loans. These loans, being revolving in nature throughout the year, allow lenders to disburse a higher volume of loans. Consequently, lenders can potentially amplify their AUM by up to 8 times, surpassing the typical 5-6 times AUM ratio associated with traditional lending practices.

Comparing Financial Platforms: Dr. Modani provides a comprehensive comparison between TReDs and OCEN, offering insights into the advantages of leveraging public networks like OCEN for enhanced interoperability and accessibility.

The Power of Public Networks: Leveraging platforms like OCEN and GeM can significantly reduce operational costs for lenders, ultimately leading to lower lending costs and improved efficiency. Dr. Modani illustrates how these public networks can drive down the cost of lending, benefiting both lenders and borrowers alike.

The Time Sensitivity of MSME Financing: Dr. Modani underscores the time-critical nature of MSME lending and stresses the importance of streamlining the loan journey to ensure timely access to funds for businesses.

His illustrations and learnings help in navigating the complex world of MSME financing by embracing innovative approaches. He believes that leveraging public networks like OCEN will only help lenders unlock new growth and success in today’s lending landscape by opening multifold opportunities to them.

In our most recent OpenHouse, we embark on an insightful exploration of the transformative landscape in MSME lending, featuring Bhavik Vasa, the Founder of GetVantage, and Sagar Parikh. The conversation delves into the potential of creating groundbreaking impact through interoperable networks, particularly focusing on OCEN. The discussion navigates the dynamic intersection of finance and technology, highlighting how inventive solutions are reshaping the lending panorama. Emphasizing the crucial role of interoperability, the dialogue underscores its significance in bridging the credit gap, propelling the MSME sector into a new era of unprecedented growth.

Key Takeaways:

Network Effects Unleashed: OCEN catalyzes network effects, narrowing the credit gap and expanding the market, fostering inclusivity and vibrancy.

Efficiency through Interoperability: Standardized protocols cut costs and efforts, providing high-quality data for lenders while empowering MSMEs with smoother access to loans.

Addressing Unmet Needs: Explore how interoperable networks bridge gaps in unsecured lending, catering to shorter tenures and smaller loan sizes.

Tech-Enabled Business Growth: Witness the role of unsecured lending in a tech-driven landscape, fostering a circular consumption economy for economic growth.

Personalized FinTech Solutions: Bhavik advocates for a borrower-centric approach, urging lenders to view lending through a tech and data-driven lens, benefiting both parties.

Collaboration Dynamics: Conclude with insights on how NBFCs and banks can coexist and collaborate, playing to their strengths for a more robust lending environment.

Ready to unlock the future of MSME lending? Join the conversation now!